Unpacking India’s VC/PE market as it moves into a more advanced phase of its evolution

Dear Reader,

I want to start this month’s newsletter with two images.

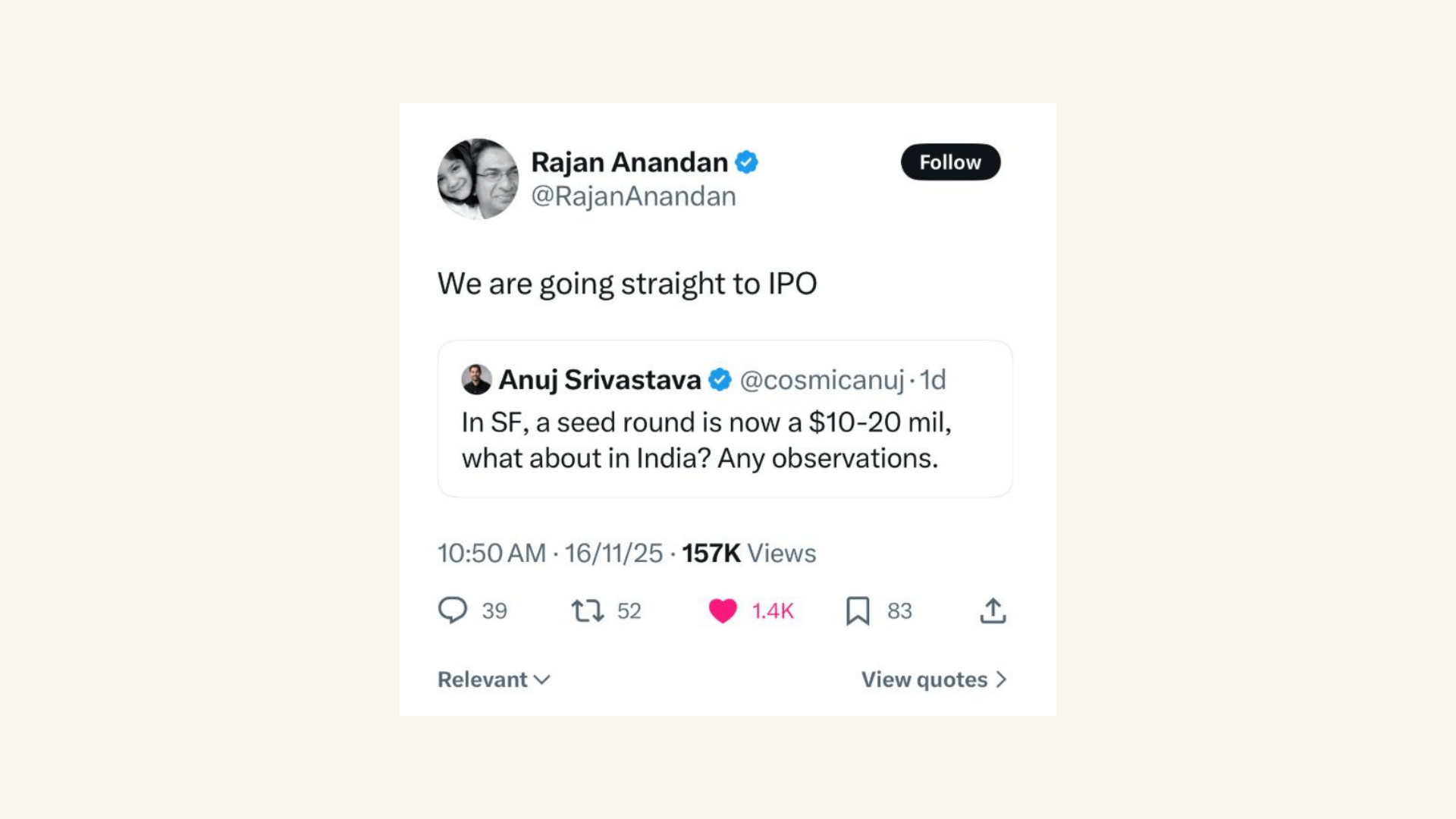

First is this tweet quote by Rajan.

Second is this clip from this Monday’s Economic Times.

The tweet captures the sentiment pulsing through India’s VC/PE ecosystem right now. The clipping shows the scale of what’s actually happening. And yes, we’ve all become somewhat numb to big numbers, but even then, this one is big: the 2025 startup IPO rush (Ather, BlueStone, Lenskart, Urban Company, Groww, Pine Labs) has already delivered about $1.6 billion of cash exits to VCs through OFS. That’s staggering by any standard.

What’s even more interesting is what sits beyond the cash. Investors still hold over $8 billion in mark-to-market value across these companies, powered by strong post-listing performance. That tells a deeper story.

By now, you’ve probably read enough debriefs and deal-room takes on what’s happening in India’s VC/PE ecosystem. But I keep coming back to that tweet, and it raises a simpler, more fundamental question:

How mature are we, really?

I’ve been racking my brain about this for a while now speaking to founders, investors, LPs, absorbing the noise and the nuance, and trying to make sense of what this moment actually means. And the more I thought about it, the clearer it became that “maturity” is not so simple. It’s layered.

If the global VC/PE universe were a three-hour film, India is well past the opening credits. The pioneer years are behind us; the early chaos has thinned; we’re somewhere around minute 45 now, the part where the story settles, the characters sharpen, and the stakes start to become real.

