Dear Reader,

Greetings from the fag-end of April.

If 2026 had a mascot, it would be a shrug. By now, we’ve all become professional athletes in the sport of ‘Dealing with Volatility.’ Tariffs? Wars? Market swings? 40-plus degrees in April? Just another Tuesday. None of it feels normal, and yet, none of it fully stops us either.

The odd part isn’t that the world is chaotic; we’ve made our peace with that. The odd part is how quickly we’ve learned to absorb the shock, adjust the sails, and move through it as if it were practiced. I don’t mean to imply that we are becoming indifferent; it’s more that we’ve developed a committed, long-term relationship with uncertainty.

And maybe that is a good thing?

Now, before I scare you off, I don’t mean “good” in the “yay, tough times build character” way. I believe I did enough of that in the last newsletter. I mean “good” in a more specific sense. Perhaps this constant volatility is doing something to the Indian private market ecosystem that stable years simply cannot.

Here’s the theory.

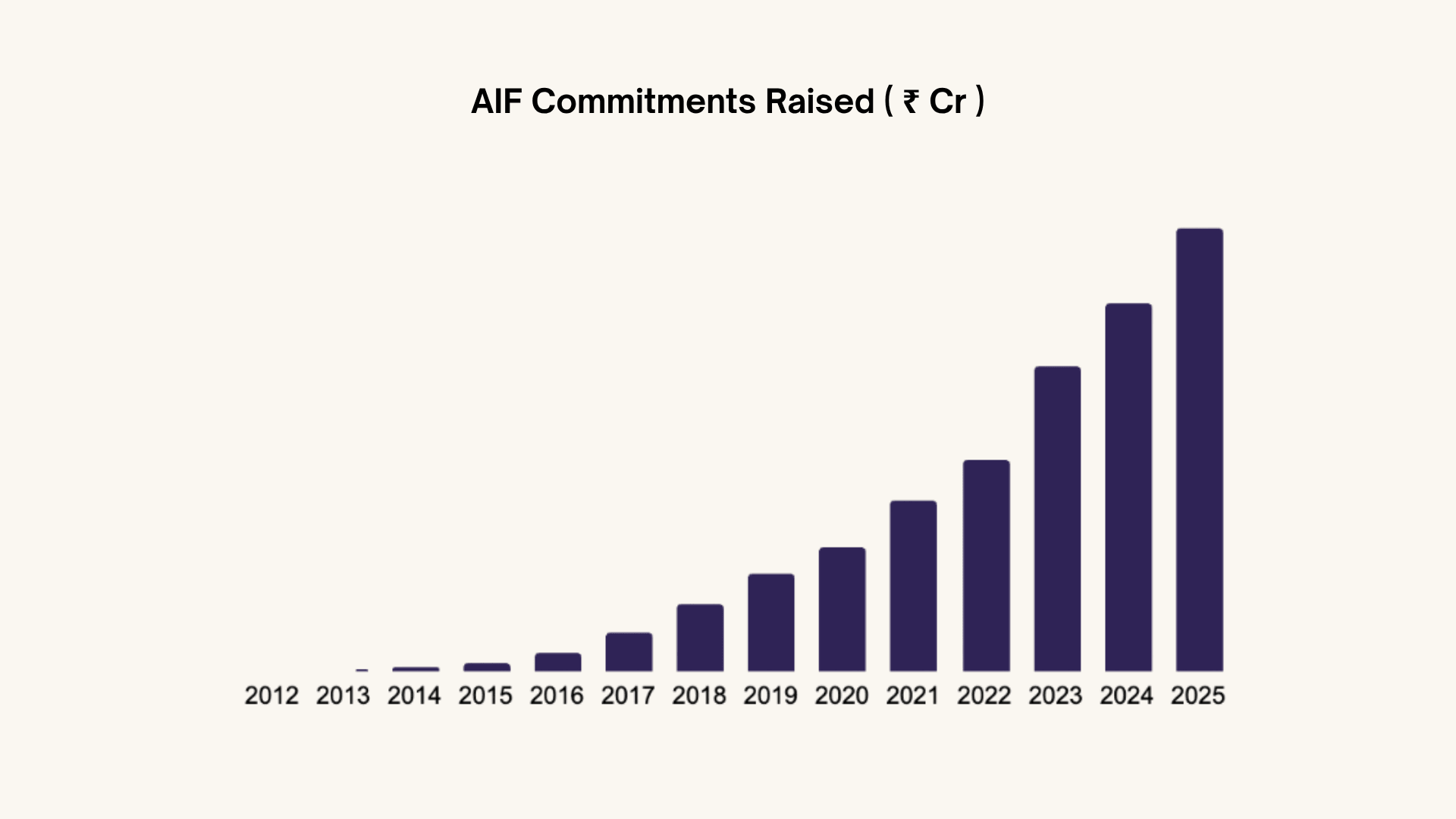

The Indian AIF ecosystem is currently 14 years old, officially settling into its teenage era. Back in March 2013, the entire organized private capital (AIFs) ecosystem of the world’s tenth-largest economy (by nominal GDP) was had recorded just ₹1,437 crore in commitments, roughly $265 million at the then-prevailing exchange rate. As of December 31, 2025, SEBI data places total AIF commitments at ₹15.74 lakh crore, or roughly $175 billion using the exchange rate around that reporting date.

