TLDR

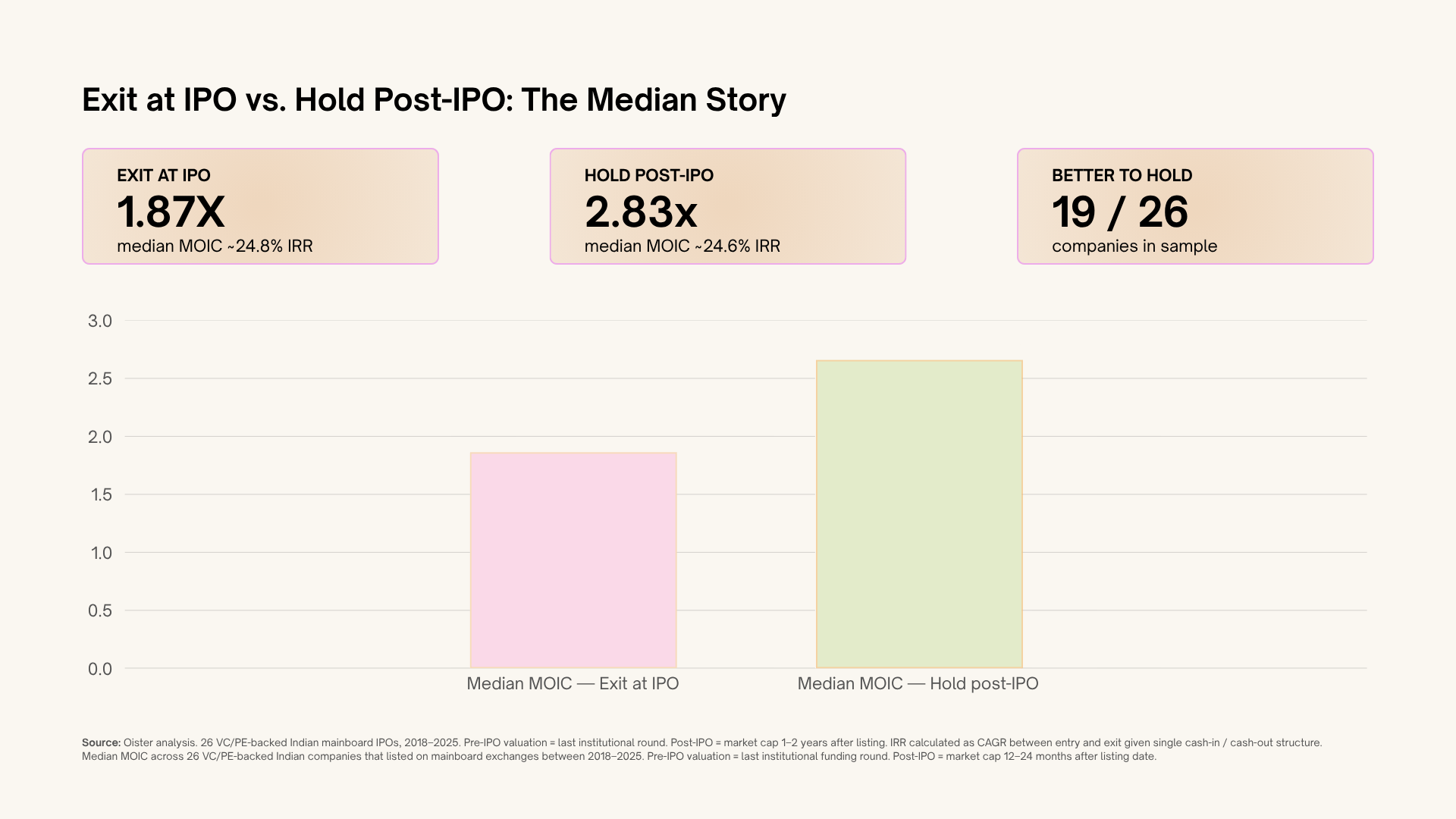

We backtested 26 VC/PE-backed Indian companies across their full journey — pre-IPO round, listing, and 1-2 years after. The median return for investors who held post-IPO was 2.83x at a 24.6% IRR — nearly double public markets. But the returns are concentrated and dispersion is violent, which means diversification isn’t optional. And most investors leave returns on the table not because they pick wrong, but because their fund structure forces them out too early. Secondaries fix both problems.