Or here’s another comparison: if India’s private markets were human, they’d be in their mid-20s. Very energetic, self-aware, still learning, and finally beginning to show real, repeatable promise.

But metaphors aside, here’s the hypothesis that emerged from all that thinking:

A mature VC/PE market is one where capital is abundant, exits are predictable, governance is institutional, and outcomes repeat across cycles.

That’s the lens we used when we went back to the numbers. And here’s what they revealed.

The data reflects exactly this point in the script. India’s private capital market crossed roughly $43 billion in PE–VC deal value in 2024, a 9% recovery from the previous year. Over 1,600 transactions were recorded, placing India solidly as the second-largest PE–VC destination in Asia-Pacific, ahead of every market except China. This is not the statistical profile of a young market. It’s the signature of an ecosystem that has built muscle memory.

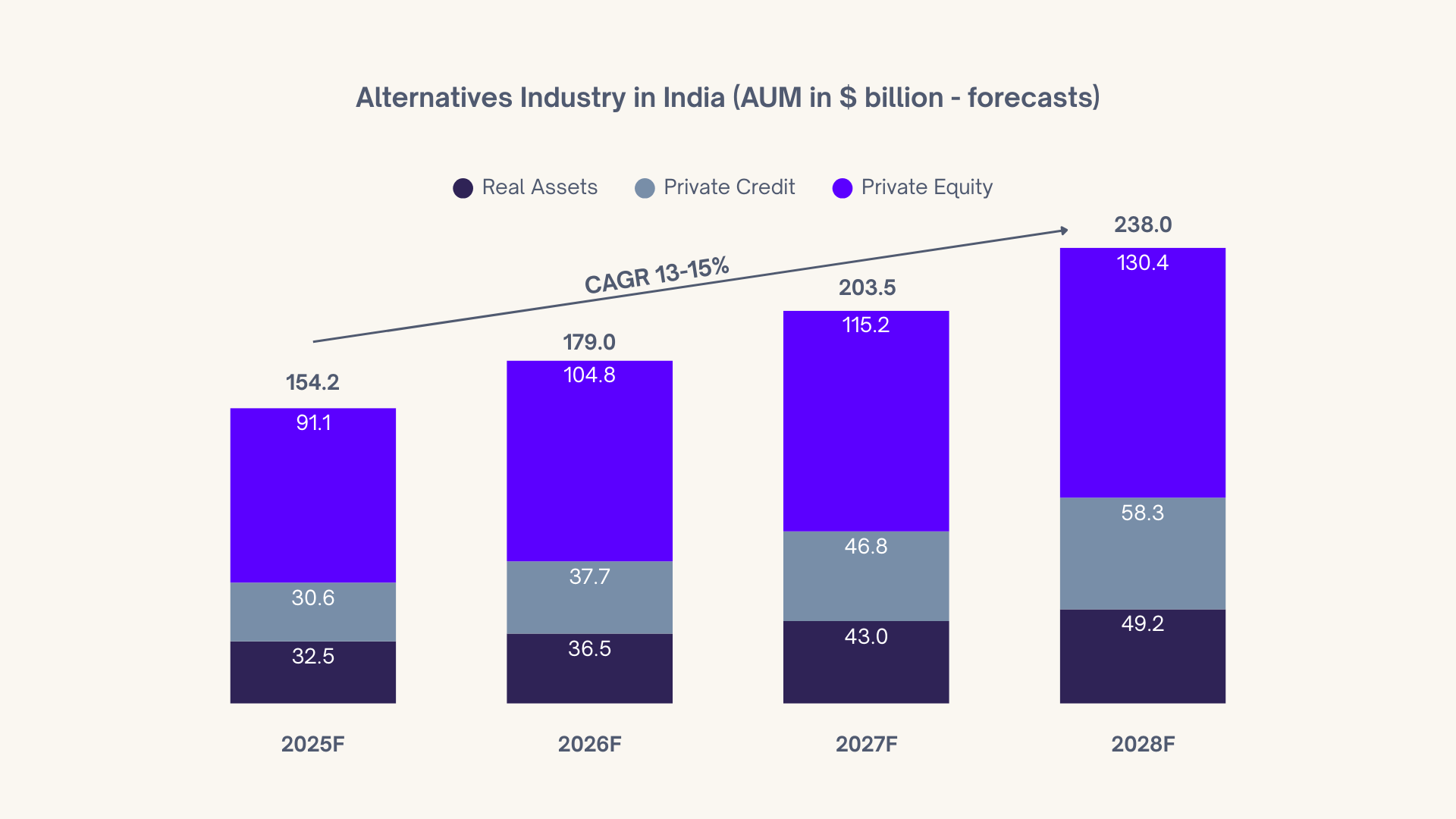

Size of market : The AUM of Indian alternative industry is expected to reach $238 bn by the year 2028 from $131 bn in 2022. Between 2024 and 2028, the industry is expected to record a CAGR of around 13-15%.

