When venturing into investments, we often encounter two main characters – equity and debt. They’re the backbone of any investment strategy, regardless of the market’s nature or the company’s phase. Each plays a unique role, each offers different benefits and risks to investors.

The world of alternative investments is no different. Private equity and private credit have both emerged as popular choices of assets among investors. In this chapter, we’re going to explore the differences between these concepts in detail.

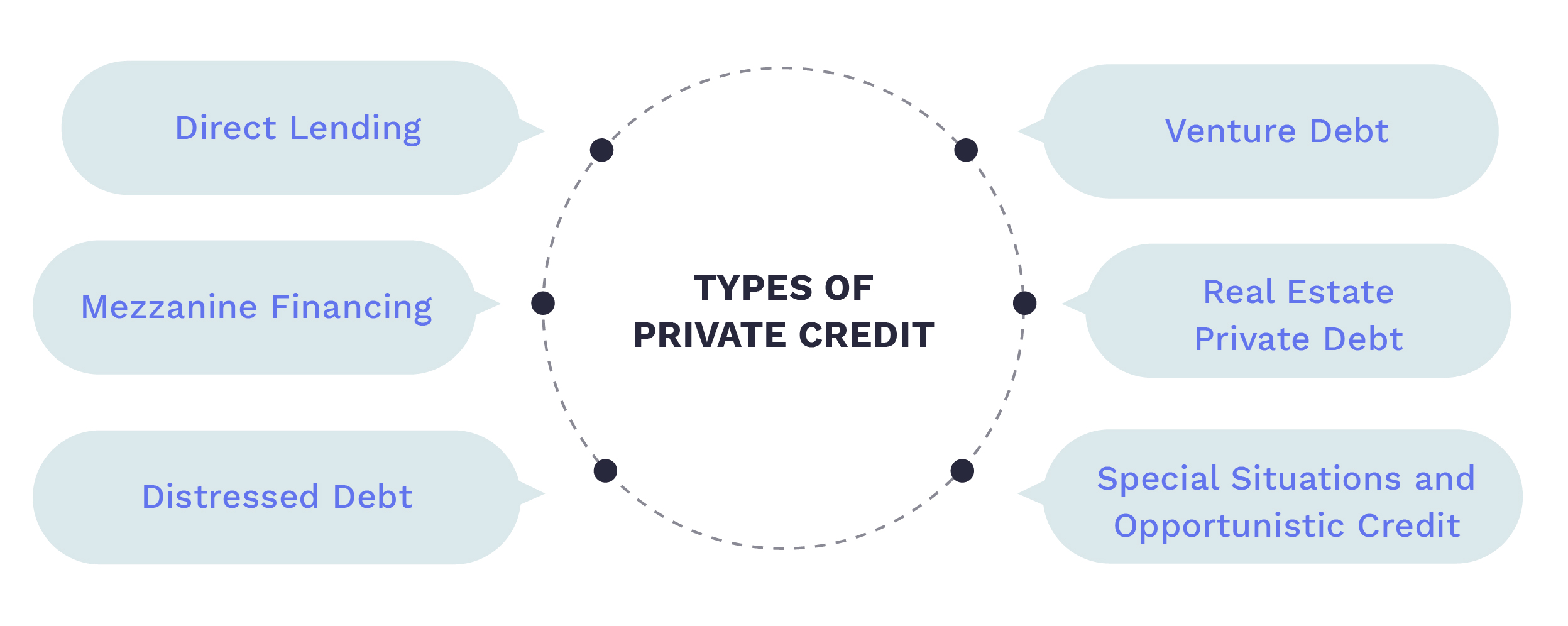

Private credit is like a friendly neighbourhood alternative to a traditional bank loan. It’s where private funds, institutional investors, and non-bank entities lend a hand to businesses in need of cash.

Take, for instance, the owner of your local bakery who’s dreaming of a bigger kitchen to start catering. He’s at a crossroads for funding: the familiar route of a bank loan or the path less travelled with a private lender.

