Why India’s $180B AIF market is entering its realisation phase, and other insights from the third edition of No Ifs About AIFs.

Dear Reader,

The first edition asked whether India’s private markets could deliver. The second asked whether that delivery could hold across cycles.

The third moves beyond the question. It shows. And then it asks what comes next.

Every year, Oister and Crisil come together to benchmark how India’s AIF ecosystem is performing beyond the narrative. No Ifs About AIFs was built to bring transparency and trust to private markets through rigorous, comparable performance measurement.

Over the last two editions, many of you helped make this report part of the ecosystem itself. You shared it, debated it, and in some cases used it to ask harder questions of the funds you back. That engagement is a big reason No Ifs About AIFs has grown into a seminal industry benchmark, and a reference point that keeps showing up in allocator conversations.

India now stands at a consequential moment. A defining decade of growth is unfolding in a more demanding global environment, and private markets will be judged increasingly on outcomes.

As we built this third edition, it became clear that benchmarking alone was no longer enough. Performance still matters. Discipline still drives alpha. But as the ecosystem scales, liquidity becomes central. Outcomes now depend on how capital exits, recycles, and compounds.

This edition reflects that. It continues to benchmark performance, and it also examines liquidity, secondaries, realisation multiples, and the persistence of returns with a sharper lens.

We know the full report takes time, and we hope you will read it end to end when you can. In the meantime, we have curated the parts we would send a friend first: the charts that clarify what is working, what is changing, and what is starting to matter more. The full report is here when you are ready.

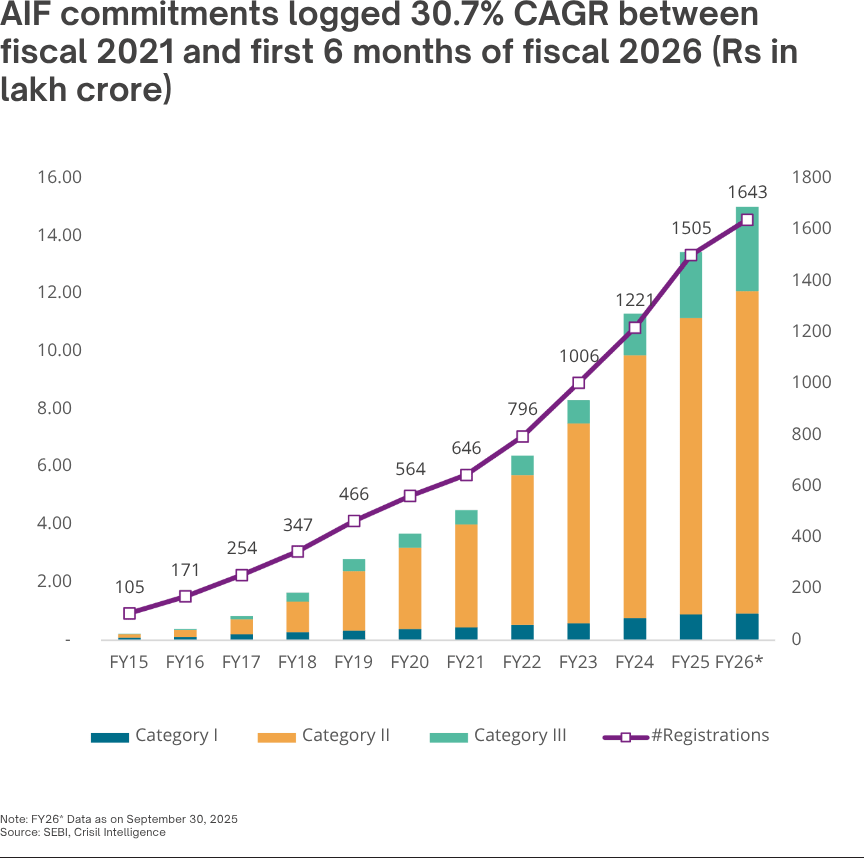

India built a ₹15 lakh crore private capital engine (AIFs) in under a decade

And the commitments have compounded at ~30.7% CAGR

Category I and II alone have grown at ~27.9% CAGR, reflecting allocator preference for equity and growth strategies.