Dear Reader,

This newsletter is about backtesting.

If you trade public equities or run a quant fund (here’s wishing), backtesting is your bread and butter. You take a strategy, run it against decades of clean, timestamped historical data, and ask a simple question:

“If I had followed this rule in the past, would I have made money?”

In public markets, you can test a strategy over a weekend. In private markets, tracking historical data is notoriously difficult.

But at Oister, we are obsessed with borrowing discipline from the public markets. We wanted to see if the core thesis driving our late-stage investment strategy actually holds water.

We already do some of this. As you may have seen, our benchmarking work with CRISIL tracking private market Category II AIFs over the last decade shows that private funds have materially outperformed public markets. Across the last seven benchmarking cycles, equity AIFs delivered an average alpha of ~8.7% over the BSE Sensex TRI.

But we wanted to go further. At Oister, we do secondaries. We spend a lot of time looking at late-stage companies, the ones that are 18 to 36 months away from an IPO. And the core belief that drives a lot of what we do is this: if you enter these companies in that window, and hold them for at least a year post-listing, you capture superior, asymmetric returns.

So we took a shot at it.

We tracked 26 VC/PE backed companies that launched mainboard IPOs on the BSE or NSE and have at least a year of trading history. There were no sector or return filters. You will recognize pretty much every name: Zomato, Nykaa, Paytm, Swiggy, PolicyBazaar, and Mamaearth.

For each one, we mapped three specific milestones:

One honest caveat before we dive into the data: Every company in this dataset successfully made it to the public markets. The dozens of companies that stalled, withdrew, or failed to list aren’t here. Thiis is the story of 26 startups that IPOed in the last 3-4 years

Here is what the data revealed and why it surprised us.

The high-level data completely validates the strategy.