Chart Title: Alternatives Industry in India (AUM in $ billion – forecasts)

Source: CareEdge. (2024, December). ‘Industry Research Report on Alternatives’

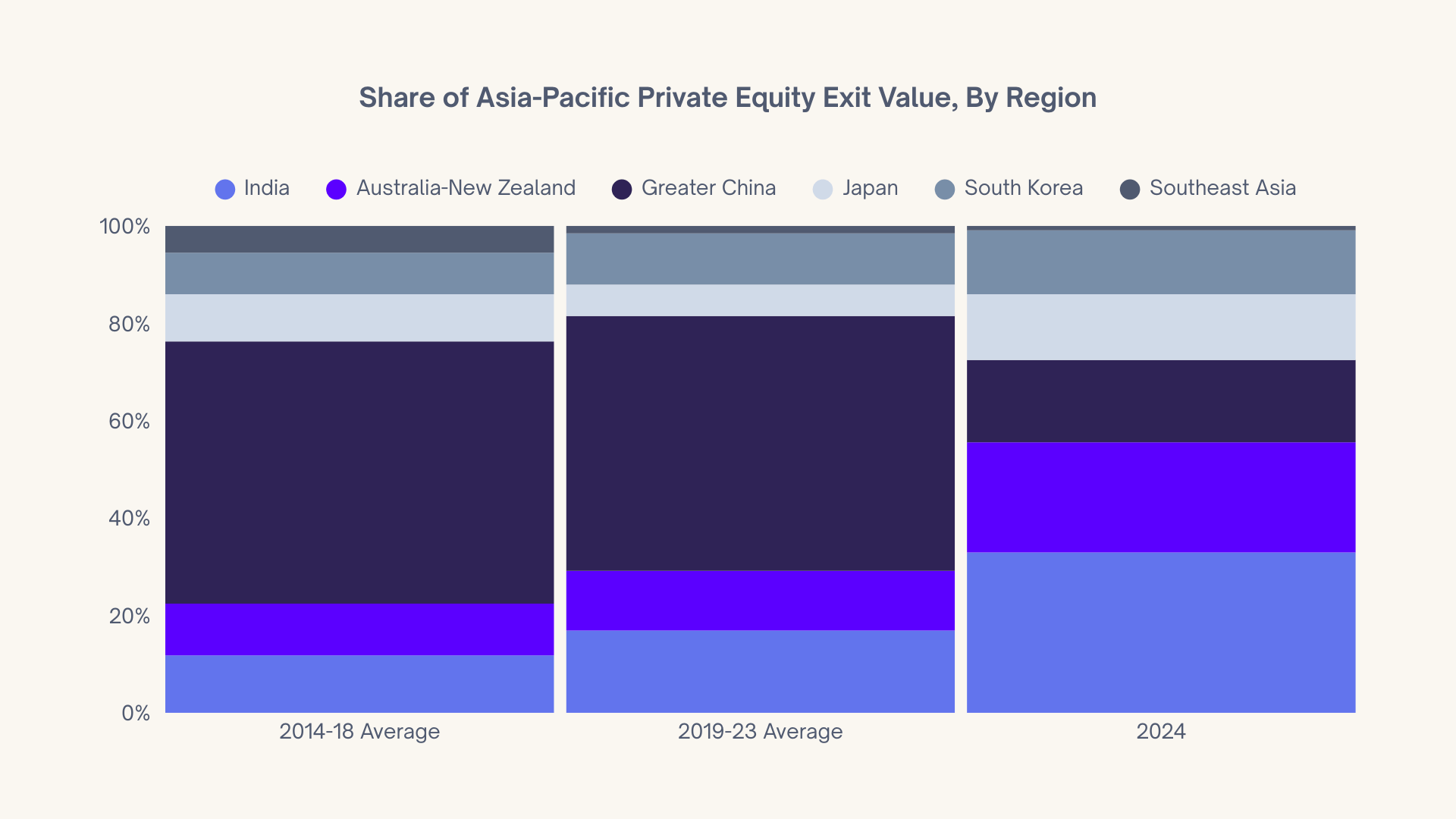

Exits: India’s share of exit value rose sharply in 2024. India was Asia Pacific’s largest exit market in 2024 in terms of value and count.

Chart Title: Share of Asia-Pacific Private Equity Exit Value, By Region

Source: Bain ‘Asia-Pacific Private Equity Report 2025’