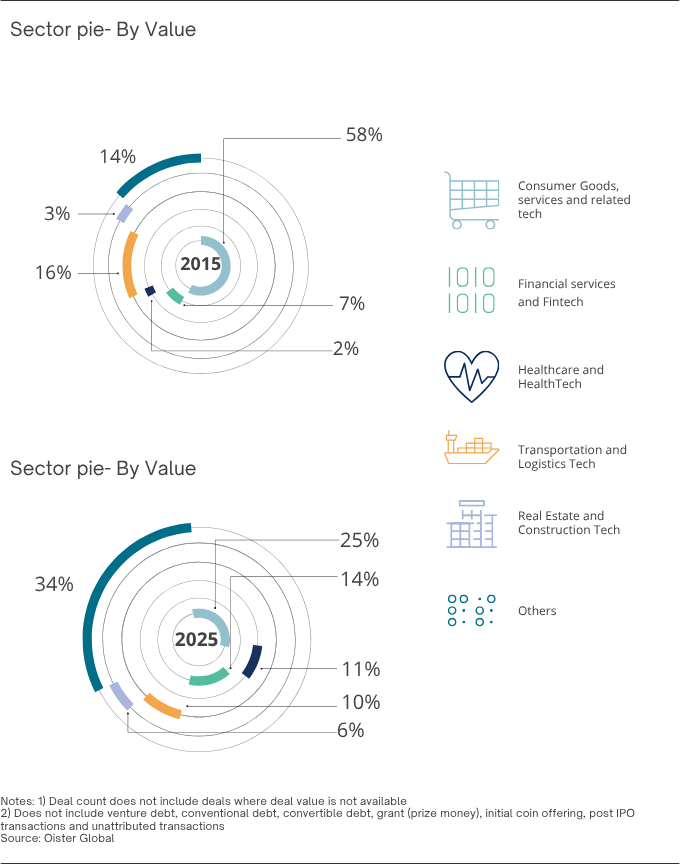

Over the past decade, India’s private markets have meaningfully diversified. The top five sectors’ share of deal value fell from 85.83% in FY15 to 66.31% in FY25 . Consumer and related tech dropped from 58% to ~25%, while financial services and fintech doubled from 7% to 14%.

Chart Reference: Compare the 2015 vs. 2025 “Sector Pie” on Page 13.

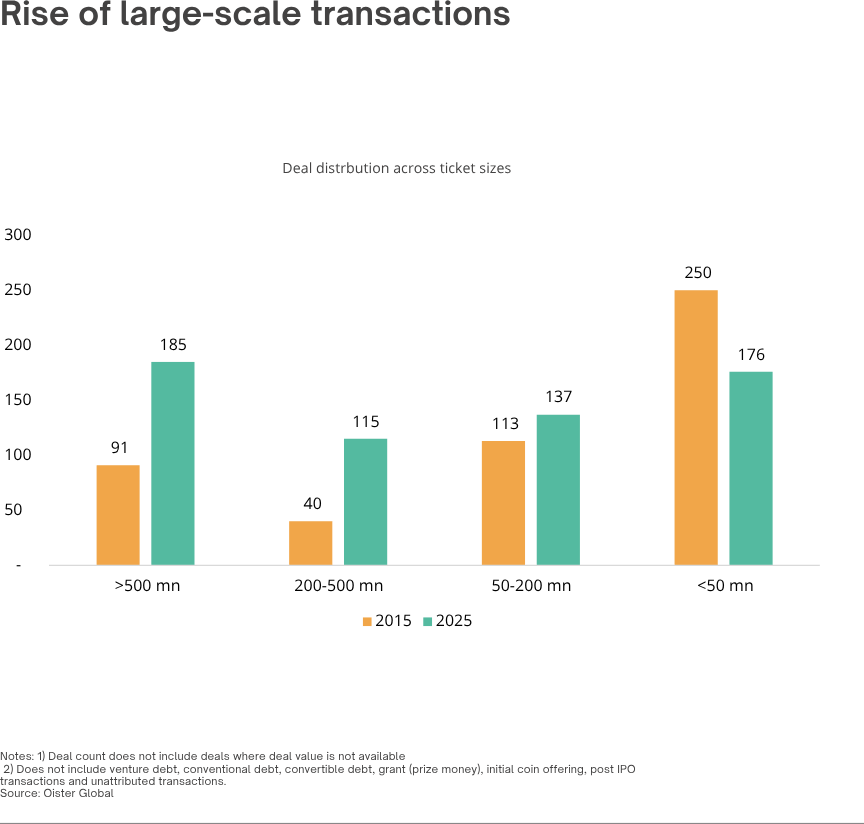

₹500mn+ deals aren’t the exception, now they make up 30% of observed deal flow

The share of deals above ₹500mn rose from ~18% (91 deals) in FY15 to 30% (185 deals) in FY25; these large deals made up ~90% of total deal value in FY25.