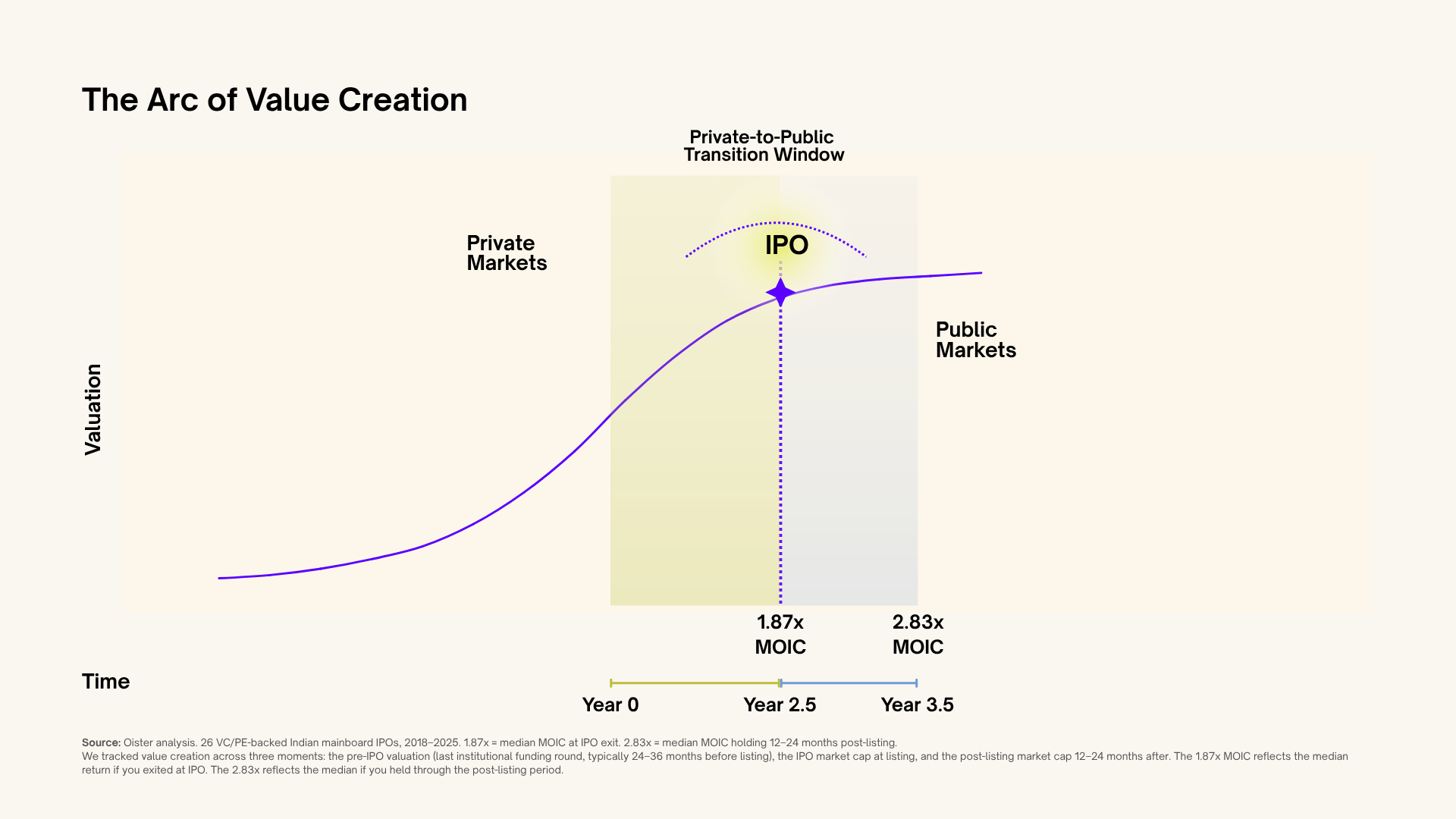

More importantly, the data completely dismantles a favorite playbook of impatient investors: buying pre-IPO, riding the listing pop, and flipping on Day 1.

If you flipped on day one, your median return dropped to 1.87x. By failing to hold, you left an entire turn of capital on the table. And here’s the nuance worth sitting with: the IRR is nearly identical, 24.8% versus 24.6%. So if you exited at IPO, you weren’t wrong on rate of return. You were just wrong on absolute wealth created. Same annual engine. The hold just kept it running longer.

In fact, 19 out of 26 companies explicitly rewarded patience.

For the vast majority, the IPO listing was barely the halfway mark where earnings maturity and market re-rating finally kicked in. And not the finish line.

Hiding behind that beautiful 2.83x median is an uncomfortable truth: extreme return dispersion. Late-stage Indian tech investing is characterized by a few spectacular breakout winners, a handful of punishing casualties, and a very quiet middle.

The key learning for us has been that individual company selection at the pre-IPO stage is inherently difficult, with outcomes often driven by factors that are hard to underwrite consistently in advance. The biggest, most institutionally backed “consensus bets” frequently underperformed, while unassuming, quieter businesses blindsided the market on the upside.

If individual winners are impossible to forecast with absolute certainty, how do you capture that highly lucrative 2.83x median?

The golden rule of private markets applies here: Concentration is the enemy. Diversification is the alpha. The investors who win don’t try to guess the single winning horse; they own enough of the basket to ensure that when an outlier hits, they hold the ticket.

Even if you get the diversification right, investors run into a structural problem the data can’t show you: forced early exits.

The data can’t show you the fund that matured in year four and was forced to sell Nykaa at ₹60 to return capital to LPs, right before the stock took off. Most investors don’t exit early because they want to; they exit because their fund structures dictate it.

When fixed fund timelines end or LPs demand distributions, perfectly good investments get crystallized at a 1.87x listing return, leaving the 2.83x post-listing compounding on the table.

This leaves late-stage investors facing two distinct roadblocks:

This is where we feel that the secondary market steps in. (Full disclosure: This is what we do at Oister, so feel free to weigh our bias accordingly).