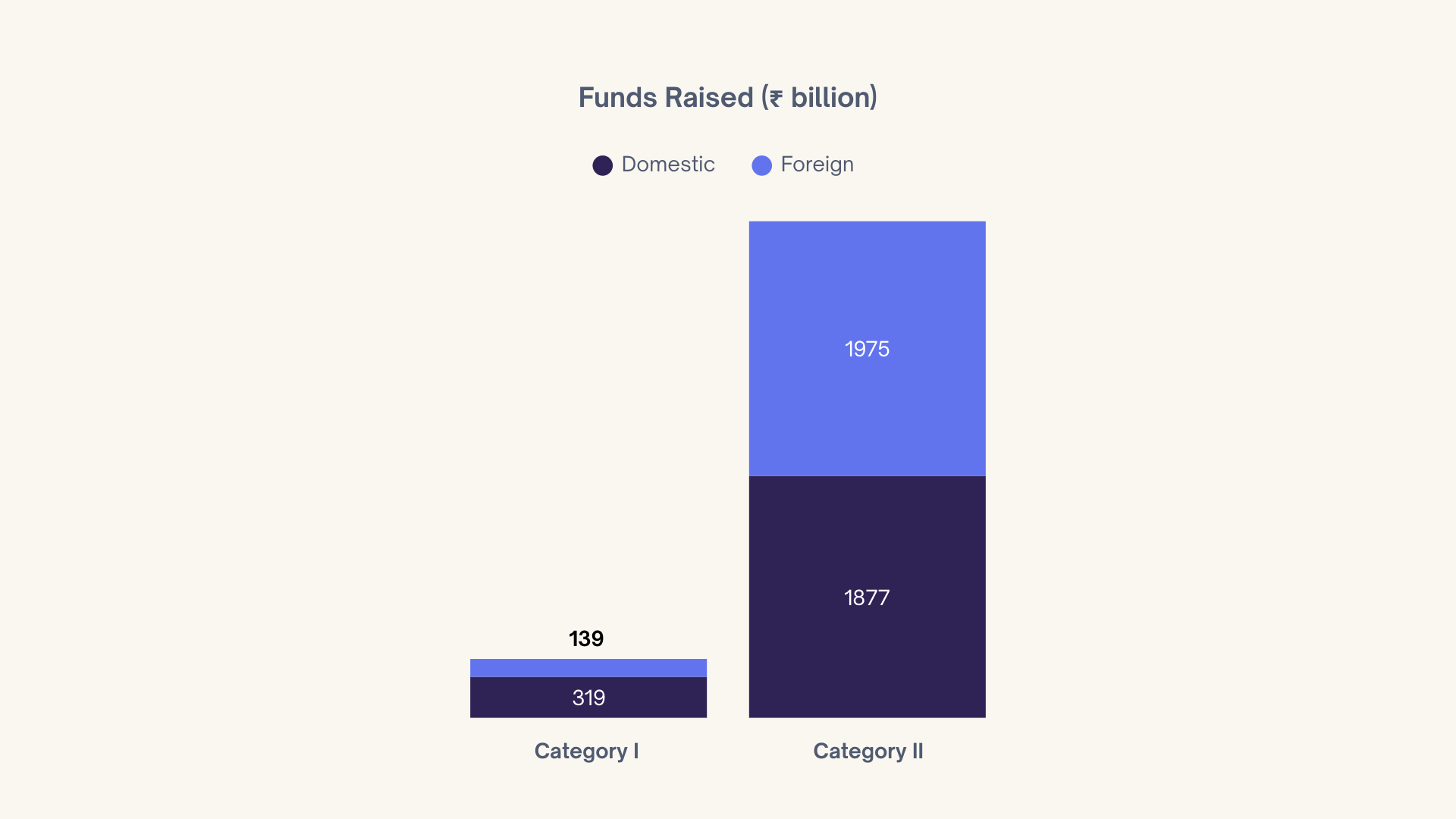

Domestic capital rising: As per data from SEBI, as of September 2024, domestic investors accounted for ~51% of gross funds raised across Category I and II AIFs.

Chart Title: Funds Raised (₹ billion)

Source: CRISIL and Oister Global Report, ‘No ifs about AIFs 2.0’

Better segmentation: At the same time, the market has segmented. We now have:

In 2024, India deployed across distinct strategies – $16.8 billion in buyouts, $13.4 billion in growth, $10.8 billion in private credit, $10 billion in start-ups, and $5 billion in PIPE.

In terms of sectoral allocation, infrastructure, financial services, real estate, e-commerce, technology, and life science, recorded more than 100 deals each in 2024 (compared to just two sectors reaching this milestone in 2023) and collectively accounted for 80% of total investments by value and 66% by deal volume. This opens up the opportunity for sector-focused managers rather than generic growth funds.