Chart PG 14

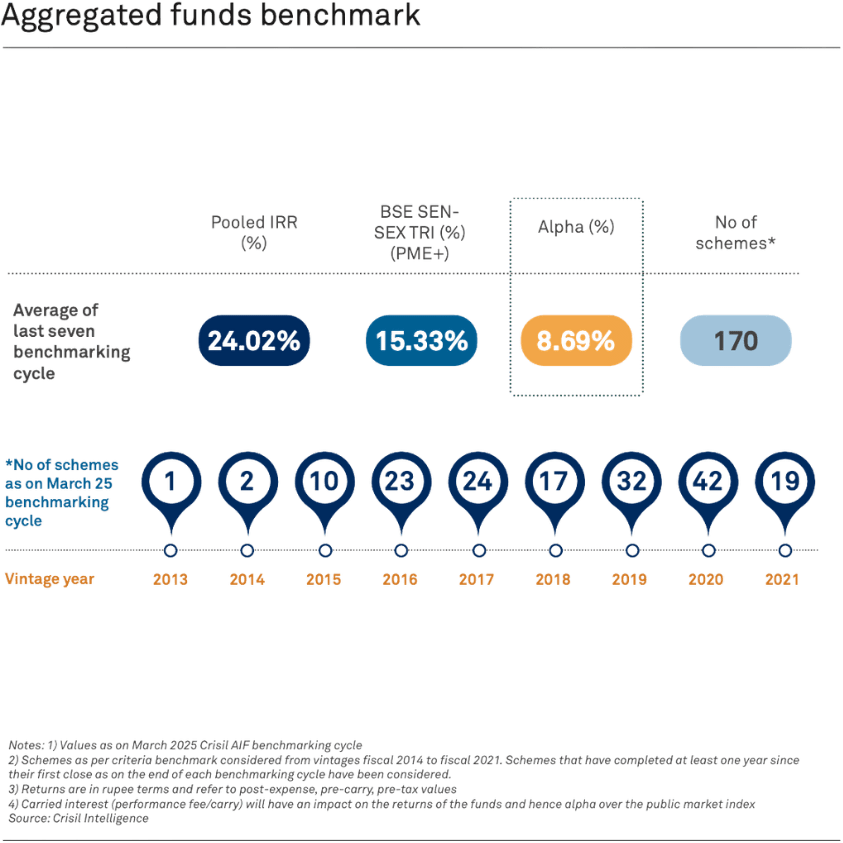

Across cycles, private market equity funds have consistently outperformed public benchmarks. The aggregated benchmark delivered an average alpha of ~8.69% over the BSE Sensex TRI across the last seven benchmarking cycles.

CHART – Page 28

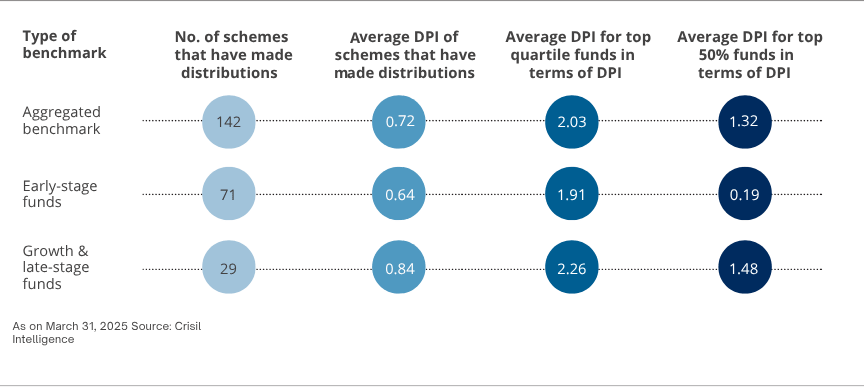

Returns are not evenly distributed. The right managers materially outperform.