A secondary transaction acts as a relief valve. It allows an early investor who needs liquidity to exit cleanly, while a secondary buyer enters at a price that reflects current, grounded realities rather than historical hype.

Because secondary buyers enter later in the cycle, they operate on a refreshed, cleaner timeline. They aren’t constrained by a legacy fund structure raised years prior, meaning they have the structural patience required to hold the position for the full 1 to 2 years post-listing that the data rewards.

India’s secondary landscape is growing exceptionally strong, scaling from a peripheral option into a mature, institutional liquidity channel, with average deal sizes surging 3.7x since FY20 to reach ₹8.39 billion. The acceleration is now so rapid that the H1 FY26 deal value (~₹361 billion) has already nearly matched the entirety of FY25 (~₹377 billion). Source

This volume is paving the way for institutional vehicle designs that explicitly build diversification into the strategy from day one, something UHNIs, HNIs, and family offices are actively prioritizing.

At Oister, we are already managing our third secondary fund in just two years, with over ₹1,000 crores deployed. We are seeing a fast-maturing market where domestic capital can finally access late-stage compounding systematically.

The laws of market gravity remain undefeated. If you want to capture true value in late-stage tech, two non-negotiable rules apply: Diversify your exposure, and have the patience to hold.

Secondaries are fast becoming the natural entry point to execute this playbook, offering a way to acquire a diversified portfolio with the structural patience required to let the full arc of compounding do its work.

The backtest simply proved what we already believed.

Thank you, and see you next month.

Jai Hind

TERMS OF USE

Thank you for your interest in our Website at https://unlistedintel.com/. Your use of this Website, including the content, materials and information available on or through this Website (together, the “Materials”), is governed by these Terms of Use (these “Terms”). By using this Website, you acknowledge that you have read and agree to these Terms.

NO OFFER, SOLICITATION OR ADVICE

Our site is provided for informational purposes only. It does not constitute to constitute (i) an offer, or solicitation of an offer, to

purchase or sell any security, other assets, or service, (ii) investment, legal, business, or tax advice, or an offer to provide such advice or (iii) a basis for making any investment decision.

The Materials are provided for informational purposes and have been prepared by Oister Global for informational purposes to acquaint existing and prospective underlying funds, entrepreneurs, and other company founders with Oister Global's recent and historical investment activities.

Please note that any investments or portfolio companies referenced in the Materials are illustrative and do not reflect the performance of any Oister Global fund as a whole. There is no obligation for Oister Global to update or alter any forward-looking statements, whether as a result of new information, future events, or otherwise.

PURPOSE LIMITATION AND ACCESS TO YOUR PERSONAL DATA:

We will only collect your personal data in a fair, lawful, and transparent manner. We will keep your personal data accurate and up to date. We will process your personal data in line with your legal rights. We use your name and contact details, such as email, postal address, and contact number to continue communications with you. We may also use your contact information to invite you to events we are hosting or to keep you updated with our news.

USE OF COOKIES OR SIMILAR DEVICES

We use cookies on our website. This helps us to provide you with a better experience when you browse our website and also allows us to make improvements to our site. You may be able to change the preferences on your browser or device to prevent or limit your device’s acceptance of cookies, but this may prevent you from taking advantage of some of our features.

MATERIAL

The material displayed on our site is provided “as is”, without any guarantees, conditions, or warranties as to its accuracy, completeness, or reliability. You should be aware that a significant portion of the Materials includes or consists of information that has been provided by third parties and has not been validated or verified by us. In connection with our investment activities, we often become subject to a variety of confidentiality obligations to funds, investors, portfolio companies, and other third parties. Any statements we make may be affected by those confidentiality obligations, with the result that we may be prohibited from making full disclosures.

MISCELLANEOUS

This Website is operated and controlled by Oister Global in India. We may change the content on our site at any time. If the need arises, we may suspend access to our site, or close it indefinitely. We are under no obligation to update any material on our site.

CONTACT INFORMATION

Any questions, concerns or complaints regarding these Terms should be sent to info@oisterglobal.com