Dear reader,

“The light at the end of the tunnel. Out of the woods. Every cloud has a silver lining. Keep calm and carry on.”

Turns out, we have an awful lot of expressions for making it through turbulent times.

After six months of tariff headlines, geopolitical flare-ups and macro surprises, the last couple of weeks have finally felt… peaceful. Not perfect, but peaceful. A welcome sliver of normalcy. I suspect we’re all happy to take it.

And with a little calm comes a familiar sight: the newspapers are smelling like DRHPs again.

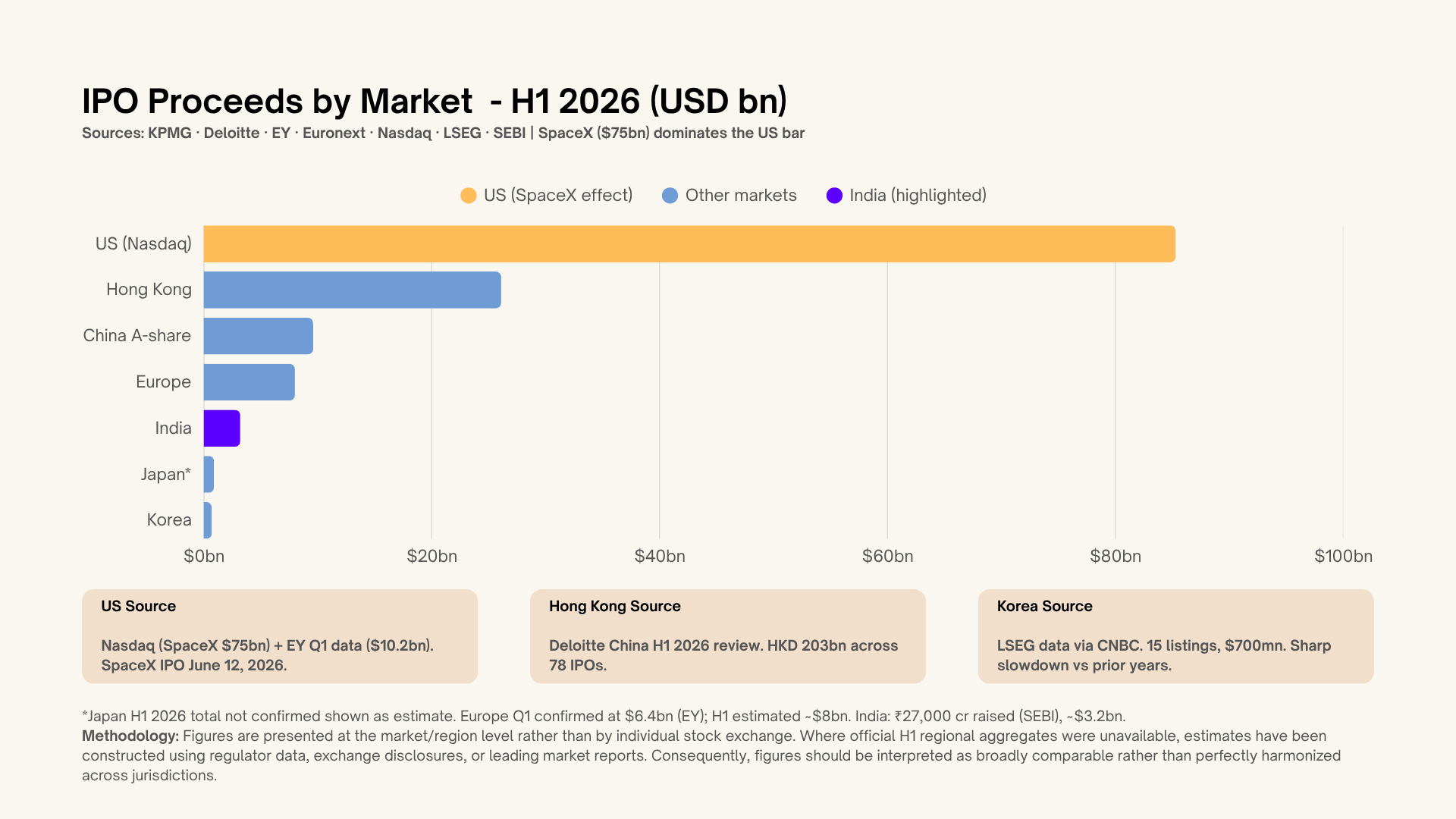

The world just witnessed its largest-ever deep-tech, space-tech listing. SpaceX has officially lifted off (pun intended), raising $75 billion at a $1.77 trillion valuation. The listing almost felt like a flare gun that finally broke the geopolitical chokehold the world has been under since March

At home, the story is similar as India prepares for some of the biggest IPOs. India’s most anticipated exchange, the NSE, finally filed its DRHP after a decade-long wait. Soon after, India’s largest telecom giant, Jio, followed suit, announcing its move from the stage of its own AGM.

Rather than asking who is going public, I wanted to explore why now? More specifically, the two distinct mindsets emerging behind today’s IPO decisions: companies that draft because they’re fundamentally ready, and companies that drift, waiting for the market window to feel just right.

But before we get into the mindset, let us set the scene.

