Why the years that age best rarely feel good at the time

In the early 2000s, a soft-spoken Indonesian collector named Rudy Kurniawan became the most powerful man in fine wine.

He bought aggressively at Christie’s and Sotheby’s, hosted lavish tastings in Los Angeles, and uncorked bottles most collectors would never see in a lifetime. Burgundy dominated his table ~ Domaine Ponsot, Romanée-Conti ~ the most revered names in the world, often from legendary years.

The vintages did the heavy lifting. Once a date like 1945 or 1947 was read aloud, the room leaned in. A great year explained everything.

The first cracks appeared when Domaine Ponsot stated publicly that bottles attributed to the estate from 1945 and 1947 had never existed. The Domaine had been closed during the war. No wine was produced in those years. Soon after, collectors noticed Rudy was offering Romanée-Conti in quantities exceeding the total historical production of certain vintages. The math didn’t work. The histories didn’t line up.

Yet for years, the market had accepted the bottles without protest because the years printed on the labels were among the most revered in wine history.

When the scheme finally unravelled, the mechanics were almost banal. Wines blended in a kitchen. Artificial ageing. Perfectly printed labels. Carefully chosen vintages. Tens of millions of dollars had already changed hands. Auctions were voided. Lawsuits followed. Tastings were replayed in memory, now with disbelief.

What endured was the realisation that value had organised itself almost entirely around the vintage.

The wine didn’t have to be great.The vintage did.

That distinction is important because it reveals how markets often price time before substance, narrative before verification, and reputation before outcomes.

What the Kurniawan episode revealed wasn’t just fraud, but how much weight markets place on time itself. Once a year acquired a reputation, it began to carry meaning, confidence, and price long before the substance was examined.

TL;DR: A guy sold fake legendary wines, and the market bought the story because the vintage on the label sounded priceless. The parallel in private markets is that “vintage” becomes a powerful shorthand in hindsight, because the year you deploy shapes pricing, competition, and the opportunity set.

Yes, the wine detour is deliberate. It’s our way of setting the mood for the year-end. As the wrap-ups roll in (and 2025 already looks like one for the books), it felt like the right moment, in Unlisted Intel, to use vintage as a lens for understanding why certain years end up carrying far more weight than others.

Before going any further, it’s worth confronting a deceptively simple question:

Do vintages really matter in private markets?

Not as folklore or shorthand, but in outcomes. How much of long-term performance is genuinely explained by the year capital is invested in? And how much is driven by everything that follows?

The answer isn’t a single insight, but a set of patterns that repeat across cycles. Four, in particular, stand out.