Banks are the old-school choice, but private lenders offer a more flexible journey. They’re not just about handing out cash; they tailor their support to fit the unique needs of businesses, especially those on the brink of growth but not quite fitting the strict criteria of banks.

Think of the bakery owner who doesn’t quite tick all the boxes for a traditional bank loan. This is where private credit comes into play. It’s not about rigid, cookie-cutter solutions; it’s about stitching together a financial plan that fits the unique situation of the bakery, just right.

A significant shift in the private debt landscape emerged following the Global Financial Crisis. Prior to the crisis, most businesses turned to conventional banks for their loan needs, particularly for higher-risk ventures.

Post-crisis, however, these banks shifted their approach, increasingly avoiding investments perceived as high-risk. This was primarily due to the introduction of stricter capital requirements under frameworks like Basel III. These regulations required banks to maintain higher capital reserves against risky assets to buffer against potential losses and high-risk lending less attractive. For example, the Tier 1 capital requirements (for a bank’s core capital, equity and reserves) was increased from 4% to 6%. As for Tier 3, which included a riskier tier of capital was eliminated.

This change opened a door for private or direct lenders. These lenders were willing to take on the risks that banks were avoiding. They were not seen as presenting a systemic risk and, in the US context, were not insured by the FDIC. So, they have a different regulatory regime as compared to banks, which does not impose high capital requirements. As a result, the amount of money managed in private debt—referred to as assets under management (AUM)—has seen a notable increase.

In 2022, private credit investments surged by an immense 89% and reached $10.2 billion. This growth is led by the emerging and developing markets — Asia, Middle East, Africa, Central and Eastern Europe and Latin America — in particular.

According to Jeff Schlapinski, Managing Director, Research at Global Private Capital Association (GPCA), “There are persistent financing gaps unaddressed by global or local banks that private credit funds are helping to fill.”

The rise in private debt is more than just a reaction to the banks’ reluctance. It’s a response to a market need. Many companies, especially mid-sized ones, found themselves in need of funding options outside of traditional banking systems.

Private debt lenders filled this gap, offering loans tailored to these companies’ specific needs. The flexibility in the terms and conditions of these loans surpasses what traditional banks typically offer. This makes them particularly appealing to companies in special circumstances or those in search of more tailored financial solutions.

Returns from private debt often favourably compare to those of public debt. Investors in private debt are usually compensated for the illiquidity risk with higher yields, known as the ‘illiquidity premium’.

Some private debt investments also offer ‘floating rate’ returns, which vary based on underlying interest rates, providing flexibility in a rising interest rate environment.

The risk profile of private debt investments can vary significantly. Unlike public debt, where credit ratings by agencies like Moody’s, S&P, and Fitch provide a standardised risk assessment, private debt often lacks such transparent credit ratings. Therefore, assessing the risk of private debt investments can be more complex and requires thorough due diligence.

A tech startup, with a revolutionary product, needs capital to scale up operations and enter new markets. They choose private equity, trading a stake in their company for not just funding but also the expertise and industry connections that the PE firm brings. This partnership fuels their growth journey, leveraging the PE firm’s resources and network.

A family-owned manufacturing business faces a temporary cash flow crunch due to market fluctuations. They opt for private credit, securing a loan that allows them to weather the storm without giving up any ownership or control. The loan is structured to align with their cash flow, ensuring they can manage repayments without undue stress.