Source: Statista

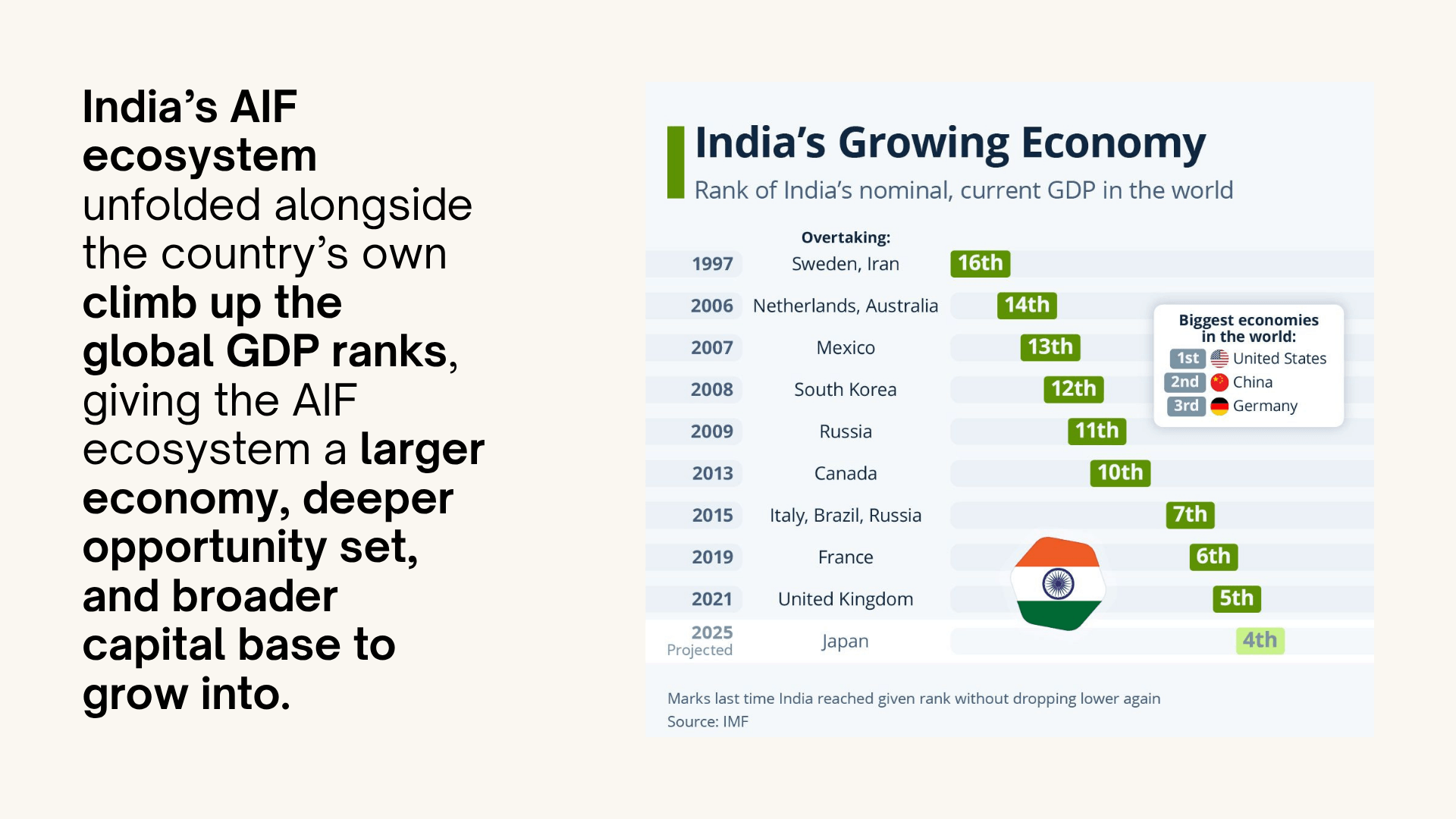

(Caption for the chart: India’s AIF ecosystem unfolded alongside the country’s own climb up the global GDP ranks, giving the AIF ecosystem a larger economy, deeper opportunity set, and broader capital base to grow into.)

While it is easy to view this as a growth story, it is more useful to view it as a timeline of structural maturity.

Source: SEBI

The timeline starts in 2012, when AIF regulations came into force. Until then, capital existed, but the system did not. Foreign private equity firms routed capital through Mauritius and Cayman Islands structures. Domestic pools of capital had no proper vehicle. Venture capital operated under a 1996 framework that had significant limitations. The market had activity but it did not have architecture.

The AIF structure created that architecture. And for the next decade, that architecture largely grew under supportive conditions.

The Nurturing Years: 2012 to 2020

The 2010s, in hindsight, were a very specific kind of environment. It was almost by design, a good one.

Global interest rates in developed markets sat near zero for most of the decade. Capital was cheap and abundant and looking for somewhere to go. India, with its young population, rising smartphone penetration, and endless frictions waiting to be solved, looked like a compelling answer. The India story was not yet crowded. It was fresh.

For most of that decade, things worked more often than they didn’t. Founders were solving real, local problems with the intensity of people who had no safety net. Zomato figuring out food delivery logistics in a country where the restaurant supply chain was completely fragmented. Ola building ride-sharing in a