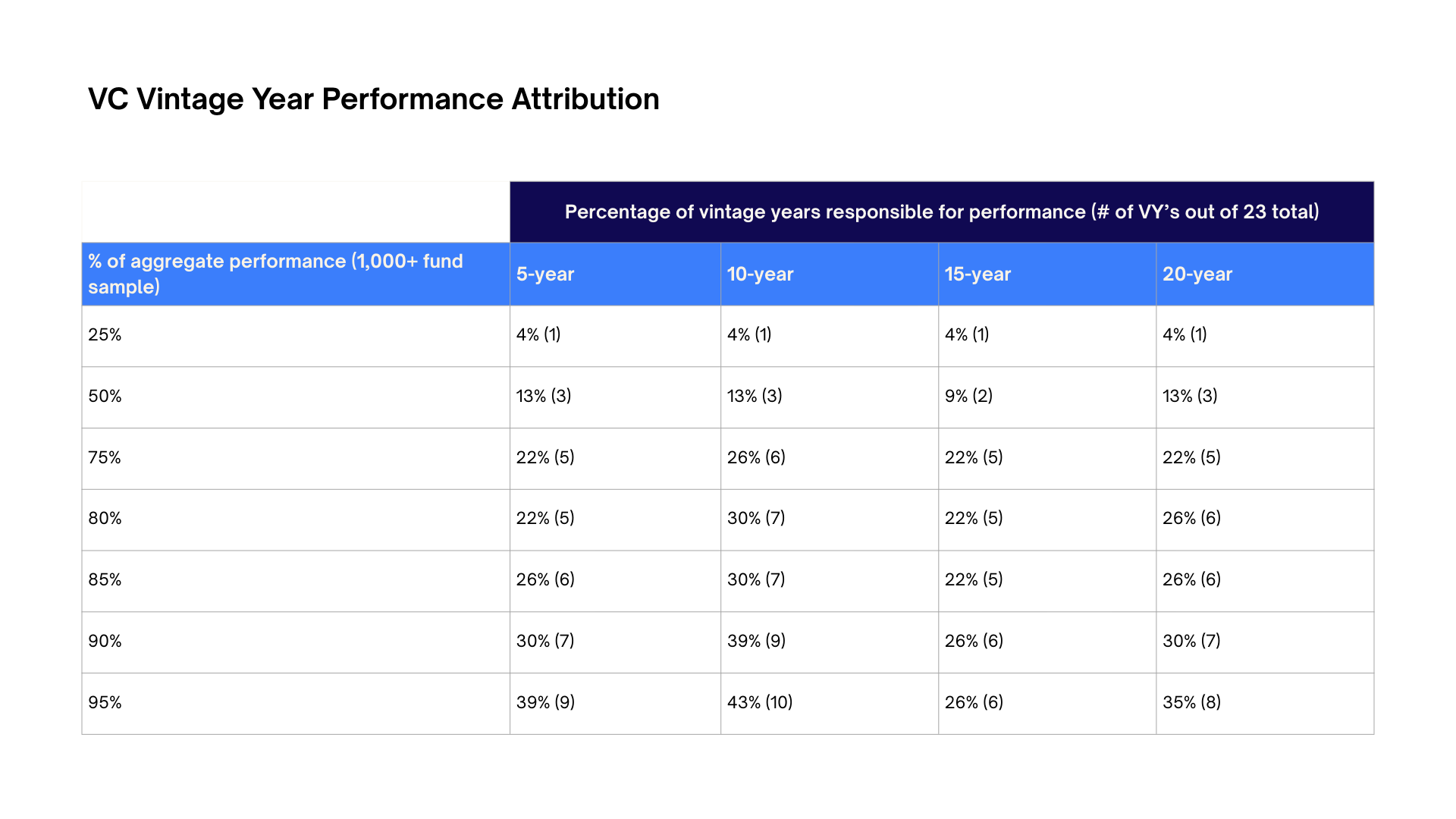

Vintage effects are most visible where return dispersion is extreme. In venture capital, outcomes follow a clear power law. Analysis by StepStone Group shows that roughly 80% of aggregate VC performance between 2000 and 2022 came from just 5–7 vintages out of 23.

A small handful of years end up doing most of the work for the asset class.

This does not mean every fund in those years performed well; only that the opportunity set widened dramatically in those vintages, allowing a few outcomes to dominate aggregate returns.

Miss them (or back the wrong managers in those years) and long-term outcomes may look materially different. The challenge, of course, is that these “golden” vintages are rarely obvious while they are forming.

