We get to see the big headlines when startups rake in funding one round after another. We also get to see when they reach their grand finale — which is often either an acquisition, a merger, or an IPO. What we don’t see is the stuff that happens in between. The extensive number crunching, evaluation, and due diligence done by VCs, who basically dot the i’s and cross the t’s before handing over the money.

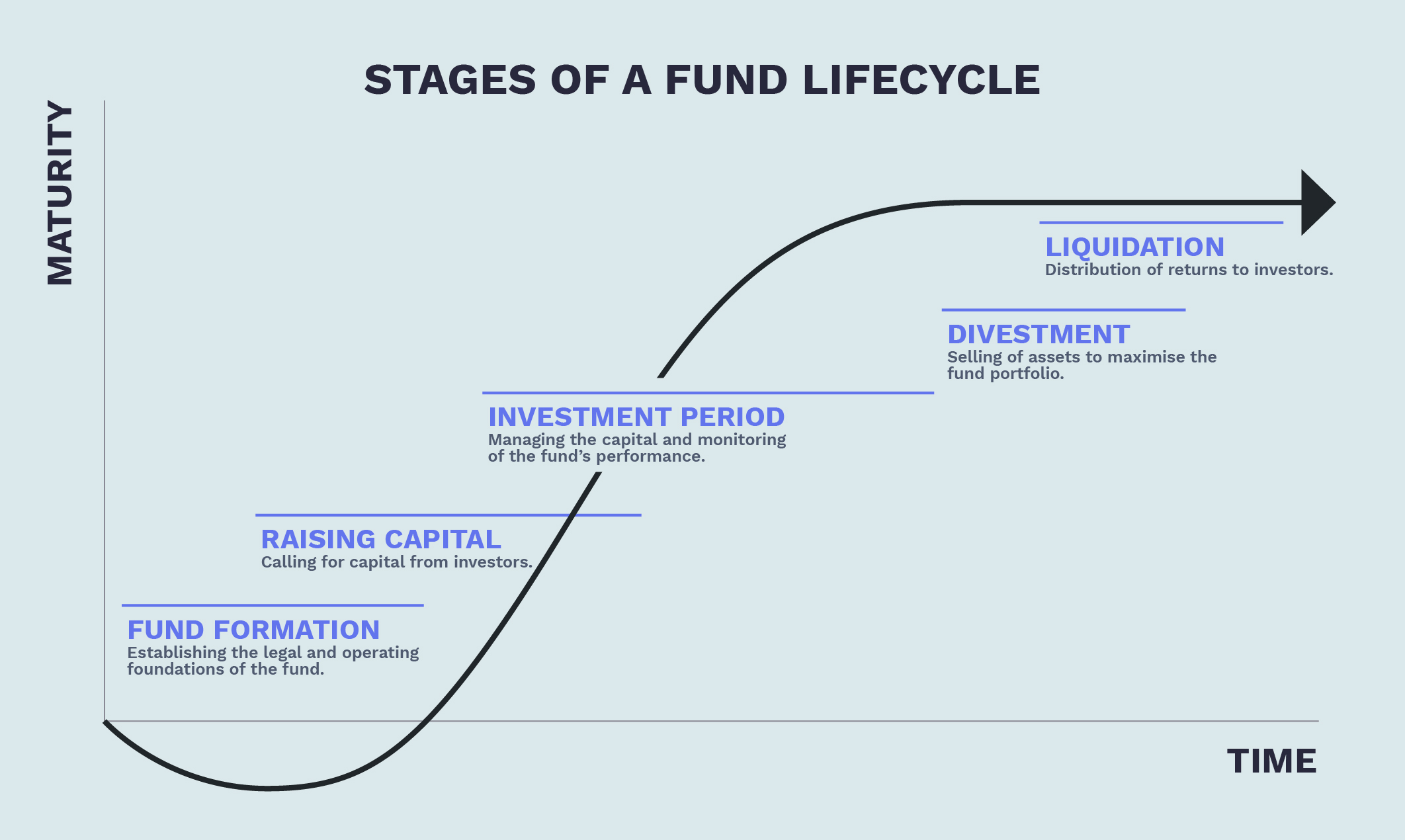

In this chapter, we examine an entire time-lapse of the fund investment lifecycle — right from the start where a founder approaches VCs to the end where the VC exits the investment.

The investment process always begins with defining investment objectives. What do we hope to achieve? What kind of an investment size are we looking at? What is the average duration that we would like to invest for? These are some common questions that VCs ask themselves.

They decide on their risk tolerance, return expectations, and the specific types of startups they intend to target.

The choice of industry is an important one, in this case. Most alternative investment funds (AIFs) prefer to invest in a few specific sectors. This is primarily because a certain level of familiarity and expertise is required at several stages of the investment process.