market where organized taxi culture barely existed. Paytm pushed digital payments before most Indians trusted the idea of paying through a phone.They were stories of constraint meeting opportunity. We are very familiar today with all the titans born in those times.

Capital was available, but not indiscriminate. Scale still had to be built over time, and deployment retained a degree of discipline. The ecosystem was not being tested yet. It was being allowed to grow. But obviously, you still had to build your way into scale.

Policy support also played a role. The government added fuel. Startup India launched in 2016. The Fund of Funds for Startups, with a corpus of ₹10,000 crore, began committing capital to domestic AIFs, which in turn deployed into early-stage companies. The first crop of VC/PE funds started to see great action.

That is why the numbers from that decade look the way they do. We went from 42 registered AIFs in 2013 to about 1,800 in 2026. Commitments grew at over 50% annually over the last decade. The system crossed ₹7 lakh crore in commitments in the September 2022 quarter, within a decade of the AIF framework, a milestone that took mutual funds nearly four decades to reach. It was compounding at its best. And more importantly, it was happening in a largely protected environment.

The ecosystem was growing fast, in a good home, with a good foundation. In that sense, the ecosystem’s first decade was a lot like childhood. The foundation mattered more than the outcomes. The right environment, patient scaffolding, and early institutional support gave the system room to grow before it had to prove itself under pressure.

India, for most of its first decade, did not go through a comparable test.

