The innovations and trends in the US financial markets have usually seen their delayed echoes in other parts of the world. One such innovation is the secondary market for private investments. ‘Secondaries’ as an asset class became mainstream in the US in 2000s and reached the global transaction volume of over $160 billion in 2024. LP-led deals accounted for more than 50% of this transaction volume, highlighting the utility of this asset class for investors looking for liquidity in the otherwise illiquid private investment space.

Now, it is time for India to get excited about secondaries. The last few years have seen the emergence of secondaries as a popular asset class and as one of the favorite topics among the leaders of the private investment industry in India. And it is only natural that this has taken steam lately. Startups saw a rise in India about a decade ago and many VC funds that capitalized on the opportunity by launching 10-year funds now need an exit. But are these companies IPO- ready yet? Likely not.

Secondaries emerged as the alternative exit path and everyone wants to now explore the potential of a ‘liquidity providing machine’ in a space which has been branded as illiquid.

If we study the history and growth of secondaries, a prominent factor that has led to the need and emergence of the secondaries ecosystem is the growth of the overall market that supplies secondary transactions, i.e., the private investment market. It is thus imperative to briefly look at the size and growth trends of the private markets.

“A thriving private market is the perfect breeding ground for secondaries.”

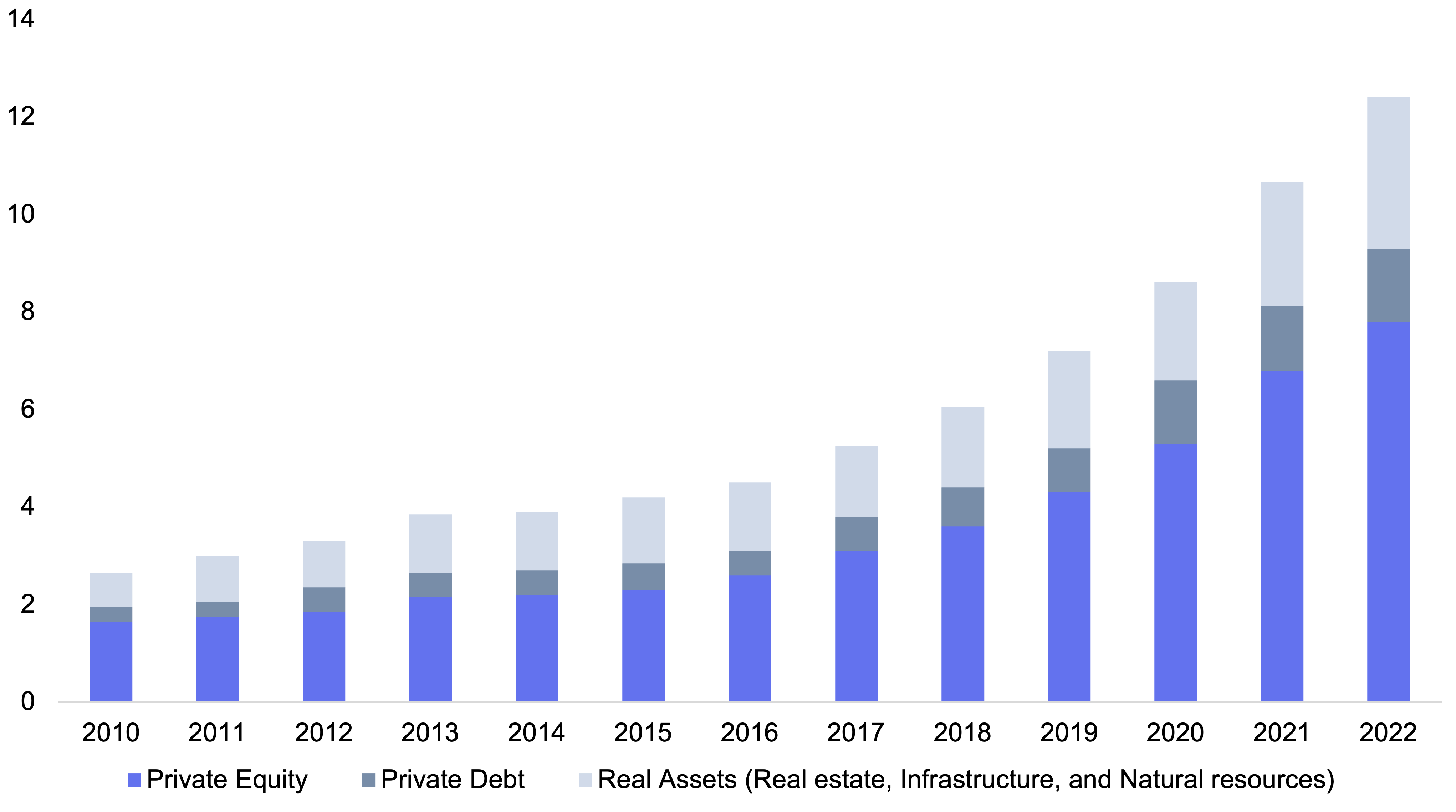

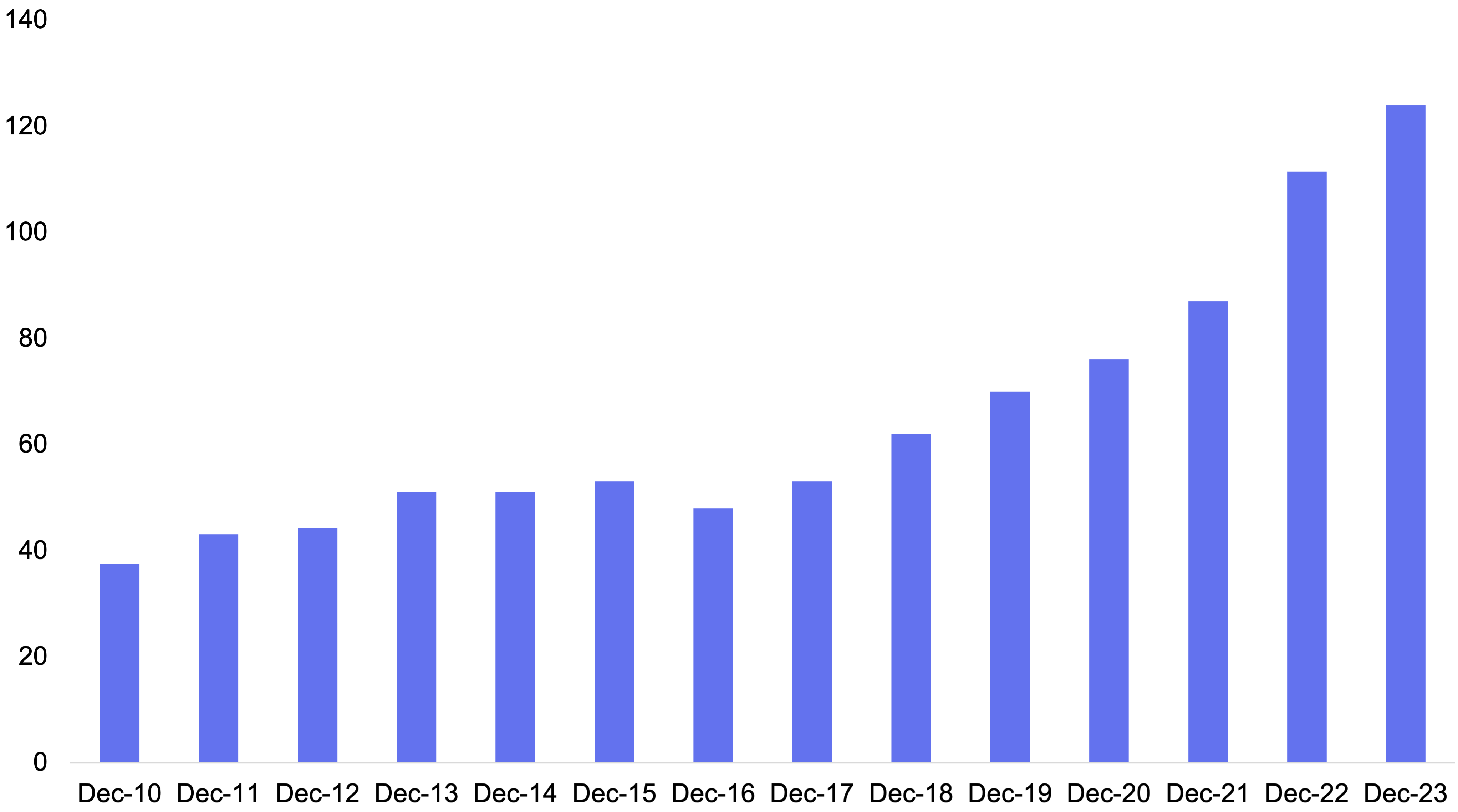

As per a report by McKinsey & Company, global private markets assets under management (AUM) grew annually by 20% between 2018 and 2023 to reach $13 trillion. As we see in figures 1 and 2, the private markets have grown considerably in size since 2010 both globally and in India.

Figure 1: Global AUM in private markets

Source: Preqin

Figure 2: India-focused private capital funds’s AUM

Source: Preqin

This growth in private markets is expected to continue at a healthy and rapid pace, especially in India, owing to the country’s favourable economic conditions and growth potential. A significant driver of this growth will be the vibrant start-up ecosystem of India. Indian startups have received a total funding of more than $150 billion in the last ten years (starting 2014). As per Indian government’s website (startupindia.gov.in), India’s startup ecosystem is the third largest in the world and is poised to grow at a rate of 12-15% annually over the next five years. This, coupled with the robust demand of Indian private equity and venture capital funds by domestic and foreign investors alike, will continue to drive the growth of the private markets in India.

A direct implication of this development in the private markets is the materialization of a robust secondary market – a trend seen in the US as well. As the private markets grew in size and started growing rapidly in the US, the need for a secondary market grew as well.

While we continue to highlight the importance of secondaries, a crucial point that cannot be missed is the fact that secondaries market volume of about $160 billion makes up only around 1% of the global private markets’ AUM of $13 trillion. The scope of this asset class, especially given its flexibility to provide liquidity as well as portfolio management tools for both LPs and GPs, place it at a unique position with many tailwinds that may help it soar to great heights. India still has a long way to go to reach the AUMs seen in the US but the private space in India has been growing steadily and warrants the need to be prepared with innovative solutions for the forthcoming trends and issues. Since US did it first and has successfully created the secondaries market, it is a valuable exercise to study the US markets and gather insights on how this asset class has done in the US over the last couple of decades. This will help us draw comparisons with the Indian market and comment on the expected trajectory of secondaries in India.The inception of secondaries: Dayton Carr is credited with executing the first ever secondaries deal in the US in 1979 when one of his friends needed to exit his stakes in some VC funds. What happened as a help to his friend gave Carr a taste of the attractiveness of this type of transaction – exposure to sound assets at a discount, higher diversification, shorter fund duration, faster returns, and more transparency into the portfolio’s holdings as compared to the LPs who made initial commitments into the fund. This led to him starting world’s first secondaries fund – Venture Capital Fund of America (VCFA) – in 1982.