For starters, to identify good investment opportunities, investors will need to understand the product potential of startups. Apart from that, even after the investment is done, investors often take a hands-on approach and participate in the growth and development of the startups.

This stage of the investment lifecycle involves the structuring of the private market fund and the sourcing of capital from different investors.

In the private market, funds are registered as alternative investment funds (AIFs) with SEBI. The most common fund structure is that of a trust. AIFs can also be set up as companies or Limited Liability Partnerships (LLPs), but these structures are rare in India.

Creating a fund structure involves finalising the fund size, fee structure, target investor profiles, and any legal considerations.

To attract investors, the fund managers create marketing presentations. They present at industry conferences and leverage any existing investor relationships. The goal is to generate interest and attract potential investors.

Of course, it is also very important to find investors whose objectives align with those of the fund. For instance, they should have similar investment goals, risk appetite, and preferences.

Just as investors conduct due diligence on companies, fund managers also conduct due diligence on potential investors. This process can be quite extensive and ensures that the investors have the necessary financial capacity and can contribute to the fund’s success.

The reason why the due diligence process is so important is because the number of participants in this case is relatively small. In the public markets, there may be thousands of investors in a particular company. In the private markets, however, the number of investors is just a fraction and the investment amount is much larger.

Each investor is important for the success of the fund on the whole, and it is very important to make sure that the interests are aligned.

Now that the alternative investment fund is set up and ready for deployment, the third step is to identify suitable investment opportunities that fit with the fund’s objectives.

During this process, the fund managers use their extensive networks to identify opportunities for investments. They even participate in industry events and specialised deal flow platforms. A number of startups are shortlisted and they set up a deal pipeline.

The fund managers conduct rigorous due diligence on the prospective startups. This is quite comprehensive, as you can imagine. A large number of options are evaluated to identify a select few good opportunities. Deals are evaluated through financial analysis, legal reviews, operational assessments, and market validation.

Now, depending on what size of startups the fund invests in, the number of deals can change.

For instance, venture capitalists generally invest in seed and early-stage startups. In this case, because the startups are still in their infancy, it can be difficult to narrow down their potential. To manage risks, venture capitalists invest in a larger number of companies. Even if a few fail, the success of the others can balance out the portfolio.

On the other hand, private equity growth funds generally invest in mid-sized startups. These startups have already existed for a few years, so their potential is easier to identify. These funds invest in a smaller number of startups but the investment amount is considerably higher.

This entails a comprehensive assessment to evaluate the viability of an opportunity and its alignment with the investment thesis.

To calculate the valuation of a private company, funds use a variety of methods such as discounted cash flow (DCF), comparable company analysis (CCA), and market multiples. This is quite a critical step to determine the fair value and the worth of the target company.

This stage involves the process of actually making the investment in the startups that have been identified in Stage 3.

Once the due diligence process is completed and the potential opportunities have been identified, fund managers proceed to negotiate the structure of the deal with the selected startups.

This involves negotiations to define terms and establish the ownership stake, and it also sets out governance rights. The startups work with the private market funds in this case to finalise the term sheet.

After the terms have been negotiated, all that remains is to formalise the agreement. This involves drawing up contracts that clearly define the terms, rights, and responsibilities of all the parties involved.

The table below shows the fifteen largest deals in the Indian private markets in 2022.

| COMPANY | SECTOR | INVESTOR | DEAL VALUE (US$ Mn) |

|---|---|---|---|

| Viacom 18 | Media & Entertainment | Bodhi Tree Systems | 1,176 |

| YES Bank | BFSI | Advent, Carlyle | 1,100 |

| Securonix | SaaS | Vista Equity Partners | 1,000 |

| Citius Tech | IT/ITeS | Bain Capital | 960 |

| VerSe Innovation (Dailyhunt) | Consumer tech | CPP Investments | 833 |

| IGT Solutions | IT/ITeS | Baring Private Equity | 810 |

| BYJU’s | Consumer tech | Byju Raveendran, Vitruvian | 800 |

| Suven Pharmaceuticals | Healthcare | Advent | 762 |

| Gujarat Titans | Sports | CVC Partners | 753 |

| Swiggy | Consumer tech | Invesco | 700 |

| ReNew Surya Roshni | Energy | Mitsui PE | 662 |

| Allen Education | Education | Bodhi Tree Systems | 600 |

| IDFC Asset Management | BFSI | Bandhan Bank | 592 |

| Tata Power Renewable Energy | Energy | Mubadala, Blackrock | 525 |

| UPL Corp | Manufacturing | KKR | 500 |

In the case of public investments, the involvement of investors tapers off after the investment has been made. In the private markets, however, the scenario looks very different.