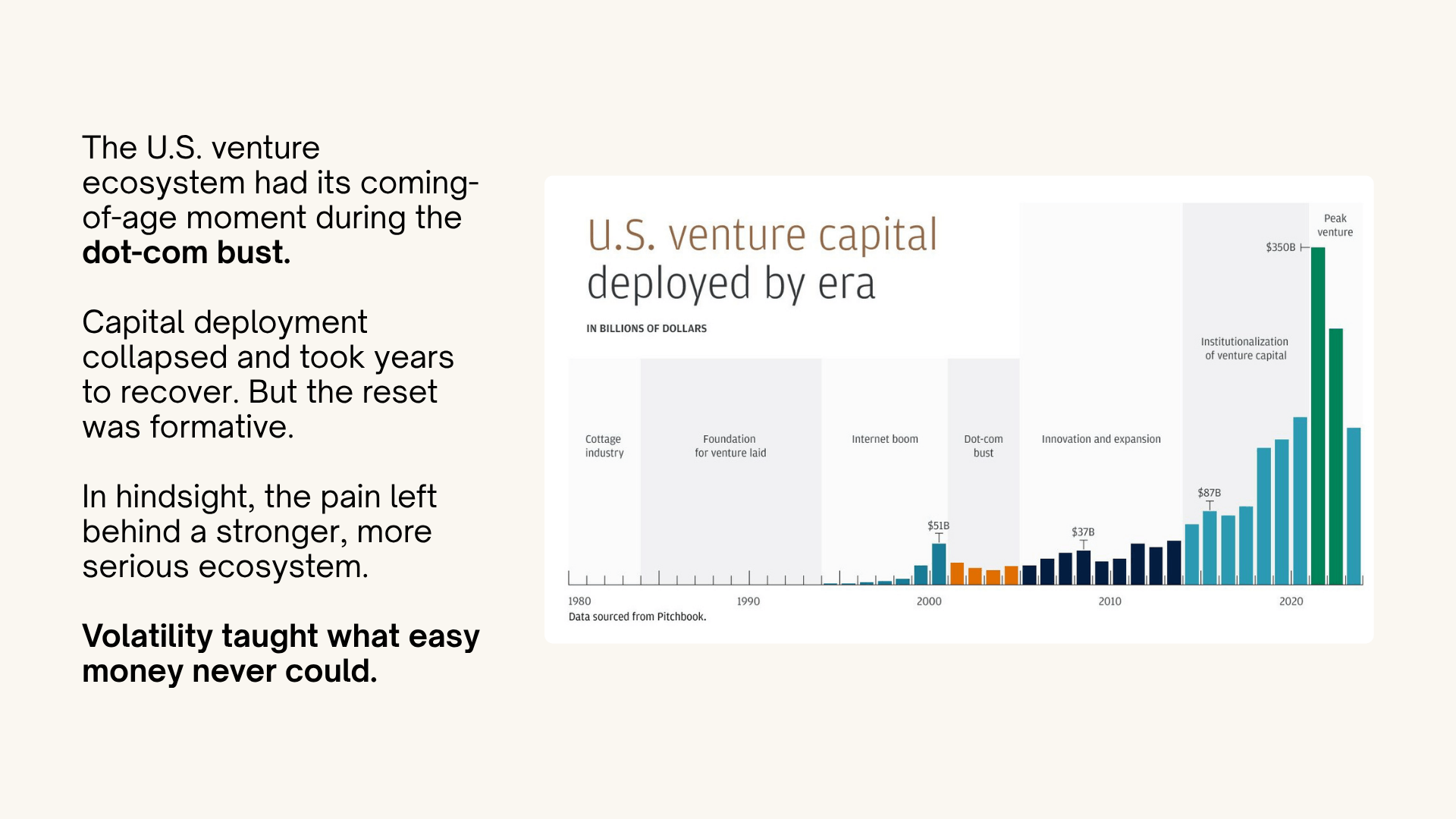

This stands in contrast to the US venture capital cycle. By the time the dot-com bust hit in the early 2000s, roughly $5 trillion in market value was erased and hundreds of funded companies failed in months. The funds and founders who came out the other side built differently in the decade that followed. Google, Amazon, and PayPal all navigated that bust. What they took from it were instincts about capital efficiency, business model durability, and governance discipline that their pre-2000 peers never had to develop.

