[TL;DR]

Under CEO Narv Narvekar, Harvard Management Company dismantled its in-house trading desks and pivoted to a pure outsourced model — systematically cutting real estate and hard assets to fund an aggressive move into private equity and uncorrelated alternatives. But the October 2025 CEO letter reveals a nuance most observers miss: HMC is now deliberately increasing portfolio risk through greater equity exposure, having determined that the fund had been too conservatively positioned relative to its actual ability to absorb volatility. The endowment is not simply chasing returns — it is recalibrating risk to match Harvard’s unique institutional capacity to hold through turbulence.

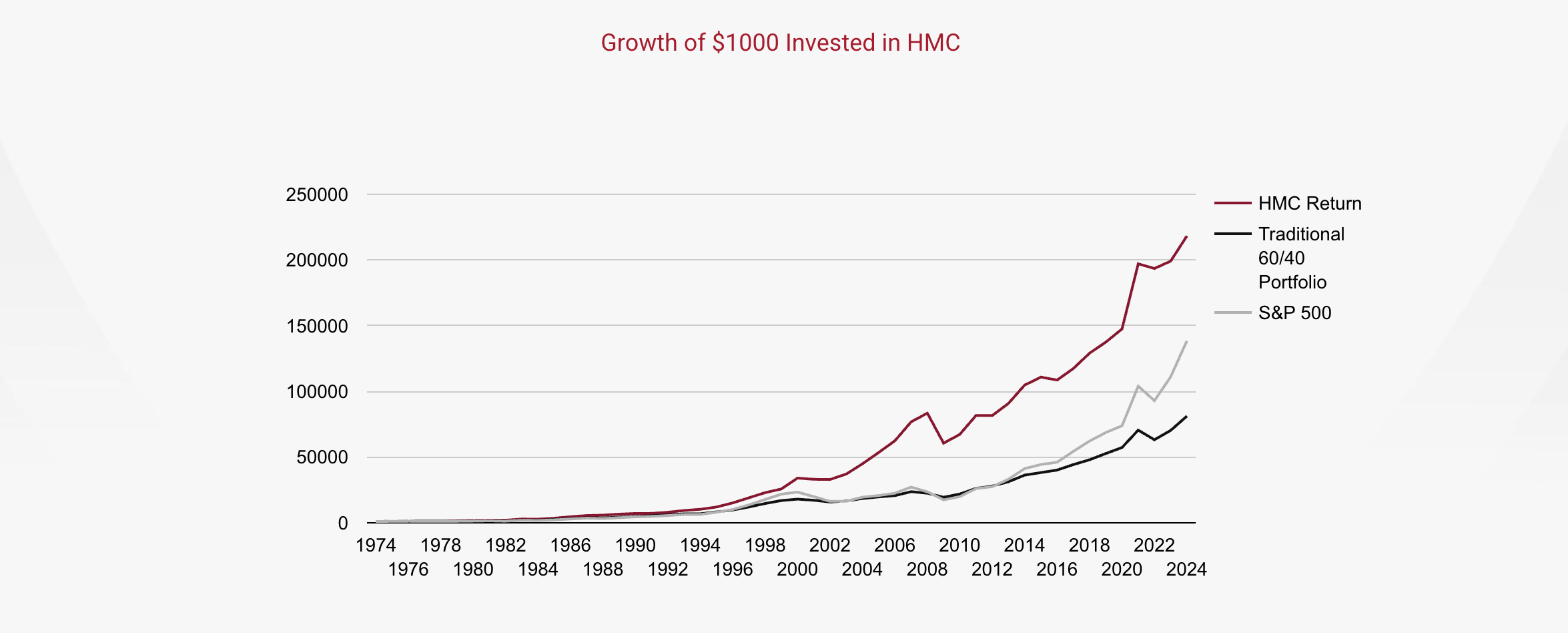

The most compelling argument for Harvard’s model isn’t a single year’s returns — it’s five decades of compounding. Since HMC’s founding in 1974, a $1,000 investment in the endowment has grown to approximately $220,000. The S&P 500 over the same period delivered roughly $140,000. A traditional 60/40 portfolio — the institutional default for most allocators — produced around $75,000. That’s not a marginal difference. HMC’s model has generated nearly 3x the wealth of conventional balanced investing over a full market cycle spanning oil shocks, the dot-com collapse, the 2008 financial crisis, COVID, and multiple rate regimes. The gap widens precisely because the endowment’s private market positions compound quietly during public market drawdowns rather than marking down with the crowd. In total, HMC has distributed more than $46 billion to the University — not as a byproduct of good investing, but as its explicit mandate. Performance here is not optional; endowment distributions now fund more than one-third of Harvard’s entire annual operating budget.

Source: Harvard Management Company

The standard critique of private-heavy portfolios is the capital trap — money locked away for a decade with no exit. Harvard’s answer is structural: because annual distributions are calibrated at roughly 5% of AUM (benchmarked against ~3% inflation + ~5% spending), the fund never needs to be liquid in aggregate. But the CEO letter adds a critical operational detail: HMC actively uses the secondary market as a portfolio management tool — not as a sign of distress, but as a disciplined mechanism to reallocate away from real estate at moments of strength and continuously refine its private equity composition. Liquidity is engineered, not hoped for.

Source: Harvard Management Company

TERMS OF USE

Thank you for your interest in our Website at https://unlistedintel.com/. Your use of this Website, including the content, materials and information available on or through this Website (together, the “Materials”), is governed by these Terms of Use (these “Terms”). By using this Website, you acknowledge that you have read and agree to these Terms.

NO OFFER, SOLICITATION OR ADVICE