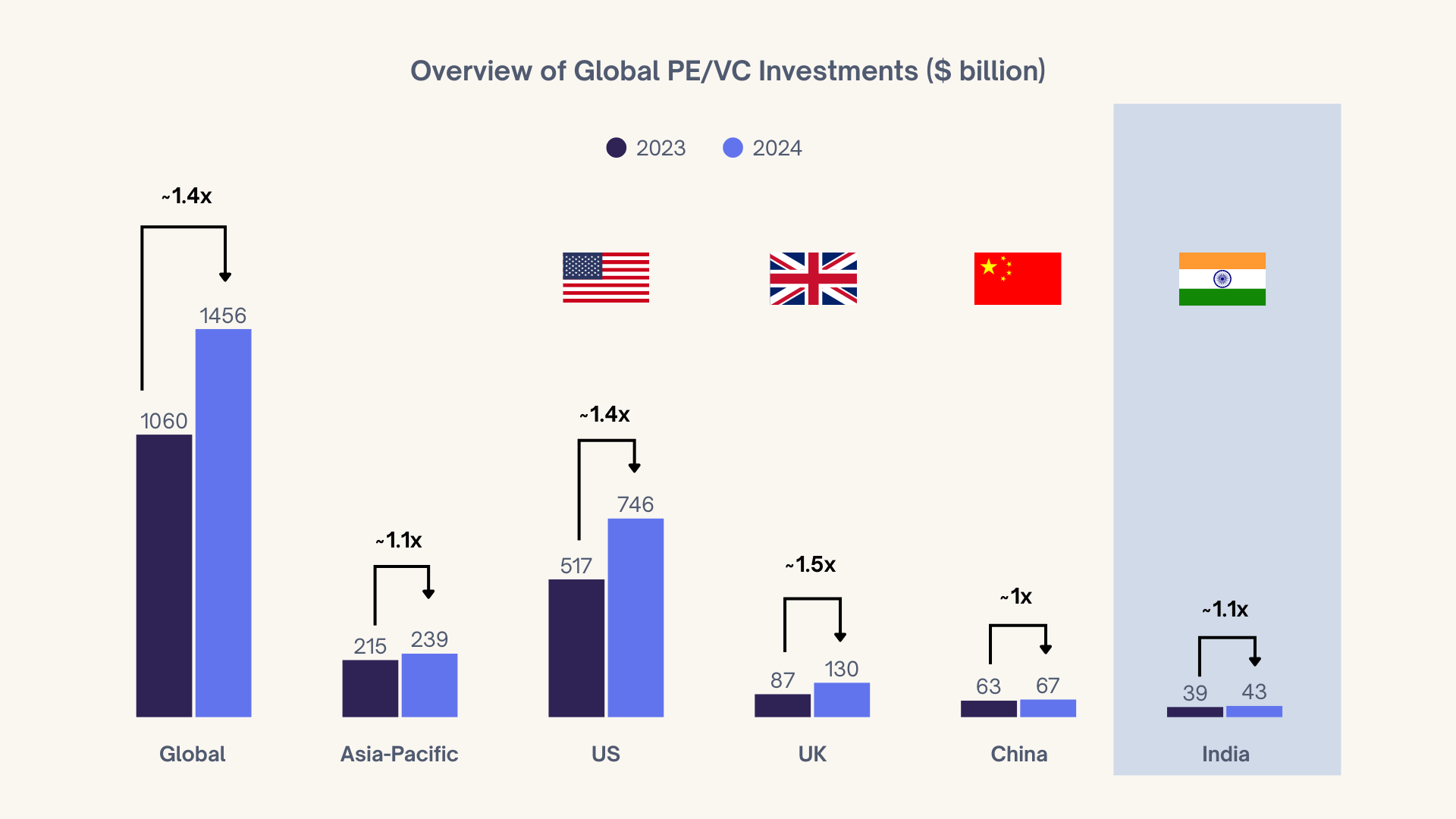

Not US/China yet

In 2024, global PE-VC investment grew ~40% from about $1.06 trillion to $1.46 trillion, led by the US and the UK, while Asia-Pacific as a whole grew a more modest ~1.1x. India tracked that regional pattern: PE-VC investments rose ~9% from $39B to $43B, slower than the global rebound, but enough to firmly hold its position as Asia-Pacific’s second-largest destination after China.

Chart Title: Overview of Global PE/VC Investments ($ billion)

Source: Bain ‘India Private Equity Report 2025’