Source: JP Morgan

(Caption for the chart: The U.S. venture ecosystem had its coming-of-age moment during the dot-com bust. Capital deployment collapsed and took years to recover. But the reset was formative. In hindsight, the pain left behind a stronger, more serious ecosystem. Volatility taught what easy money never could. )

A more recent example is China. Over the past decade, its technology and private market ecosystem expanded rapidly, supported by domestic capital and policy direction. But periodic regulatory interventions and capital tightening forced sharp resets. Entire sectors saw valuations compress, and business models were re-evaluated under new constraints. The outcome was similar. Survival required adaptation, and discipline became structural rather than cyclical.

India’s 2010s were different. The 2016 demonetisation shock was significant, but it also accelerated digital payments adoption in ways that benefited much of the ecosystem. The 2018 IL&FS crisis rattled credit markets but did not reshape how founders built or how fund managers deployed. Neither episode became a broad venture-market reset around valuations, burn, governance, and unit economics. Through most of the 2010s, India’s private market ecosystem remained broadly supported by liquidity, policy scaffolding, digital adoption, and a long runway for formalisation.

India’s private market ecosystem is now entering its own version of that transition. The environment has changed abruptly and repeatedly. The foundational years are behind us. The ecosystem has officially entered its teenage era: unpredictable, occasionally volatile, but ultimately where real character is built.

2020 Onwards: The First Real Test

If the 2010s were the nurturing years, 2021 was the ecosystem’s first unsupervised weekend. Post-COVID liquidity flooded the markets, and the Indian startup scene experienced something it had never seen before: irrational exuberance at scale.

Startups raised $38 billion in 2021, producing 44 unicorns in a single year. Rounds closed in days. Valuations were pegged to US comparables with entirely different unit economics. Disciplined investors watched peers deploy at unthinkable multiples and felt the squeeze to keep up.

For the first time, capital became impatient. And for the first time, the ecosystem responded to that impatience. Deployment cycles shortened, and expectations of growth accelerated.

The correction, when it came, was sharp. Startup funding dropped to $25 billion in 2022, then to $11 billion in 2023. Late-stage funding, the heartbeat of the “growth at all costs” era, fell by over 73% YoY in 2023.

The impact was not limited to funding volumes. The slowdown exposed structural weaknesses. Business models that depended on continued capital infusion became difficult to sustain. Governance lapses and inconsistencies in reporting came under greater scrutiny. The environment forced a reassessment of both what was being built and how it was being evaluated.

This period functioned as a filter. In 2021, conditions made a wide range of businesses appear viable. By 2023, capital required clearer evidence of durability. Companies had to justify their existence through unit economics, not just scale narratives.

Between 2023 and 2025, a large number of startups ceased operations. This was not an isolated disruption but part of a broader consolidation phase that most maturing ecosystems eventually undergo.

At the same time, the structure of capital began to shift. Domestic venture funds now account for a significantly larger share of overall funding than they did a decade ago. Public markets have also played a more active role, with a growing number of technology-led listings supported by domestic institutional and retail participation.

The ecosystem that has emerged from this period of ‘volatility’ is more measured. Capital is more selective, and expectations are more grounded in operating performance than in projected scale.

The ecosystem that has moved through the last five years is not a weakened one. It is a more aware one.

We are already seeing signs of that in how the market is behaving today. Capital has slowed, but it has not disappeared. Good businesses continue to raise, build, and, in many cases, reach the public markets. Across sectors, there is evidence of this shift. Space technology companies are moving from ambition to execution. AI-led businesses are being built with clearer use cases and monetisation pathways. Fintech, after its own reset, is seeing models that are more aligned with regulation and long-term viability.

There is a muscle being built here: the ability to operate within volatility. The fund managers who have deployed through this period have built judgement that cannot be learned in easier cycles. The founders building today are doing so under a different set of expectations. The system is no longer asking only how large something can become. It is asking why it should exist in the first place.

