[TL;DR]

A Gen Z shopper opens Blinkit in Delhi looking for a specific face serum from a legacy FMCG giant. It’s out of stock. Seven seconds later, she taps buy on an alternative from Foxtale or Minimalist. Twenty years of prime-time television advertising, lost to a single hyper-local inventory miss.

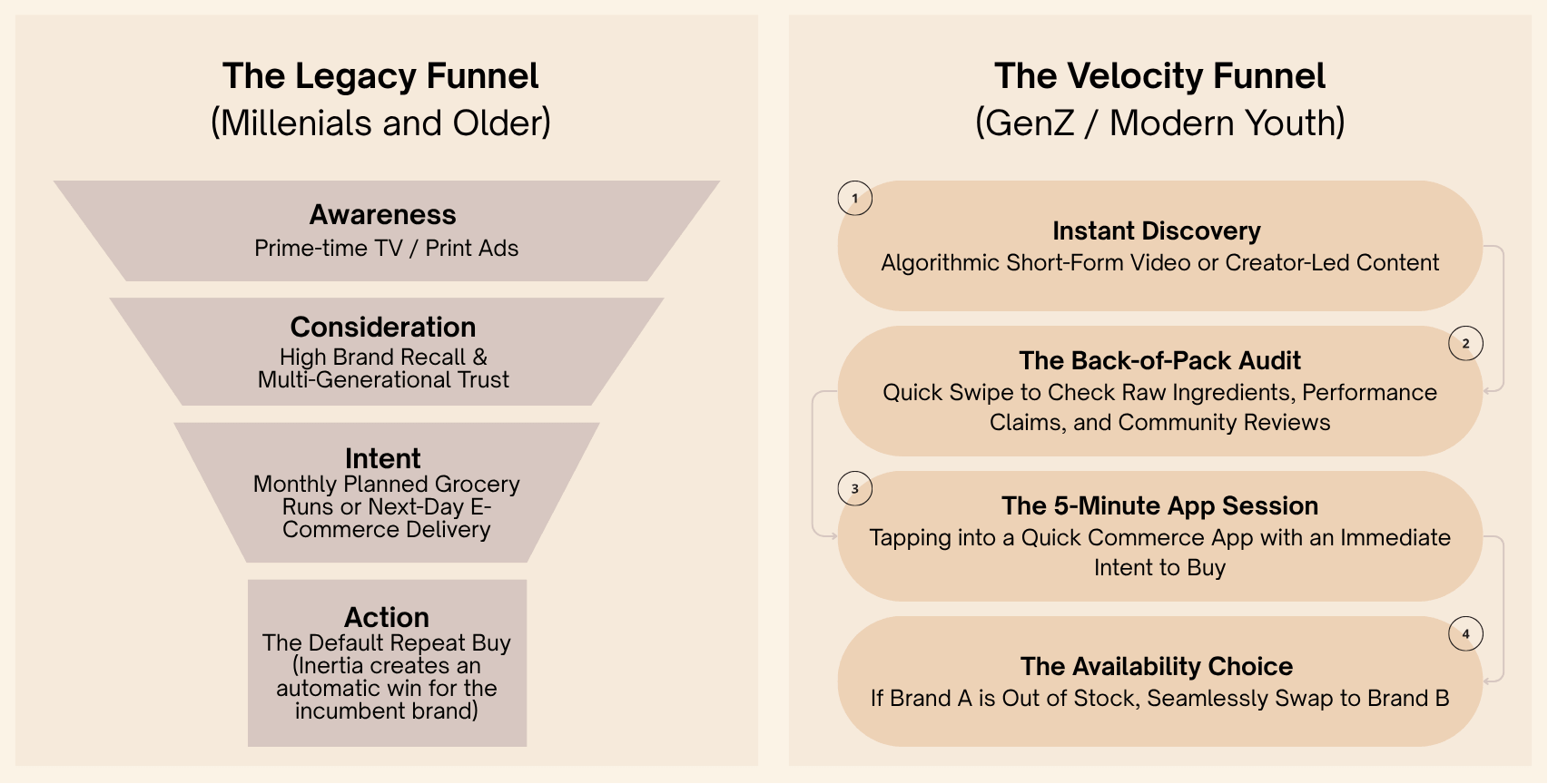

That is the new operational reality of the Indian consumer market. For decades, consumer-facing businesses operated under a comfortable premise: earn a household’s trust once, keep it for generations. Brand equity was an impenetrable moat built on massive media buy and physical distribution networks. That playbook has completely broken down. India’s 377 million Gen Z consumers now directly influence 43% of national household consumption, driving $860 billion in economic power — $200 billion of it from their own independent earnings as the oldest members enter the workforce. But to conclude that loyalty is dead is to miss the point entirely. Loyalty hasn’t disappeared. It has fundamentally shifted from marketing-driven loyalty to operational loyalty. The battle for the modern Indian consumer is no longer won in marketing departments. It is won in the unit economics of the supply chain.

The “default repeat buy” — the automatic, inertia-driven repurchase that sustained legacy FMCG margins for decades — has been eliminated by three simultaneous structural forces.

The first is instant gratification at infrastructure scale. Quick commerce has re-engineered consumer psychology by training urban shoppers to expect 10-minute delivery. India’s dark store network has expanded to over 7,000 micro-fulfillment centers to meet this expectation, with sessions lasting under 5 minutes and visit-to-order conversion running 8x higher than traditional e-retail. When intent spikes and a preferred brand is out of stock, consumers don’t wait — they swap. Convenience has permanently replaced heritage as the primary loyalty driver at the moment of purchase.