Source: StepStone Analysis

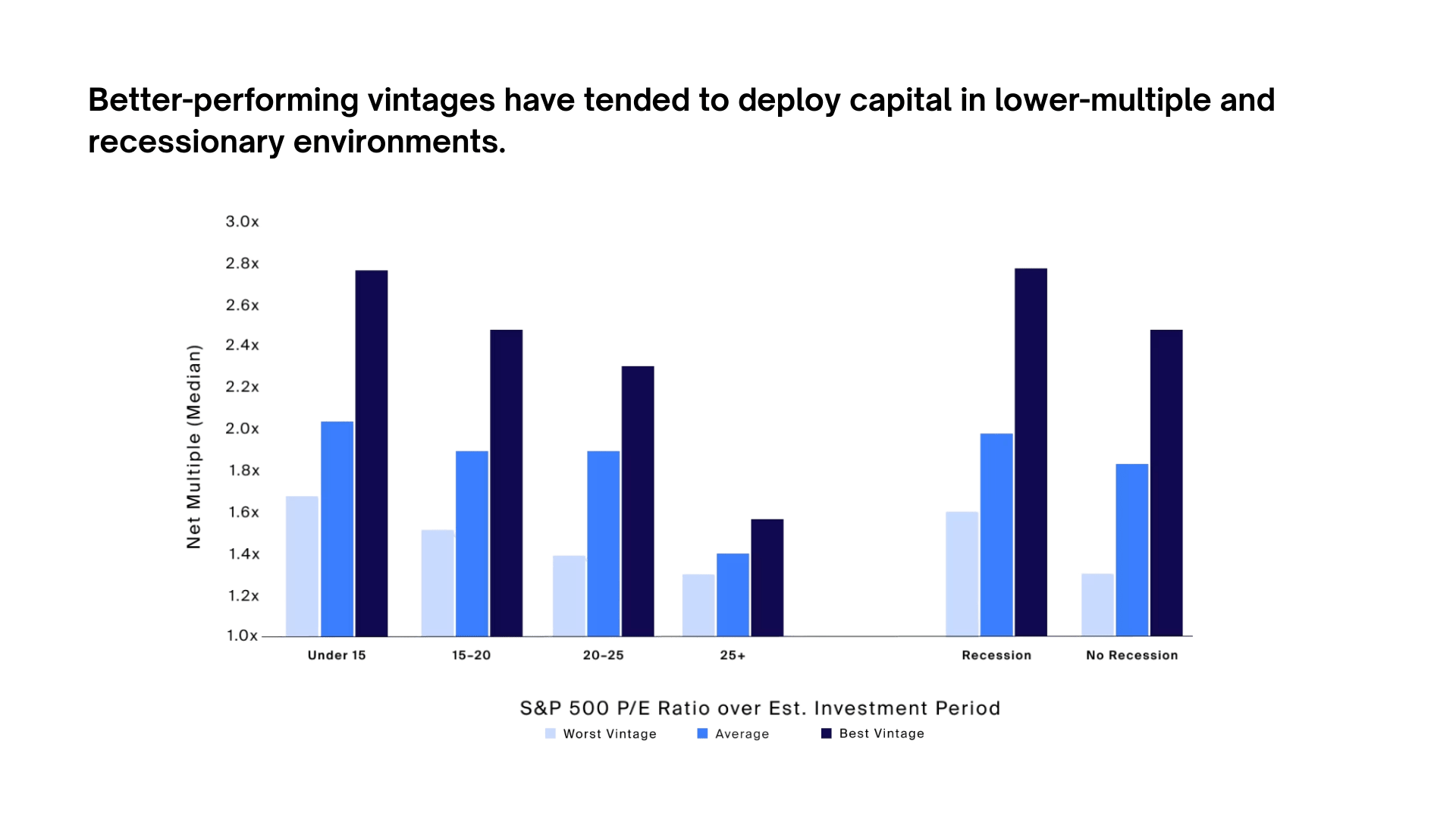

When vintages cluster around economic downturns, a counterintuitive pattern appears. Research shows that recession-year vintages, particularly those raised in 2001 and during the 2008–09 Global Financial Crisis, have historically produced higher net multiples than funds raised in the years leading up to those downturns.

These were not years investors rushed toward. Capital was scarce, financing constrained, and uncertainty was high. Yet those same conditions created lower entry prices and enforced discipline, which proved advantageous over long horizons.

In other words, the environment penalised comfort and rewarded restraint.

Source: CAIS

Recognising these patterns does not mean they are easy, or even particularly valuable, to exploit.