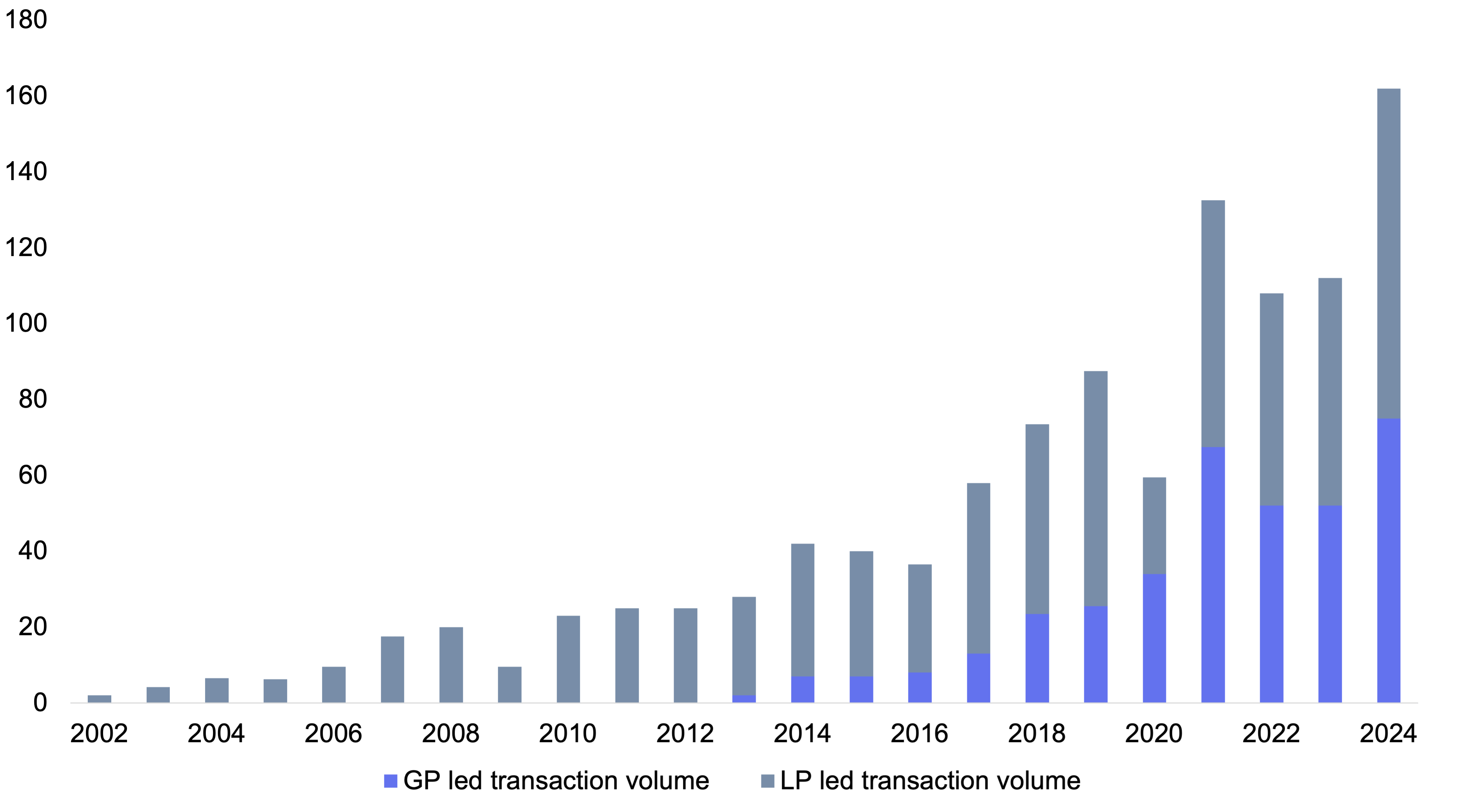

The origin story indicates that LP-led secondaries were the majority (if not the entire) part of what made up the secondaries market. As we can see in Figure 3, global secondaries transaction volume consisted entirely of LP-led deals until 2012 when the overall transaction volume had reached $25 billion. This is important to highlight because of the following two reasons:

Figure 3: Global secondaries transaction volume

Source: Evercore FY 2024 Secondary Market Review – Highlights

Another trend that marks the story of secondaries in the US and globally in the recent times is the growing popularity of GP-led single-asset transactions. As evident in figure 3 above, the volume of GP-led deals has seen a robust growth in the recent years as the GPs bet on their best assets and continue to hold them in continuation vehicles. What was a non-existent area just ten years ago now constitute about 50% of the total secondaries transaction volume – a substantial jump highlighting the relevance of such deals in protecting against early exits that GPs are forced to make with the end of the fund tenure. The return potential of such vehiclesis towards the higher end of the spectrum because the holdings are believed to be solid assets with a significant upside. This trend highlights important insights for the Indian markets:

When it comes to direct secondaries, it remains a flourishing space both in the US and India. From India’s perspective, these transactions are of particular significance because the Indian economy is much younger. As a result, the growth that some companies are seeing is exponential. With the end of each 10-year fund cycle, these companies are evolving to the next phase of their business life cycle (what started as a startup might be in its growth phase after 10 years and in its mature phase in another 10 years). This necessitates the secondary transactions between existing and new investors to suit the needs of the new phases a company finds itself in. The value added by a VC fund does not roll over to the growth stage of a company and it needs a different group of investors and partners to tackle different set of challenges to ensure continued growth.