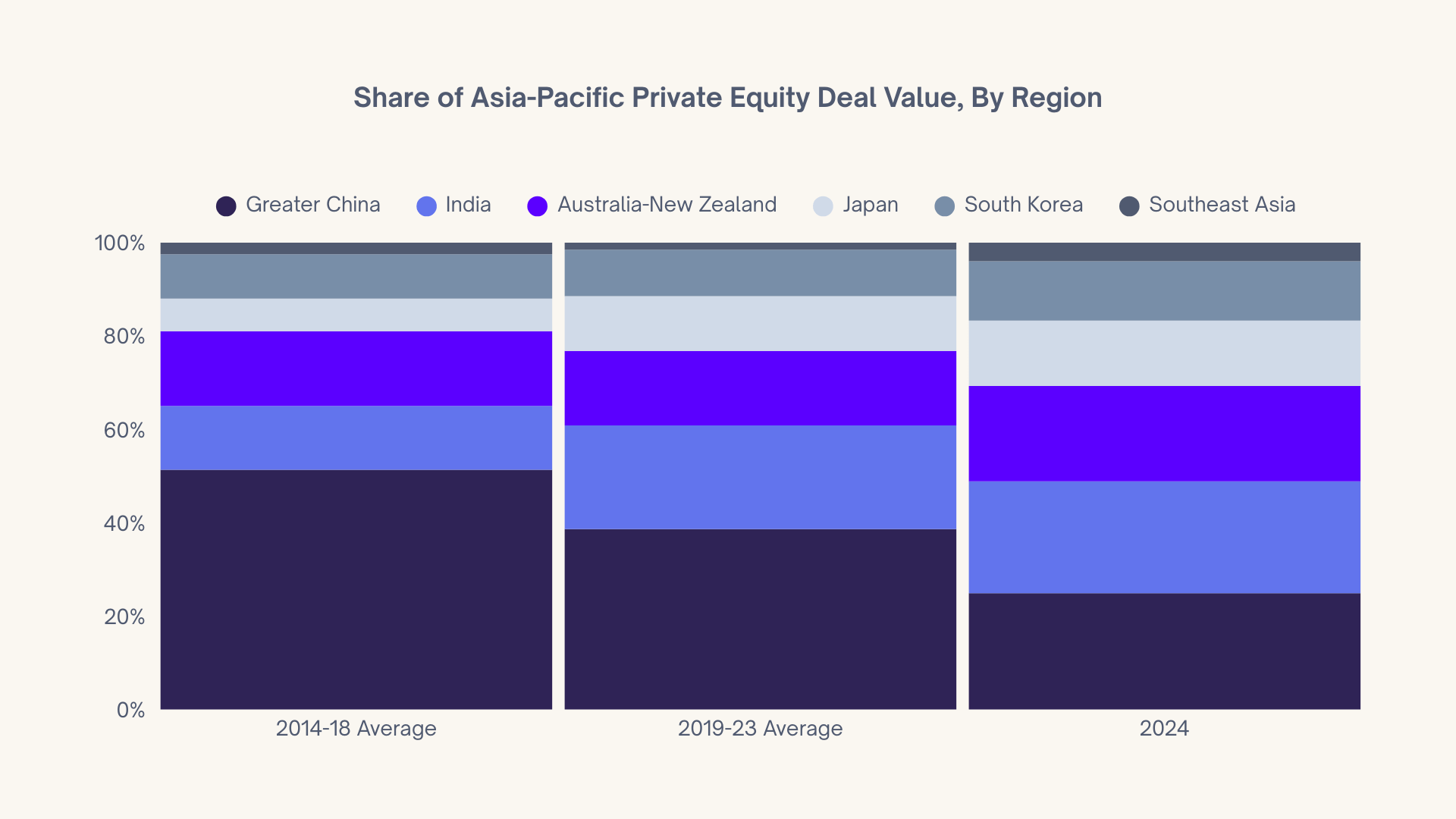

But far ahead of many other markets

Within Asia-Pacific, India has pulled away from the rest of the pack. Over the last decade, its share of regional PE deal value has steadily increased, even as Greater China’s has slipped, and by 2024 India clearly stands as the second-biggest market in the region, well ahead of Japan, South Korea, and Australia–New Zealand.

Chart Title: Share of Asia-Pacific Private Equity Deal Value, By Region

Source: Bain ‘Asia-Pacific Private Equity Report 2025’

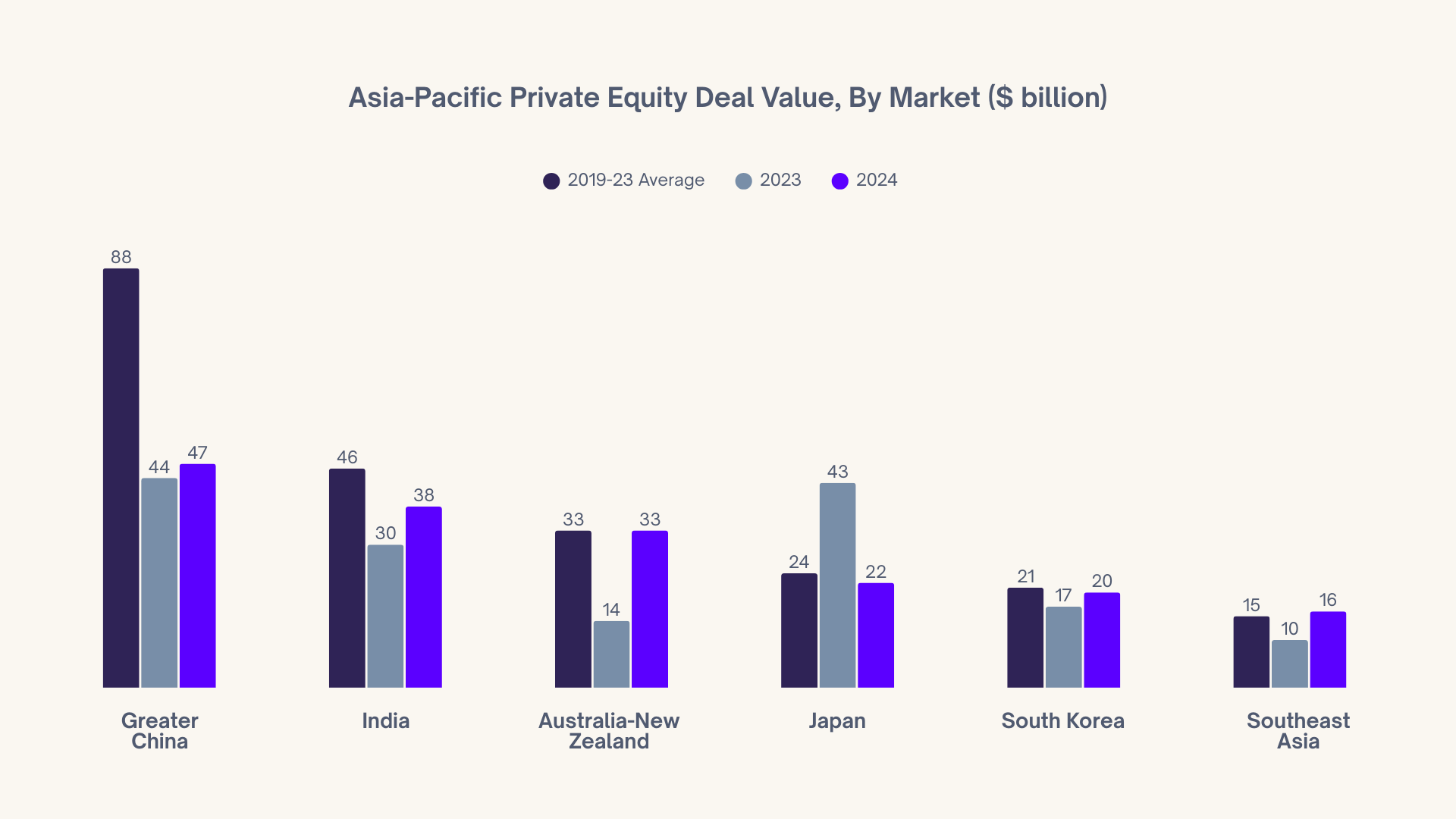

India is young by years, mature by outcomes

India was the only market in Asia-Pacific to post double-digit growth in both PE deal value and deal count in 2024: investments climbed from $30 billion in 2023 to $38 billion in 2024, even as Greater China, Japan, South Korea and Southeast Asia all sat below or around their 2019–23 averages.