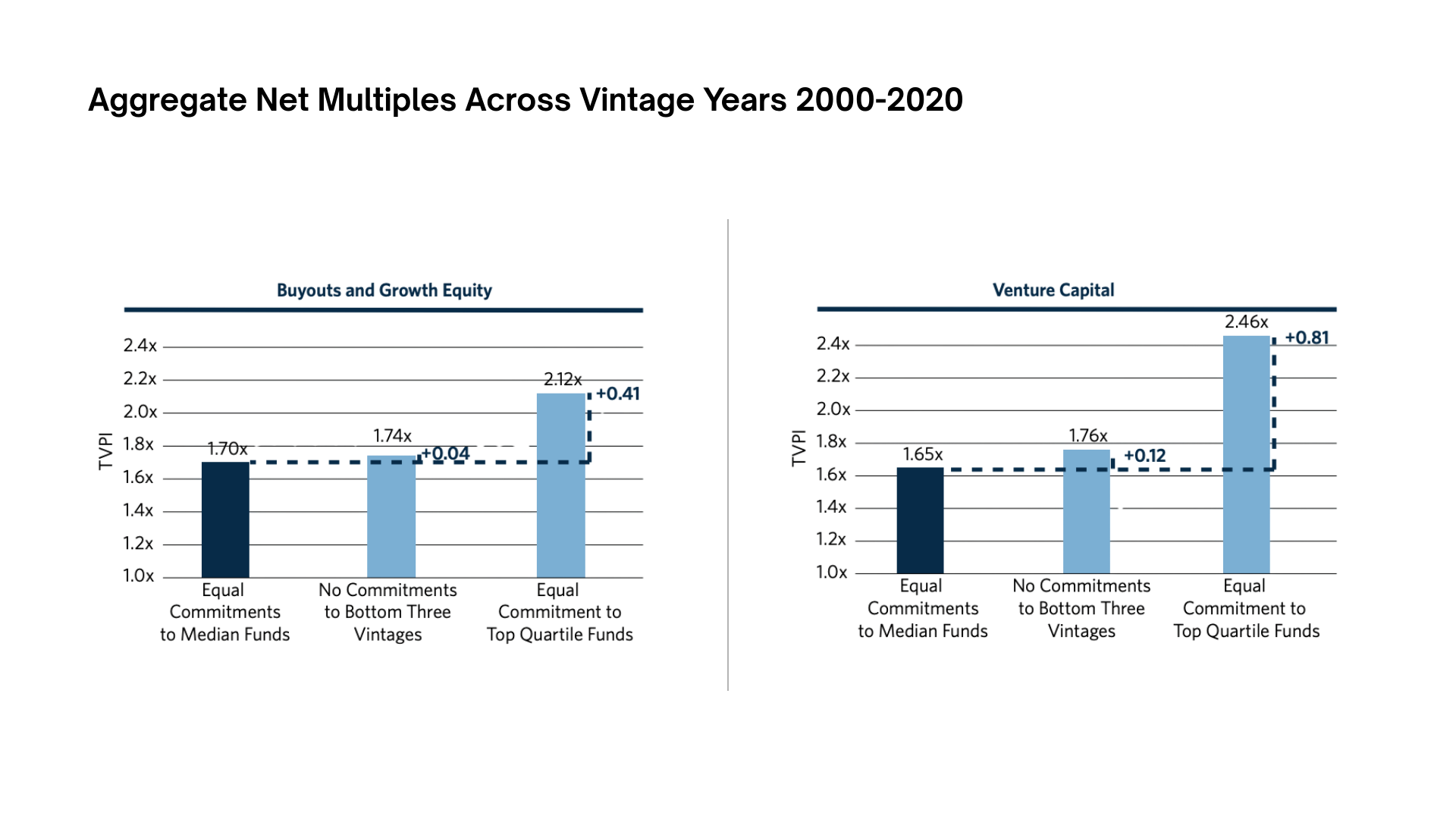

Commonfund’s analysis shows that even with perfect hindsight, the benefits of avoiding “bad” years are surprisingly small. An allocator who somehow skipped the three worst vintages between 2000 and 2020 would have improved total value only marginally, from roughly a 1.70x multiple to about 1.74x.

By contrast, consistent access to top-quartile managers lifted outcomes far more meaningfully.

This resolves the apparent contradiction: vintages shape the range of possible outcomes, but managers determine whether any of that dispersion is actually captured.