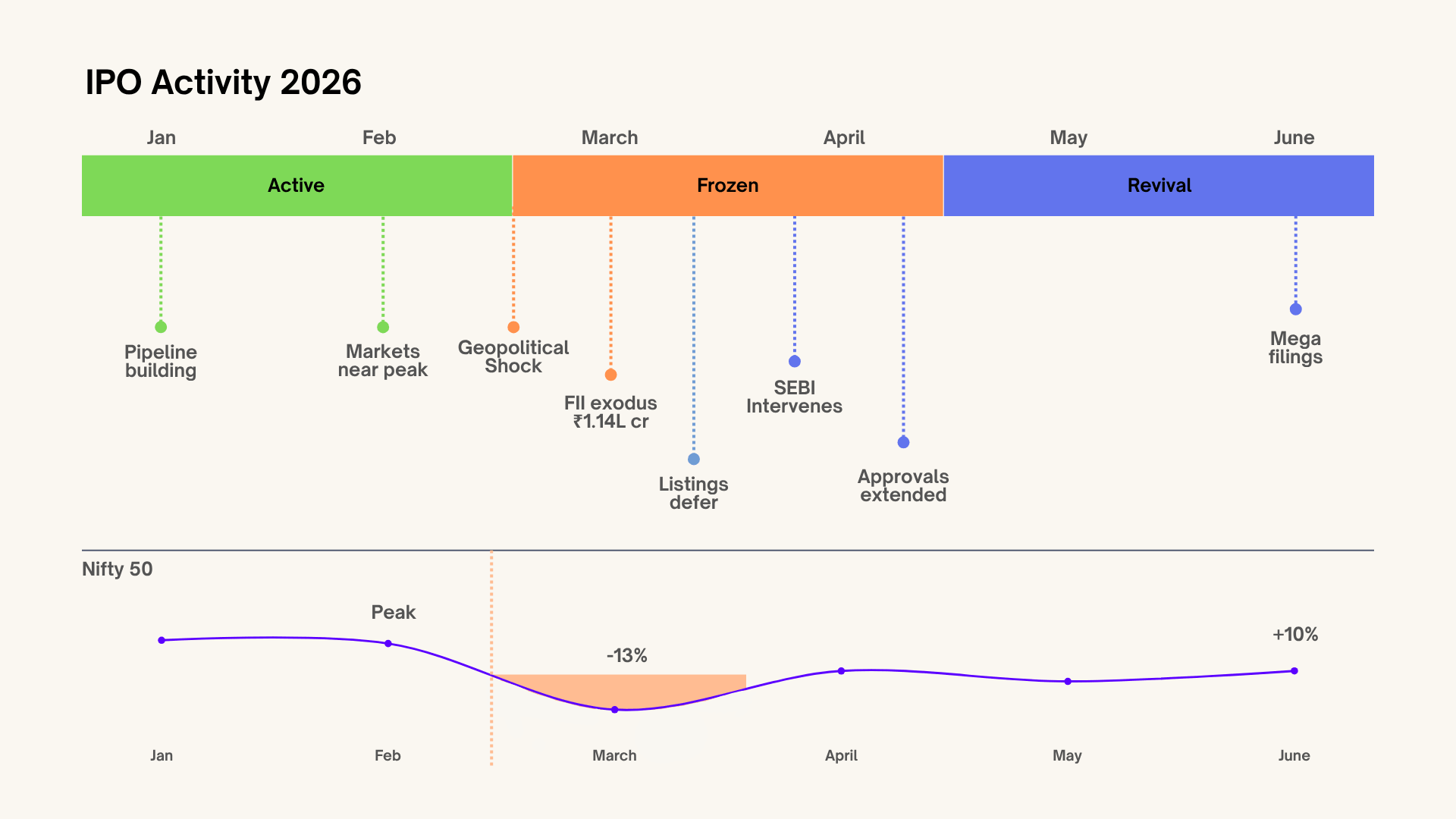

H1 2026 was, by any measure, a year of two halves, compressed into six months. January and February held promise. A healthy pipeline of quality companies was moving through SEBI, markets were near multi-month highs, and investor appetite felt firm.

Then February 28 arrived. Conflict erupted in West Asia. Crude crossed $100. In March alone, foreign investors pulled ₹1.14 lakh crore from Indian equities. a number that still staggers when you sit with it. The Nifty fell 13% from its peak. Companies with valid SEBI approvals, bankers on retainer, and roadshow decks already printed made a collective decision: not yet.

The freeze was swift. Of 22 mainboard listings in H1 2026, 14 debuted in the red. Average listing day return: 1.64%. Only one mainboard IPO launched in April. Nearly ₹2.45 lakh crore in approved IPOs sat untouched, their observation letters ticking down toward expiry.

SEBI moved in April, extending approval windows to September 30, allowing issue sizes to flex by up to 50% without refiling. It was a pragmatic intervention, and a signal that the regulator understood what the market was going through.

Across markets, H1 2026 told a version of the same story. Globally, IPO proceeds surged 208% year-on-year, but deal count fell 8%. Fewer listings. Bigger ones. Hong Kong ran its most active primary market in five years. Europe’s defence sector produced the world’s third-largest IPO of the quarter. And in the US, SpaceX did what SpaceX does, rewrote the record books and made everything else look small by comparison.

Within that backdrop, two very different things were happening.

Some companies kept moving. They filed, priced, and listed into the volatility, into the uncertainty, into a primary market that was actively delivering negative returns to new entrants. The conditions were unfavourable. They proceeded regardless.

Others paused. Deliberately and strategically. DRHPs sat approved but unfiled. Roadshows were postponed. Nearly ₹2.45 lakh crore in approved IPOs remained unlaunched through the peak of the freeze. These were not companies lacking readiness, many had regulatory approvals in hand, institutional interest mapped, and the governance infrastructure of a public company already largely in place. The decision to wait was a considered one.

Same market. Same regulatory environment. Same macroeconomic shock. Two fundamentally different responses.

What makes this bifurcation worth examining is precisely that both sides had strong arguments. This was not a case of prepared companies proceeding and unprepared ones retreating. The split ran along a deeper line, a difference in how leadership on each side fundamentally understood what a public listing is for.