After investment, the fund managers work closely with the company’s management team. Depending on the terms of the negotiated contract, this involvement can come at various levels. In some cases, private market funds retain seats on the company’s board to advise on strategic initiatives and new projects. In some other cases, they may even be involved in the day-to-day operations of the startup.

The objective, of course, is to create value.

Leveraging their industry expertise, network, and available resources, fund managers collaborate with the startup to realise its growth and profitability goals. The potential is already present. The aim is to create the right environment and the most supportive circumstances so that this potential can germinate.

At the right moment, fund managers exit from the investment.

Unlike public markets, private investments are not very liquid in nature. In order to exit from a portfolio company, fund managers have to plan their exit strategies well beforehand and finalise the terms with the startup.

Possible methods of exiting from the startup include selling the company to another buyer, merging it with another company, or even through an IPO.

When the investment is done in the early stages of the startup’s growth, investors can exit during subsequent rounds of funding. Sometimes, even the startups themselves can buy back the ownership stake from the investors.

After the fund exits from the existing startup and the profits are realised, the private market fund returns the capital and distributes the profits to different investors.

In some cases, the fund may invest a small part of the invested capital, say about 10% to offset the effects of the fees charged.

Private market funds charge a fee to the investors in return for the management services and any operational expenses incurred. But, as the fee is paid out of the committed capital of the fund, it reduces the amount of capital available for investments.

Allowing the funds to recycle a part of the investment can help counteract this effect.

Venture capital funds, especially those that invest in early-stage startups, often reserve capital for follow-on investments.

Say, for instance, a fund invests in the pre-seed, seed, or even a series A round. It might retain enough capital so that it can also participate in the following funding rounds for its portfolio companies. In some cases, the fund can even retain up to 60-70% of the capital for follow-on investments.

Please note, that this strategy is generally used by venture capital funds and not private equity funds.

The fund decides how much capital to reserve for future investments and also, which portfolio companies to back.

The lifecycle of a fund is a meticulously orchestrated journey that requires careful planning, diligence, and collaboration. Fund managers develop their investment theses, raise capital, source investment opportunities, make investment decisions, foster growth and value creation, and ultimately, execute exit strategies. The private markets, with their distinct characteristics, offer investors the opportunity to actively engage with the growth and development of startups.

TERMS OF USE

Thank you for your interest in our Website at https://unlistedintel.com/. Your use of this Website, including the content, materials and information available on or through this Website (together, the “Materials”), is governed by these Terms of Use (these “Terms”). By using this Website, you acknowledge that you have read and agree to these Terms.

NO OFFER, SOLICITATION OR ADVICE

Our site is provided for informational purposes only. It does not constitute to constitute (i) an offer, or solicitation of an offer, to

purchase or sell any security, other assets, or service, (ii) investment, legal, business, or tax advice, or an offer to provide such advice or (iii) a basis for making any investment decision.

The Materials are provided for informational purposes and have been prepared by Oister Global for informational purposes to acquaint existing and prospective underlying funds, entrepreneurs, and other company founders with Oister Global's recent and historical investment activities.

Please note that any investments or portfolio companies referenced in the Materials are illustrative and do not reflect the performance of any Oister Global fund as a whole. There is no obligation for Oister Global to update or alter any forward-looking statements, whether as a result of new information, future events, or otherwise.

PURPOSE LIMITATION AND ACCESS TO YOUR PERSONAL DATA:

We will only collect your personal data in a fair, lawful, and transparent manner. We will keep your personal data accurate and up to date. We will process your personal data in line with your legal rights. We use your name and contact details, such as email, postal address, and contact number to continue communications with you. We may also use your contact information to invite you to events we are hosting or to keep you updated with our news.

USE OF COOKIES OR SIMILAR DEVICES

We use cookies on our website. This helps us to provide you with a better experience when you browse our website and also allows us to make improvements to our site. You may be able to change the preferences on your browser or device to prevent or limit your device’s acceptance of cookies, but this may prevent you from taking advantage of some of our features.

MATERIAL

The material displayed on our site is provided “as is”, without any guarantees, conditions, or warranties as to its accuracy, completeness, or reliability. You should be aware that a significant portion of the Materials includes or consists of information that has been provided by third parties and has not been validated or verified by us. In connection with our investment activities, we often become subject to a variety of confidentiality obligations to funds, investors, portfolio companies, and other third parties. Any statements we make may be affected by those confidentiality obligations, with the result that we may be prohibited from making full disclosures.

MISCELLANEOUS

This Website is operated and controlled by Oister Global in India. We may change the content on our site at any time. If the need arises, we may suspend access to our site, or close it indefinitely. We are under no obligation to update any material on our site.

CONTACT INFORMATION

Any questions, concerns or complaints regarding these Terms should be sent to info@oisterglobal.com