The second is radical transparency. Young consumers have universally decoupled celebrity hype from product performance. Insurgent players like Minimalist have scaled rapidly by printing active ingredient percentages on the front of their bottles, transforming transparency from a compliance requirement into a core product feature. Brand trust is now audited at the back of the pack — raw ingredients, sourcing ethics, functional formulation — not bought through prime-time commercials. Four out of five Gen Z consumers see protein as essential and actively track nutritional credentials; two out of five millennials always read food labels for sugar content. The consumer who reads labels doesn’t respond to taglines.

The third is dupe culture at mass scale. The explosion of agile D2C brands has democratised premium efficacy at mass-market prices. Consumer sentiment data shows 82% of young consumers actively plan to purchase prestige-quality alternatives without the heritage price markup. The quality gap that once protected global incumbents has effectively closed.

Together, these three forces have replaced the loyalty moat with a real-time availability battle fought inside a 5-minute app session.

The most important signal for brand operators and capital allocators is where quick commerce volume is concentrating. According to Redseer’s March 2026 report, quick commerce’s share in Food FMCG is projected to grow 4.5x — from 4% today to 15–20% by 2030 — at a 45–50% CAGR, growing roughly 9x faster than all other retail channels combined.

| Category | YoY Growth via Quick Commerce | 2030 Outlook |

|---|---|---|

| Food FMCG (QC share) | 4% → 15–20% by 2030 | 45–50% CAGR |

| Frozen RTC | +88% (CY24–25) | ~$375M established category |

| Chocolates (online QC share) | +110% YoY | QC drove ~50% of incremental growth |

| NARTD Beverages | QC growing >100% | Market heading to $40B by 2030 |

| Packaged Coconut Water | >20% of packaged sales via QC | 60–80 brands competing |

The brand that wins in this environment is no longer the one with the largest historical marketing spend. It is the brand that maintains a flawless, real-time digital supply chain deeply integrated with localised dark store networks — and that shows up first on the app screen the moment intent spikes.

Source : How India Shops Online 2026

Because top-line GMV growth can be artificially inflated through expensive, non-repeating performance marketing, institutional investors have fundamentally rewritten their valuation frameworks. The core boardroom question has shifted from “How many users did you add?” to “How many stayed?”

Three operational metrics now dominate consumer brand due diligence:

Net Cohort Retention — Does a specific customer group’s spending grow or remain stable over 12 months, rather than simply transacting once? Repeat GMV from an existing cohort is valued exponentially above first-purchase acquisition numbers, because it proves the supply chain — not the campaign — is doing the work.

Organic Brand Search Volume — What percentage of digital traffic arrives via unpaid, direct brand search versus expensive keyword targeting? In quick commerce, a consumer typing a brand name directly into Blinkit or Zepto is the clearest possible signal of genuine preference over algorithmic placement.

Dark Store Fill Rate — Is the brand maintaining 98%+ availability at the hyper-local level? A single stock-out in a high-intent moment is no longer a missed sale. It is an actively converted customer for an insurgent competitor whose only advantage was being in stock.

TERMS OF USE

Thank you for your interest in our Website at https://unlistedintel.com/. Your use of this Website, including the content, materials and information available on or through this Website (together, the “Materials”), is governed by these Terms of Use (these “Terms”). By using this Website, you acknowledge that you have read and agree to these Terms.

NO OFFER, SOLICITATION OR ADVICE

Our site is provided for informational purposes only. It does not constitute to constitute (i) an offer, or solicitation of an offer, to

purchase or sell any security, other assets, or service, (ii) investment, legal, business, or tax advice, or an offer to provide such advice or (iii) a basis for making any investment decision.

The Materials are provided for informational purposes and have been prepared by Oister Global for informational purposes to acquaint existing and prospective underlying funds, entrepreneurs, and other company founders with Oister Global's recent and historical investment activities.

Please note that any investments or portfolio companies referenced in the Materials are illustrative and do not reflect the performance of any Oister Global fund as a whole. There is no obligation for Oister Global to update or alter any forward-looking statements, whether as a result of new information, future events, or otherwise.

PURPOSE LIMITATION AND ACCESS TO YOUR PERSONAL DATA:

We will only collect your personal data in a fair, lawful, and transparent manner. We will keep your personal data accurate and up to date. We will process your personal data in line with your legal rights. We use your name and contact details, such as email, postal address, and contact number to continue communications with you. We may also use your contact information to invite you to events we are hosting or to keep you updated with our news.

USE OF COOKIES OR SIMILAR DEVICES

We use cookies on our website. This helps us to provide you with a better experience when you browse our website and also allows us to make improvements to our site. You may be able to change the preferences on your browser or device to prevent or limit your device’s acceptance of cookies, but this may prevent you from taking advantage of some of our features.

MATERIAL

The material displayed on our site is provided “as is”, without any guarantees, conditions, or warranties as to its accuracy, completeness, or reliability. You should be aware that a significant portion of the Materials includes or consists of information that has been provided by third parties and has not been validated or verified by us. In connection with our investment activities, we often become subject to a variety of confidentiality obligations to funds, investors, portfolio companies, and other third parties. Any statements we make may be affected by those confidentiality obligations, with the result that we may be prohibited from making full disclosures.

MISCELLANEOUS

This Website is operated and controlled by Oister Global in India. We may change the content on our site at any time. If the need arises, we may suspend access to our site, or close it indefinitely. We are under no obligation to update any material on our site.

CONTACT INFORMATION

Any questions, concerns or complaints regarding these Terms should be sent to info@oisterglobal.com