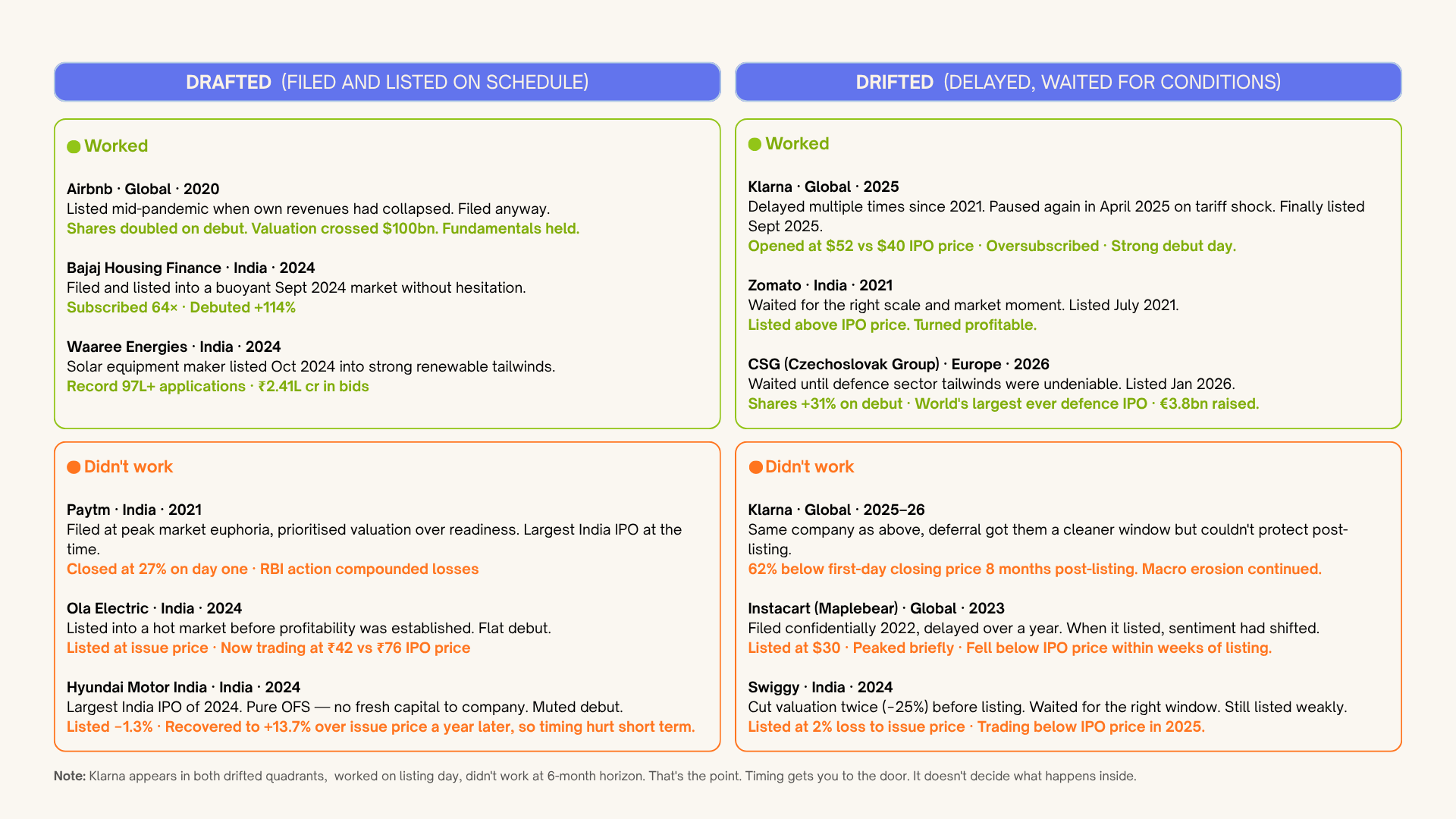

The data above resists easy conclusions. Companies that filed into difficult conditions and were rewarded. Companies that waited carefully for the right window and still underperformed post-listing. The most documented case of this paradox is Klarna, the Swedish buy-now-pay-later giant that spent years as Europe’s most closely watched private company, reaching a peak valuation of $45 billion in 2021 before the tech correction brought it sharply back to earth. It delayed its IPO repeatedly, each time citing conditions. When it finally listed in September 2025, the debut was strong, oversubscribed, shares up 30% on day one. Six months later, the stock was 62% below its first-day closing price.

Same company. Different time horizons. Different columns. Timing, it turns out, is not the variable that explains the divergence. Something more fundamental is.