While the overall AIF benchmark delivered ~8.7% alpha over public markets, the top half of managers generated 13.6% alpha, a very different outcome.

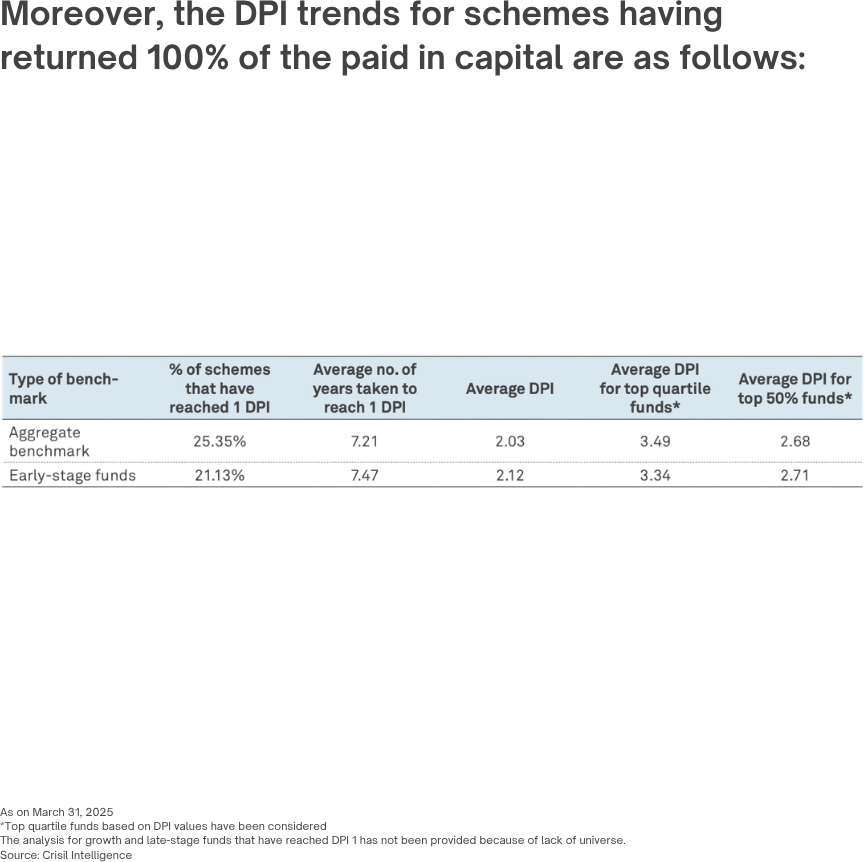

And when it comes to real money back, top-quartile funds that fully returned capital delivered an average 3.49x DPI, versus ~2.03x at the aggregate level.

Over 80% of the equity AIF schemes we benchmarked have now made distributions. Even better? More than 25% have already hit a DPI of 1.0x or higher.