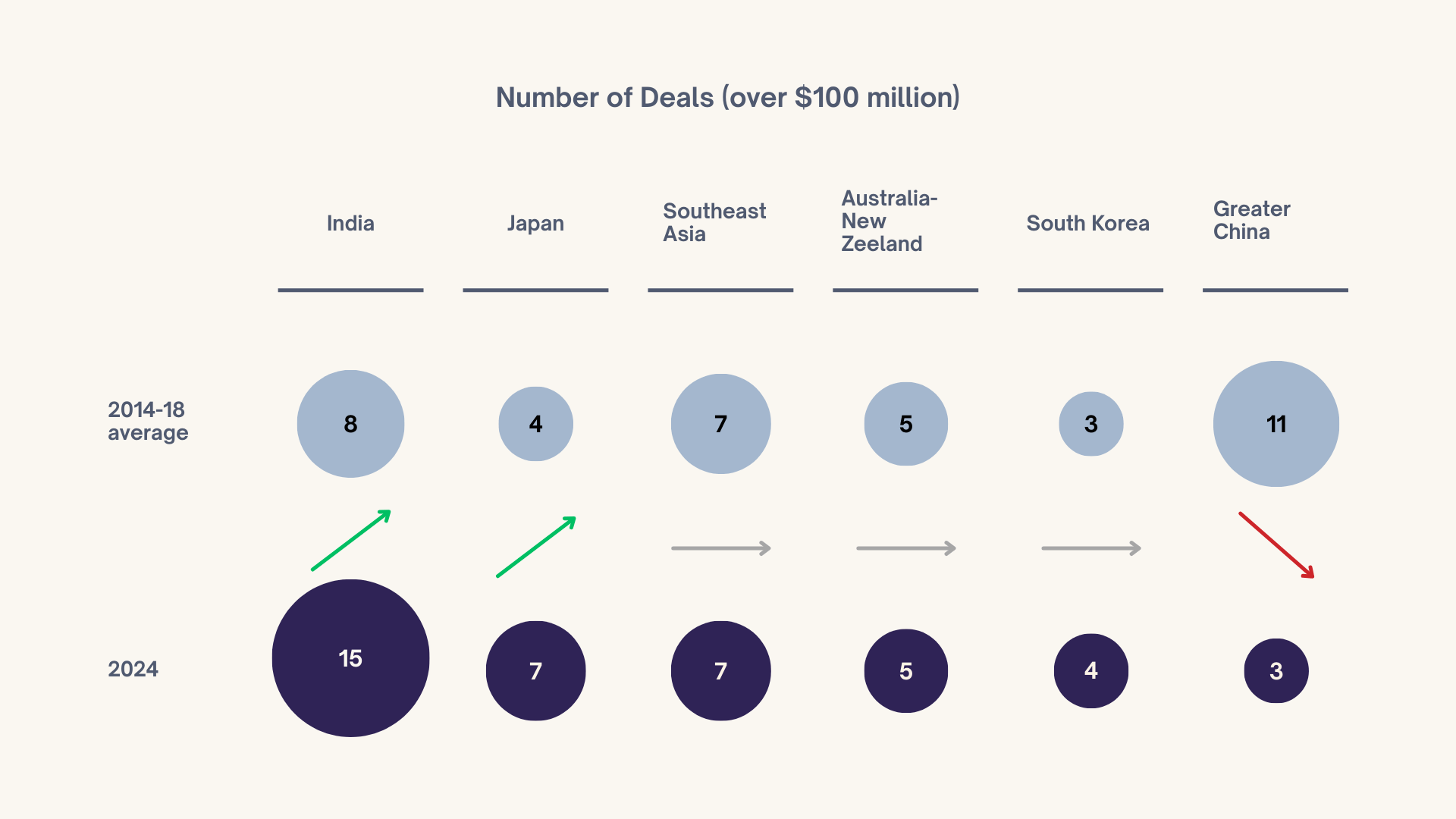

At the same time, leading global GPs are concentrating their big cheques in India: $100m+ deals in India rose from an average of 8 (2014–18) to 15 in 2024, while comparable deals in Greater China dropped from 11 to just 3, and stayed flat or barely up in the rest of the region.

Chart Title: Asia-Pacific Private Equity Deal Value, By Market ($ billion)

Source: Bain ‘Asia-Pacific Private Equity Report 2025’

Chart Title: Number of Deals (over $100 million)

Source: Bain ‘Asia-Pacific Private Equity Report 2025’

No ecosystem matures without its own set of gaps. The presence of these gaps precisely tells you there’s meaningful headroom ahead. India’s no different. Three areas stand out.

Exits work, but the mix needs to widen.

IPOs have delivered, no question. But beyond public markets, the exit toolkit is still shallow. Secondary sales, GP-leds, and sponsor-to-sponsor exits haven’t scaled to where they should be in a $4+ trillion economy.

Early-stage density outside the top corridors

VC recovery has been healthy in the aggregate, but deal flow is still heavily skewed towards certain sectors and metros. Beyond consumer tech, SaaS, and fintech, the pipeline in climate, deep tech, manufacturing, and frontier sectors remains thinner than it should be for a $4+ trillion economy.

Long GP track records

Many of India’s GPs have not yet seen three or four full cycles through from entry to exit. First- and second-time funds still make up a meaningful share of the landscape, which means track-record depth is a work in progress.