There is a certain type of founder who looks at a volatile market and sees, not a reason to wait, but a reason to move.

The drafters aren’t reckless. They operate from a conviction that over any meaningful time horizon, public markets reward quality. A business with clean unit economics, honest disclosures and tight governance will find liquidity, whether in a bull market, a bear market or somewhere in between. That chasing the perfect macro window is, itself, a form of strategic distraction.

Their belief is clear, if the business is ready, the timing is right.

This is a harder position to hold than it sounds. Filing into a weak market requires a specific kind of institutional confidence. the confidence that the business does not need the market’s enthusiasm to validate its own worth. It already knows what it is. It is inviting the public in, not seeking their approval.

The historical record offers them some support. Airbnb filed and listed in December 2020, at the height of a pandemic that had devastated its own revenues. Shares doubled on debut. The business was so fundamentally sound that the market looked past the conditions and priced the conviction. Bajaj Housing Finance listed in September 2024 into a market already showing signs of fatigue. Subscribed 67 times. Debuted at a 114% premium.

In both cases, the window wasn’t perfect. The business was.

Then there is the other kind of founder. Equally capable. Equally prepared. Just guided by a different conviction.

For the drifters, the IPO isn’t the finish line. And that intuitively makes sense. IPO is the first day of life as a public company, and first impressions matter. Their calculus is simple and rooted in fiduciary responsibility: a poor listing is never just a bad day. It becomes a permanent narrative. Once a stock earns the label of a ‘broken IPO,’ that reputation leaves a stain for years afterward

Of the mainboard listings in H1 2026, the majority struggled on debut, with March listings averaging negative returns. April saw a near-complete freeze, with the pipeline effectively standing still as approved IPOs waited out the turbulence. FII outflows of ₹1.14 lakh crore in a single month. A Nifty nearly 13% off its peak. In that environment, waiting was not hesitation, it was a considered read of the room.

The trade-off is clear. Waiting delayed liquidity. Listing too early risked something far harder to recover from: a depressed stock, weaker institutional demand and a public narrative that could outlast the market cycle itself.

So they waited, but not idly. They strengthened governance, sharpened unit economics and built businesses that could justify their valuations on fundamentals alone, not favourable market conditions.

Because markets recover. Broken IPO narratives rarely do. And a company that arrives at the public eye on its own terms, not the market’s, tends to stay there longer.

The question of who wins between the drafters and the drifters is, in itself, a category error. Both camps are responding to the same structural reality, the transition from a market of noise to a market of quality.

The distinction lies in the founder’s primary objective. Does the leadership view the public market as a temporary window to exploit at a peak valuation? Or as the permanent, final home for a mature business?

One is a transaction; the other is a conviction.

The founder timing the market is optimizing for the listing. The founder building for the market is optimizing for the decade that follows it. We aren’t making a moral judgment,the market requires both the aggressive builders and the disciplined stewards. However, for an investor looking at a business through a full cycle, the reasoning behind the filing date is the most critical signal available. The filing date tells you when. The reasoning tells you who.

The era of the speculative, hyper-inflated rush has ended because the market enforced it. Bad listings are remembered. Broken IPOs scar a stock for years. A structural quality filter has taken hold, and it is arguably the most underappreciated shift in India’s private market narrative.

This shift in founder mindset is fundamentally changing how companies present themselves to the public. As a result, the document itself has evolved.

The modern DRHP is no longer a growth story being sold. It is a maturity test being submitted. Governance, cash flow reality, unit economics, no longer buried in risk factors. They are the thesis. Both drafters and drifters will face this filter equally. Timing doesn’t bypass it. Only substance does.

This shift is visible beyond the listing halls too. The VC and PE ecosystem has matured, and with it, the approach to exits has evolved. Capital is being deployed with longer conviction horizons. Businesses are increasingly built with public-market readiness baked into their core, not bolted on at listing. The IPO is no longer a destination to be rushed toward. It is an outcome to be earned.