Vintages describe the environment; managers determine the result.

Source: commonfund

Over long horizons, behaviour tends to matter more than foresight.

Commonfund’s work on endowments shows that institutions with sustained allocations to private investments (typically above 20%) outperformed peers by around 70 basis points per year over a 25-year period.

The advantage did not come from clever timing, but from staying invested through difficult periods and maintaining pacing discipline.

Attempts to skip vintages often resulted in persistent under-allocation. Gaps of 2-4% that could last five years or more, even after efforts to catch up.

Vintage effects are real but they are blunt instruments. They describe conditions, not guarantees.

Within any given year, dispersion remains wide, driven by manager quality, sector exposure, and how capital is actually deployed.

Our work on vintages led us to a paradox.

The years that felt great while we were living through them – full of capital, optimism, and slick pitch decks – are rarely the years you’d pick if you could go back and buy the whole vintage. And the years everyone cursed on IC calls often turn out to be the ones that carry the portfolio.

To understand why, you have to look at the plumbing: how much capital was raised, how much was invested and at what valuations, and what was the market’s mood.

Globally. And in India.

In global buyouts, 2006–07 was the classic “great” stretch. Private equity fundraising finally pushed past the half-trillion mark. Leverage was cheap. Mega-deals set the tone. Entry multiples marched higher as everyone ran the same trade: financial engineering on top of a world of permanently low rates.

Venture got its own high-water mark in 2021. US VC funds raised around $168 billion, almost 1.9x 2020 and more than 2.5x the prior five-year average. Early-stage valuations jumped ~64% in a year while late-stage jumped ~93%. A hot IPO and SPAC window made those marks look sensible, until it didn’t.

India traced the same arc in fast-forward.

2019: PE deal value hit roughly $45 billion, ~70% higher than 2018 and more than 110% above the prior five-year average. India briefly became the second-largest PE deal market in APAC.

2021: total private-capital deal value reached about $53 billion, up 71% year-on-year across 1,100+ deals. VC alone was ~$38.5 billion (3.8x 2020) and, for the first time, more than half of all private capital. 44 unicorns were minted, more than China.

Everything that is supposed to be cyclical went vertical at the same time: fundraising, round sizes, unicorn count, exit value.

These years feel decisive. They dominate annual letters and conference panels. The instinct is to assume they are also the years that will carry the portfolio.

But look at what those inputs do to the starting point for returns:

None of that guarantees weak outcomes.

But structurally, these are difficult starting points. The very conditions that made the year feel powerful at the time are often the ones that compress future returns.

Now flip the lens to the years no one wanted to talk about.

Globally, 2001 and 2008–09 are the obvious markers. In both, public markets had just crashed and banks were shrinking balance sheets. LPs did what they always do: cut commitments and “wait for clarity”.

Preqin’s long-run data shows the 2001 PE vintage ended up as one of the strongest in more than two decades. CAIS’s analysis of the GFC period finds that funds raised in 2008–09 produced higher net multiples across buyout, venture, and real estate than the three vintages immediately before.

Fundraising was miserable. Deals were smaller, slower, and negotiated from a position of fear. Valuations and leverage terms reset.

If you were designing an environment purely for long-run IRR, it would look uncomfortably like that.

India’s “not-so-great” regimes follow the same script, with the caveat that India’s private-market history is shorter, and outcomes are still maturing.

Post dot-com and Ketan Parekh, capital became fearful and scarce. During 2008–09, deals slowed and exits were painful. Capital that did go to work bought roads, power, lenders and early consumer businesses at prices that look implausible today.

The most recent cycle makes the contrast explicit.

After the 2021 peak:

From an allocator’s lens, 2022–23 were textbook “not-so-great” years.

ICs were tired. GPs were fighting over terms. Founders were dragged back toward profitability.

By 2024, the market began to heal. Capital deployed went into cleaner cap tables, reasonable valuations, and thinner competition.

Those are precisely the conditions that tend to define strong vintages in hindsight because they compound well.