Based on data from CRISIL and Oister Global’s report No ifs about AIFs 2.0, a sample of 279 Category I and II funds shows that about 56% are managed by first-time investment managers, 20% by second-time managers, and only 24% by managers that have launched three or more funds. Even in the last three vintages alone, roughly 44% of all managers coming to market were first-time GPs – evidence of strong entrepreneurial energy, but also a reminder of how early we still are in building long, multi-cycle GP track records.

So what does all this mean for investors sizing up the next decade? India’s trajectory is its own, so here’s our humble take, and it tends to fall into four clear buckets.

What strengthens: India’s domestic capital pools are only getting deeper with mutual funds, insurers, pensions, and soon alternatives, while control deals, cleaner governance, and real sector depth in financials, healthcare, consumer, and infra start to show up with scale.

What still needs time: dependable exits beyond IPOs, truly deep early-stage ecosystems outside the usual hubs, and GP franchises that mature into real institutions with multi-cycle credibility and succession.

What will differentiate India: a rare blend of growth, scale, and improving governance, a domestic bid that can actually underwrite exits, and a buyout/secondaries opportunity set shaped by decades of founder-led, under-institutionalised businesses finally reaching transition points.

And why this moment matters: because the next decade is about proving India can compound consistently, across vintages and cycles. That’s what entering the compounding phase really means.

India is moving along a maturity curve of its own, shaped by two forces that make this moment fundamentally different.

First: the domestic bid arrived early.

In most markets, deep domestic public-equity pools and broad retail participation come long before private markets and venture-backed IPOs really scale. In India, that gap has been unusually narrow. By the time this startup IPO wave arrived, mutual funds, SIP culture, and direct retail participation were already a meaningful share of secondary-market demand.

Second: policy and prudence have acted as invisible scaffolding.

India’s regulatory ecosystem gets plenty of criticism for being conservative and process-heavy. Some of that is deserved. But that conservatism has also built a fairly strong spine: disclosure-heavy listing rules, tighter related-party scrutiny, greater expectations from auditors and independent directors, and a regulator that is increasingly willing to intervene. All this has forced private markets to professionalise faster than many peers. Our curve is hence defined by a rising floor. Better governance, better quality, better repeatability.

Put simply: India is no longer a market defined by possibility alone. We’re entering a phase where outcomes are becoming repeatable, where capital cycles feel familiar, and where governance is becoming a norm, not an aspiration. We’re not fully mature, not yet, but we’re well past the introductions. If the last decade proved we could build, the next will prove we can sustain, exit, and repeat across vintages, sectors, and cycles.

India’s private markets are stepping into their adult years. And like adulthood, it brings stronger confidence, clearer expectations, and a better understanding of what really matters. We may still be at minute 45 of the three-hour film, but the plot is now in motion, the characters are defined, and the direction is unmistakable.

Jai Hind

TERMS OF USE

Thank you for your interest in our Website at https://unlistedintel.com/. Your use of this Website, including the content, materials and information available on or through this Website (together, the “Materials”), is governed by these Terms of Use (these “Terms”). By using this Website, you acknowledge that you have read and agree to these Terms.

NO OFFER, SOLICITATION OR ADVICE

Our site is provided for informational purposes only. It does not constitute to constitute (i) an offer, or solicitation of an offer, to

purchase or sell any security, other assets, or service, (ii) investment, legal, business, or tax advice, or an offer to provide such advice or (iii) a basis for making any investment decision.

The Materials are provided for informational purposes and have been prepared by Oister Global for informational purposes to acquaint existing and prospective underlying funds, entrepreneurs, and other company founders with Oister Global's recent and historical investment activities.

Please note that any investments or portfolio companies referenced in the Materials are illustrative and do not reflect the performance of any Oister Global fund as a whole. There is no obligation for Oister Global to update or alter any forward-looking statements, whether as a result of new information, future events, or otherwise.

PURPOSE LIMITATION AND ACCESS TO YOUR PERSONAL DATA:

We will only collect your personal data in a fair, lawful, and transparent manner. We will keep your personal data accurate and up to date. We will process your personal data in line with your legal rights. We use your name and contact details, such as email, postal address, and contact number to continue communications with you. We may also use your contact information to invite you to events we are hosting or to keep you updated with our news.

USE OF COOKIES OR SIMILAR DEVICES

We use cookies on our website. This helps us to provide you with a better experience when you browse our website and also allows us to make improvements to our site. You may be able to change the preferences on your browser or device to prevent or limit your device’s acceptance of cookies, but this may prevent you from taking advantage of some of our features.

MATERIAL

The material displayed on our site is provided “as is”, without any guarantees, conditions, or warranties as to its accuracy, completeness, or reliability. You should be aware that a significant portion of the Materials includes or consists of information that has been provided by third parties and has not been validated or verified by us. In connection with our investment activities, we often become subject to a variety of confidentiality obligations to funds, investors, portfolio companies, and other third parties. Any statements we make may be affected by those confidentiality obligations, with the result that we may be prohibited from making full disclosures.

MISCELLANEOUS

This Website is operated and controlled by Oister Global in India. We may change the content on our site at any time. If the need arises, we may suspend access to our site, or close it indefinitely. We are under no obligation to update any material on our site.

CONTACT INFORMATION

Any questions, concerns or complaints regarding these Terms should be sent to info@oisterglobal.com