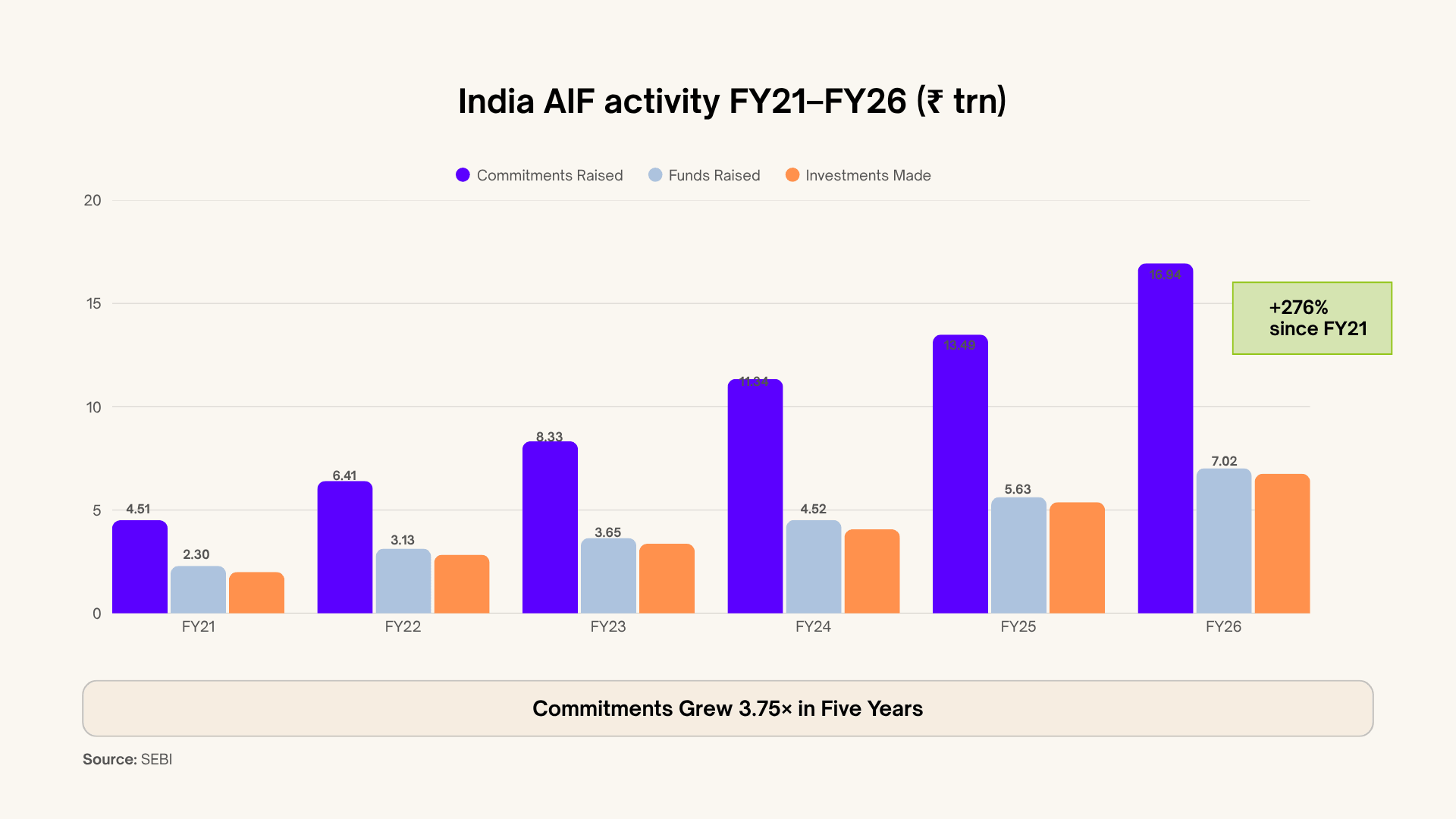

The numbers reflect this. AIF commitments in India have grown from ₹4.51 trillion in FY21 to ₹16.94 trillion in FY26, a 3.75x expansion in five years, compounding at over 30% annually. That trajectory doesn’t emerge from an ecosystem chasing quick exits. It emerges from one that has collectively decided to build with depth, discipline, and a longer view of what value creation actually looks like.