Our site is provided for informational purposes only. It does not constitute to constitute (i) an offer, or solicitation of an offer, to

purchase or sell any security, other assets, or service, (ii) investment, legal, business, or tax advice, or an offer to provide such advice or (iii) a basis for making any investment decision.

The Materials are provided for informational purposes and have been prepared by Oister Global for informational purposes to acquaint existing and prospective underlying funds, entrepreneurs, and other company founders with Oister Global's recent and historical investment activities.

Please note that any investments or portfolio companies referenced in the Materials are illustrative and do not reflect the performance of any Oister Global fund as a whole. There is no obligation for Oister Global to update or alter any forward-looking statements, whether as a result of new information, future events, or otherwise.

PURPOSE LIMITATION AND ACCESS TO YOUR PERSONAL DATA:

We will only collect your personal data in a fair, lawful, and transparent manner. We will keep your personal data accurate and up to date. We will process your personal data in line with your legal rights. We use your name and contact details, such as email, postal address, and contact number to continue communications with you. We may also use your contact information to invite you to events we are hosting or to keep you updated with our news.

USE OF COOKIES OR SIMILAR DEVICES

We use cookies on our website. This helps us to provide you with a better experience when you browse our website and also allows us to make improvements to our site. You may be able to change the preferences on your browser or device to prevent or limit your device’s acceptance of cookies, but this may prevent you from taking advantage of some of our features.

MATERIAL

The material displayed on our site is provided “as is”, without any guarantees, conditions, or warranties as to its accuracy, completeness, or reliability. You should be aware that a significant portion of the Materials includes or consists of information that has been provided by third parties and has not been validated or verified by us. In connection with our investment activities, we often become subject to a variety of confidentiality obligations to funds, investors, portfolio companies, and other third parties. Any statements we make may be affected by those confidentiality obligations, with the result that we may be prohibited from making full disclosures.

MISCELLANEOUS

This Website is operated and controlled by Oister Global in India. We may change the content on our site at any time. If the need arises, we may suspend access to our site, or close it indefinitely. We are under no obligation to update any material on our site.

CONTACT INFORMATION

Any questions, concerns or complaints regarding these Terms should be sent to info@oisterglobal.com