By late 2025, the label is printed, but the bottle is still young.

In India, the setup is constructive. PE–VC investments rebounded about 9% in 2024 to $43 billion. Exits hit a record $33 billion. In 2025, exit momentum has continued in a steadier, less theatrical way.

That sequencing matters. Capital returning before a fundraising surge tends to restore discipline rather than excess.

Globally, fundraising remains constrained. Commitments are still ~40% below the 2021 peak. But deal activity and exits have recovered enough to recycle capital without reigniting euphoria.

What could break this vintage is not obvious exuberance but interruption: a closed exit window, a sharp public-market derating, or a prolonged fundraising drought that starves deployment mid-cycle.

Absent that, the starting conditions look sound.

Seen through the lens of vintages, this is often how good years begin. The wine is being made in the cellar, not rushed to auction.

It doesn’t guarantee that 2025 will age well.

But stripped of mood and narrative, it looks far closer to the silent years that compound than the loud ones we spend a decade explaining.

With that, we’re at the final Unlisted Intel of 2025.

The dictionary word of the year was “rage bait”, and the year certainly wasn’t a quiet one. There wasn’t a single boring moment.

With time, 2025 may come to be seen as a strong vintage – one that set better foundations and left the ecosystem better prepared for what followed.

Thank you to everyone who read, shared, and engaged with Unlisted Intel this year.

We end 2025 sharper, more calibrated, and better positioned for the vintages ahead.

Here’s to an even better 2026.

Jai Hind 🇮🇳

TERMS OF USE

Thank you for your interest in our Website at https://unlistedintel.com/. Your use of this Website, including the content, materials and information available on or through this Website (together, the “Materials”), is governed by these Terms of Use (these “Terms”). By using this Website, you acknowledge that you have read and agree to these Terms.

NO OFFER, SOLICITATION OR ADVICE

Our site is provided for informational purposes only. It does not constitute to constitute (i) an offer, or solicitation of an offer, to

purchase or sell any security, other assets, or service, (ii) investment, legal, business, or tax advice, or an offer to provide such advice or (iii) a basis for making any investment decision.

The Materials are provided for informational purposes and have been prepared by Oister Global for informational purposes to acquaint existing and prospective underlying funds, entrepreneurs, and other company founders with Oister Global's recent and historical investment activities.

Please note that any investments or portfolio companies referenced in the Materials are illustrative and do not reflect the performance of any Oister Global fund as a whole. There is no obligation for Oister Global to update or alter any forward-looking statements, whether as a result of new information, future events, or otherwise.

PURPOSE LIMITATION AND ACCESS TO YOUR PERSONAL DATA:

We will only collect your personal data in a fair, lawful, and transparent manner. We will keep your personal data accurate and up to date. We will process your personal data in line with your legal rights. We use your name and contact details, such as email, postal address, and contact number to continue communications with you. We may also use your contact information to invite you to events we are hosting or to keep you updated with our news.

USE OF COOKIES OR SIMILAR DEVICES

We use cookies on our website. This helps us to provide you with a better experience when you browse our website and also allows us to make improvements to our site. You may be able to change the preferences on your browser or device to prevent or limit your device’s acceptance of cookies, but this may prevent you from taking advantage of some of our features.

MATERIAL

The material displayed on our site is provided “as is”, without any guarantees, conditions, or warranties as to its accuracy, completeness, or reliability. You should be aware that a significant portion of the Materials includes or consists of information that has been provided by third parties and has not been validated or verified by us. In connection with our investment activities, we often become subject to a variety of confidentiality obligations to funds, investors, portfolio companies, and other third parties. Any statements we make may be affected by those confidentiality obligations, with the result that we may be prohibited from making full disclosures.

MISCELLANEOUS

This Website is operated and controlled by Oister Global in India. We may change the content on our site at any time. If the need arises, we may suspend access to our site, or close it indefinitely. We are under no obligation to update any material on our site.

CONTACT INFORMATION

Any questions, concerns or complaints regarding these Terms should be sent to info@oisterglobal.com