An established retail chain plans to expand its operations nationally. They choose private equity to leverage the strategic and operational expertise the PE firm offers. In exchange for a significant equity stake, they gain access to capital and a partner that actively contributes to refining their expansion strategy and execution.

| Aspect | Private Equity | Private Credit |

|---|---|---|

| Definition | Private equity is like being part of a business’s story, investing directly in companies (not on public markets) and often actively influencing their strategy. | Private credit is akin to being a supportive character in a business’s narrative, providing loans to companies outside the traditional banking system. |

| Returns | Aiming for the stars, private equity looks for high returns through significant growth or strategic changes in the business. | Private credit plays it safer, focusing on steady returns through interest payments, with a more predictable outcome. |

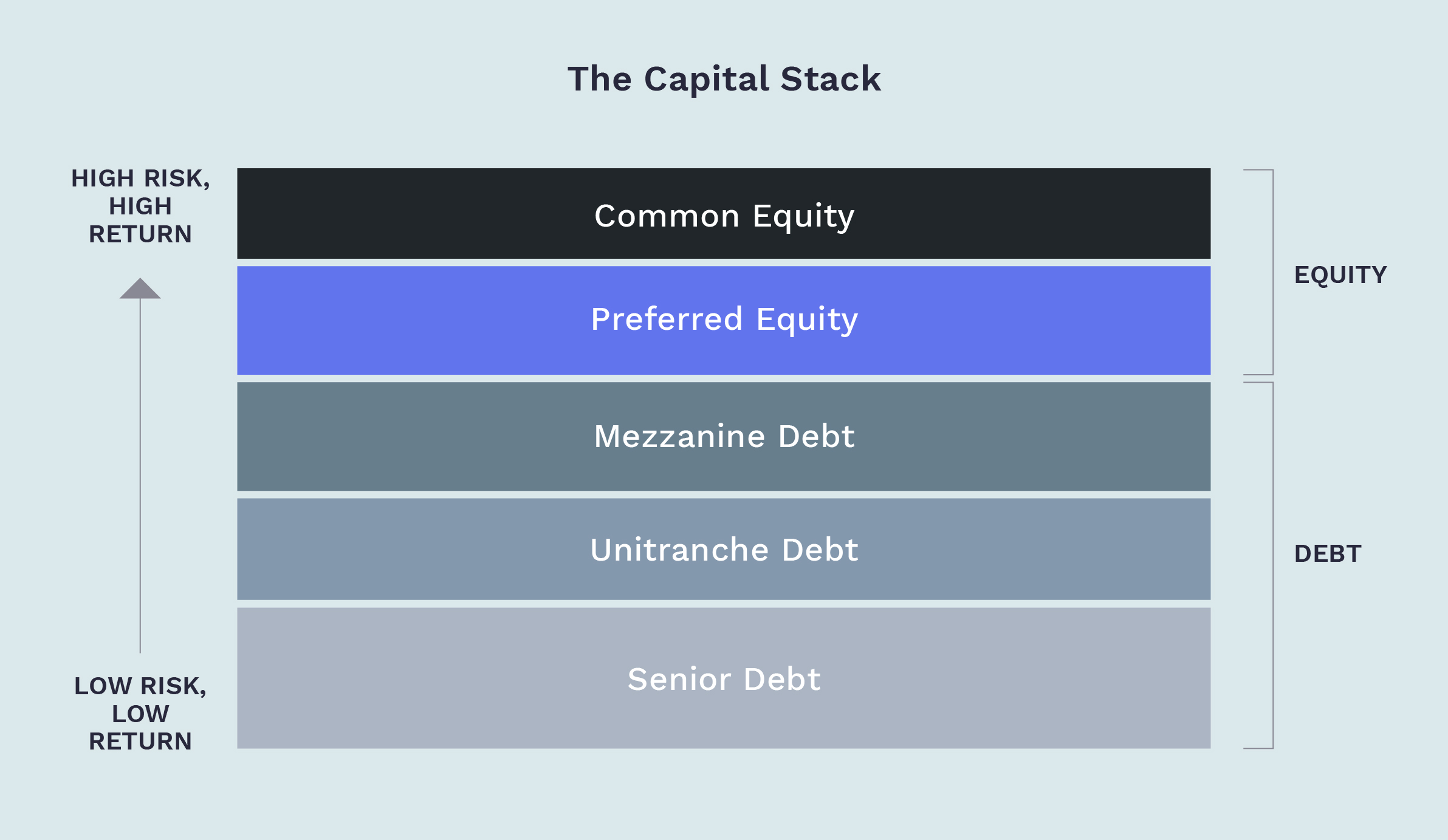

| Risk Profile | Higher risk, higher reward – private equity is like a rollercoaster, with potential for great highs and significant lows. | A more stable journey – private credit typically carries lower risk than equity, as debt repayment often takes priority over equity in case of liquidation. |