It is a transition from a market of noise to a market of quality. And that transition, once made, tends to be permanent.

At Oister, we have skin in this conversation, even if we aren’t the ones ringing the opening bell.

We operate in the layer before the DRHP. As a private markets asset manager, we back companies in India’s secondary and private markets, some already on the public stage, others yet to see a ticker. For all of them, the eventual moment of truth is the same: the choice to draft or drift. The perpetual tension between whether the business is ready, whether the market is ready, and the realization that those two things rarely align on schedule.

What we’ve learned, consistently, is this: the IPO is not the destination. It is an audit. The moment the public market holds up a mirror to everything that was built in the years before the prospectus was filed. The companies worth backing are the ones that would pass that audit on any given day, not just when conditions are kind.

We’ve always believed that the best companies don’t time the market. They outlast it.

Thank you, and see you next month.

Jai Hind

TL;DR: The H1 2026 IPO market split into “Drafters” (those listing despite market volatility, betting on business fundamentals) and “Drifters” (those waiting for better timing, viewing it as a fiduciary duty to protect their stock’s reputation). Ultimately, the distinction is cosmetic; the market has shifted from rewarding growth stories to demanding maturity. Whether a founder lists now or later, only business substance, not timing determines success.

TERMS OF USE

Thank you for your interest in our Website at https://unlistedintel.com/. Your use of this Website, including the content, materials and information available on or through this Website (together, the “Materials”), is governed by these Terms of Use (these “Terms”). By using this Website, you acknowledge that you have read and agree to these Terms.

NO OFFER, SOLICITATION OR ADVICE

Our site is provided for informational purposes only. It does not constitute to constitute (i) an offer, or solicitation of an offer, to

purchase or sell any security, other assets, or service, (ii) investment, legal, business, or tax advice, or an offer to provide such advice or (iii) a basis for making any investment decision.

The Materials are provided for informational purposes and have been prepared by Oister Global for informational purposes to acquaint existing and prospective underlying funds, entrepreneurs, and other company founders with Oister Global's recent and historical investment activities.

Please note that any investments or portfolio companies referenced in the Materials are illustrative and do not reflect the performance of any Oister Global fund as a whole. There is no obligation for Oister Global to update or alter any forward-looking statements, whether as a result of new information, future events, or otherwise.

PURPOSE LIMITATION AND ACCESS TO YOUR PERSONAL DATA:

We will only collect your personal data in a fair, lawful, and transparent manner. We will keep your personal data accurate and up to date. We will process your personal data in line with your legal rights. We use your name and contact details, such as email, postal address, and contact number to continue communications with you. We may also use your contact information to invite you to events we are hosting or to keep you updated with our news.

USE OF COOKIES OR SIMILAR DEVICES

We use cookies on our website. This helps us to provide you with a better experience when you browse our website and also allows us to make improvements to our site. You may be able to change the preferences on your browser or device to prevent or limit your device’s acceptance of cookies, but this may prevent you from taking advantage of some of our features.

MATERIAL

The material displayed on our site is provided “as is”, without any guarantees, conditions, or warranties as to its accuracy, completeness, or reliability. You should be aware that a significant portion of the Materials includes or consists of information that has been provided by third parties and has not been validated or verified by us. In connection with our investment activities, we often become subject to a variety of confidentiality obligations to funds, investors, portfolio companies, and other third parties. Any statements we make may be affected by those confidentiality obligations, with the result that we may be prohibited from making full disclosures.

MISCELLANEOUS

This Website is operated and controlled by Oister Global in India. We may change the content on our site at any time. If the need arises, we may suspend access to our site, or close it indefinitely. We are under no obligation to update any material on our site.

CONTACT INFORMATION

Any questions, concerns or complaints regarding these Terms should be sent to info@oisterglobal.com