The first decade built the foundation. The recent years have begun to shape behaviour. At 14, the ecosystem is no longer early. It is not fully mature either. It is in that in-between phase where direction matters more than momentum.

And this is where the context of India matters. For an economy that is still expanding at this pace, building its private market ecosystem under conditions of volatility may not be a disadvantage. It may be a necessity. The demands of this market are too large to be carried by fragile businesses or undisciplined capital.

We do not know what the next decade will look like. The 2030s will likely bring their own cycles, their own excesses, and their own corrections. But if this phase does what it is supposed to do, we will enter that decade with a system that is more resilient, more selective, and more capable of carrying the weight of its own ambition.

At 14, the Indian private market ecosystem is behaving a lot like a teenager. It has outgrown the protected years, but it has not yet fully grown into itself. It has ambition, impatience, occasional overconfidence, and the first signs of self-awareness. The last few years have been an awkward but necessary education: learning that easy capital is not a personality, momentum is not maturity, and volatility is not always a punishment. Sometimes, it is the thing that teaches you how to stand straighter.

If this phase does what it is supposed to do, the twenties should look different. Not just bigger, but steadier. By then, the ecosystem should have a better relationship with risk, a clearer sense of judgement, and less dependence on favourable conditions to feel confident. Volatility will not disappear, but it may stop feeling like an interruption. It may simply become part of the operating system.

So when the ground moves, the shrug remains. More as a signal than indifference. The ecosystem is still adjusting, still learning, still growing into itself. But it is no longer surprised by the volatility around it.

And that, perhaps, is what coming of age looks like.

See you in May.

Jai Hind

TERMS OF USE

Thank you for your interest in our Website at https://unlistedintel.com/. Your use of this Website, including the content, materials and information available on or through this Website (together, the “Materials”), is governed by these Terms of Use (these “Terms”). By using this Website, you acknowledge that you have read and agree to these Terms.

NO OFFER, SOLICITATION OR ADVICE

Our site is provided for informational purposes only. It does not constitute to constitute (i) an offer, or solicitation of an offer, to

purchase or sell any security, other assets, or service, (ii) investment, legal, business, or tax advice, or an offer to provide such advice or (iii) a basis for making any investment decision.

The Materials are provided for informational purposes and have been prepared by Oister Global for informational purposes to acquaint existing and prospective underlying funds, entrepreneurs, and other company founders with Oister Global's recent and historical investment activities.

Please note that any investments or portfolio companies referenced in the Materials are illustrative and do not reflect the performance of any Oister Global fund as a whole. There is no obligation for Oister Global to update or alter any forward-looking statements, whether as a result of new information, future events, or otherwise.

PURPOSE LIMITATION AND ACCESS TO YOUR PERSONAL DATA:

We will only collect your personal data in a fair, lawful, and transparent manner. We will keep your personal data accurate and up to date. We will process your personal data in line with your legal rights. We use your name and contact details, such as email, postal address, and contact number to continue communications with you. We may also use your contact information to invite you to events we are hosting or to keep you updated with our news.

USE OF COOKIES OR SIMILAR DEVICES

We use cookies on our website. This helps us to provide you with a better experience when you browse our website and also allows us to make improvements to our site. You may be able to change the preferences on your browser or device to prevent or limit your device’s acceptance of cookies, but this may prevent you from taking advantage of some of our features.

MATERIAL

The material displayed on our site is provided “as is”, without any guarantees, conditions, or warranties as to its accuracy, completeness, or reliability. You should be aware that a significant portion of the Materials includes or consists of information that has been provided by third parties and has not been validated or verified by us. In connection with our investment activities, we often become subject to a variety of confidentiality obligations to funds, investors, portfolio companies, and other third parties. Any statements we make may be affected by those confidentiality obligations, with the result that we may be prohibited from making full disclosures.

MISCELLANEOUS

This Website is operated and controlled by Oister Global in India. We may change the content on our site at any time. If the need arises, we may suspend access to our site, or close it indefinitely. We are under no obligation to update any material on our site.

CONTACT INFORMATION

Any questions, concerns or complaints regarding these Terms should be sent to info@oisterglobal.com