| Involvement in Business | Hands-on approach – private equity investors often roll up their sleeves and get involved in managing and guiding the business. | More hands-off – private credit investors usually don’t get involved in day-to-day business operations. |

| Investment Horizon | Long-term commitment – private equity investments often require patience, as they can take years to mature and yield returns. | Shorter horizon – private credit agreements usually have a fixed duration with a clear exit strategy, aligning with loan repayments. |

| Income Generation | Growth-focused – private equity gains are typically realized when the company is sold or goes public. | Regular income – private credit provides returns mainly through ongoing interest payments, offering a predictable cash flow. |

| Security and Collateral | Equity stakes – private equity involves owning a part of the company, without collateral backing the investment. | Secured interest – private credit is often backed by company assets, providing an added layer of security. |

TERMS OF USE

Thank you for your interest in our Website at https://unlistedintel.com/. Your use of this Website, including the content, materials and information available on or through this Website (together, the “Materials”), is governed by these Terms of Use (these “Terms”). By using this Website, you acknowledge that you have read and agree to these Terms.

NO OFFER, SOLICITATION OR ADVICE

Our site is provided for informational purposes only. It does not constitute to constitute (i) an offer, or solicitation of an offer, to

purchase or sell any security, other assets, or service, (ii) investment, legal, business, or tax advice, or an offer to provide such advice or (iii) a basis for making any investment decision.

The Materials are provided for informational purposes and have been prepared by Oister Global for informational purposes to acquaint existing and prospective underlying funds, entrepreneurs, and other company founders with Oister Global's recent and historical investment activities.

Please note that any investments or portfolio companies referenced in the Materials are illustrative and do not reflect the performance of any Oister Global fund as a whole. There is no obligation for Oister Global to update or alter any forward-looking statements, whether as a result of new information, future events, or otherwise.

PURPOSE LIMITATION AND ACCESS TO YOUR PERSONAL DATA:

We will only collect your personal data in a fair, lawful, and transparent manner. We will keep your personal data accurate and up to date. We will process your personal data in line with your legal rights. We use your name and contact details, such as email, postal address, and contact number to continue communications with you. We may also use your contact information to invite you to events we are hosting or to keep you updated with our news.

USE OF COOKIES OR SIMILAR DEVICES

We use cookies on our website. This helps us to provide you with a better experience when you browse our website and also allows us to make improvements to our site. You may be able to change the preferences on your browser or device to prevent or limit your device’s acceptance of cookies, but this may prevent you from taking advantage of some of our features.

MATERIAL

The material displayed on our site is provided “as is”, without any guarantees, conditions, or warranties as to its accuracy, completeness, or reliability. You should be aware that a significant portion of the Materials includes or consists of information that has been provided by third parties and has not been validated or verified by us. In connection with our investment activities, we often become subject to a variety of confidentiality obligations to funds, investors, portfolio companies, and other third parties. Any statements we make may be affected by those confidentiality obligations, with the result that we may be prohibited from making full disclosures.

MISCELLANEOUS

This Website is operated and controlled by Oister Global in India. We may change the content on our site at any time. If the need arises, we may suspend access to our site, or close it indefinitely. We are under no obligation to update any material on our site.

CONTACT INFORMATION

Any questions, concerns or complaints regarding these Terms should be sent to info@oisterglobal.com