This is a valuable strategy from the perspective of fund managers as well. Funds are set up with a defined strategy and focus on their areas of expertise. A VC fund manager’s expertise does not extend to managing a growth stage company and so it is best for them to sell their position to a better suited investor. Secondaries provide them the avenue to exit and recycle the proceeds in other startups.

“Market dislocations: where chaos meets opportunity, and the bold find their path to profit.”

Figure 3 is pointing to another very crucial aspect of secondaries – transaction volumes see a significant jump in times of market dislocations and consequent liquidity crunch. Two noteworthy instances of this, as highlighted in the chart, are:

This highlights the potential of this asset class to really solve the illiquidity problem that has bothered investors in the past. This characteristic also acts as a predictor for the success of secondaries: when the markets catch fire, investors with the right foresight can tap into this asset class to gain profits higher than other areas of the market.

Bringing it all back together, secondaries provide a very attractive investment opportunity in India – be it LP-led or GP-led or direct secondaries. Looking at how the space has developed in the US, we can gage the direction where it may go in India as the private markets evolve further. But looking at their history in the US is not the only factor helping to raise confidence in the future of secondaries in India.

TERMS OF USE

Thank you for your interest in our Website at https://unlistedintel.com/. Your use of this Website, including the content, materials and information available on or through this Website (together, the “Materials”), is governed by these Terms of Use (these “Terms”). By using this Website, you acknowledge that you have read and agree to these Terms.

NO OFFER, SOLICITATION OR ADVICE

Our site is provided for informational purposes only. It does not constitute to constitute (i) an offer, or solicitation of an offer, to

purchase or sell any security, other assets, or service, (ii) investment, legal, business, or tax advice, or an offer to provide such advice or (iii) a basis for making any investment decision.

The Materials are provided for informational purposes and have been prepared by Oister Global for informational purposes to acquaint existing and prospective underlying funds, entrepreneurs, and other company founders with Oister Global's recent and historical investment activities.

Please note that any investments or portfolio companies referenced in the Materials are illustrative and do not reflect the performance of any Oister Global fund as a whole. There is no obligation for Oister Global to update or alter any forward-looking statements, whether as a result of new information, future events, or otherwise.

PURPOSE LIMITATION AND ACCESS TO YOUR PERSONAL DATA:

We will only collect your personal data in a fair, lawful, and transparent manner. We will keep your personal data accurate and up to date. We will process your personal data in line with your legal rights. We use your name and contact details, such as email, postal address, and contact number to continue communications with you. We may also use your contact information to invite you to events we are hosting or to keep you updated with our news.

USE OF COOKIES OR SIMILAR DEVICES

We use cookies on our website. This helps us to provide you with a better experience when you browse our website and also allows us to make improvements to our site. You may be able to change the preferences on your browser or device to prevent or limit your device’s acceptance of cookies, but this may prevent you from taking advantage of some of our features.

MATERIAL

The material displayed on our site is provided “as is”, without any guarantees, conditions, or warranties as to its accuracy, completeness, or reliability. You should be aware that a significant portion of the Materials includes or consists of information that has been provided by third parties and has not been validated or verified by us. In connection with our investment activities, we often become subject to a variety of confidentiality obligations to funds, investors, portfolio companies, and other third parties. Any statements we make may be affected by those confidentiality obligations, with the result that we may be prohibited from making full disclosures.

MISCELLANEOUS

This Website is operated and controlled by Oister Global in India. We may change the content on our site at any time. If the need arises, we may suspend access to our site, or close it indefinitely. We are under no obligation to update any material on our site.

CONTACT INFORMATION

Any questions, concerns or complaints regarding these Terms should be sent to info@oisterglobal.com