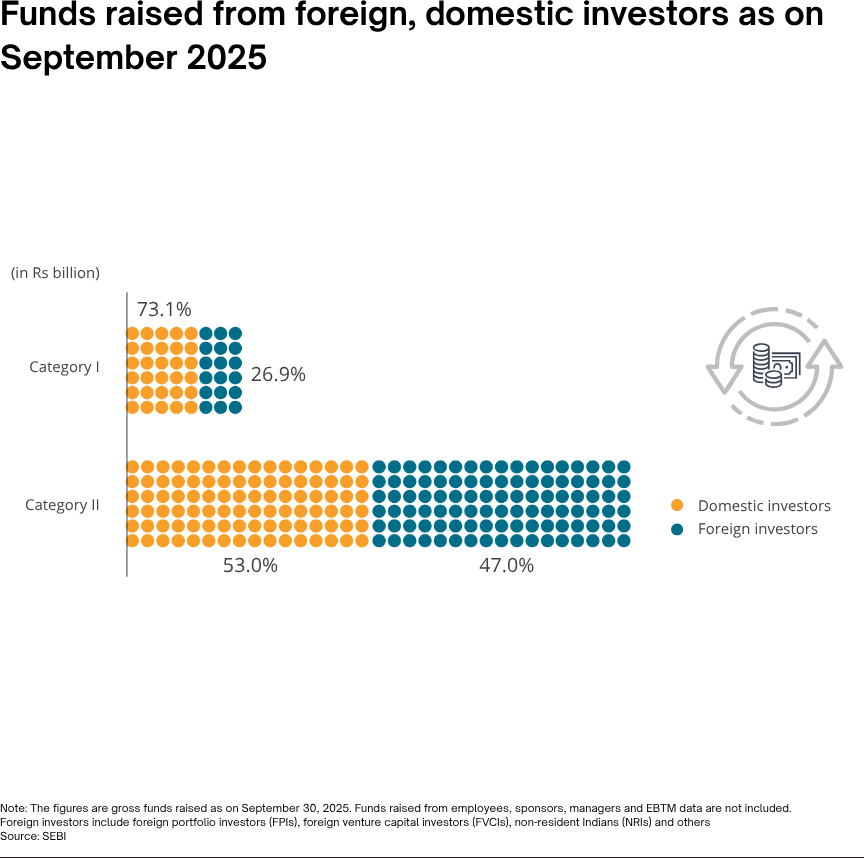

AIF capital pool is now majority-Domestic

Domestic participation in Category I & II AIFs rose from 50.3% (Mar ’24) to 55.3% (Sep ’25), with ₹1.14 lakh crore of incremental domestic inflows.

Chart pg 20

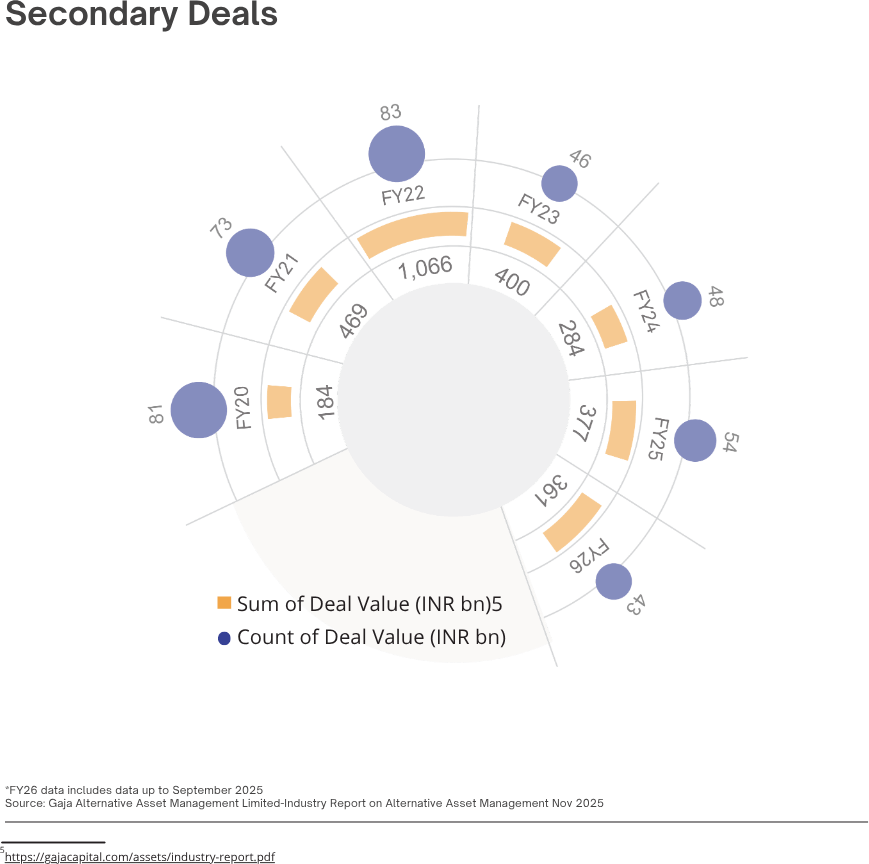

Over the past five years, the average secondary deal size in India has increased from ₹2.28 billion to ₹8.39 billion, a 3.7x rise that signals a clear shift toward institutional-scale transactions.

Secondary deal value reached approximately ₹377 billion in FY25, and the first half of FY26 alone has already recorded around ₹361 billion in secondary transactions.

Chart PG 34

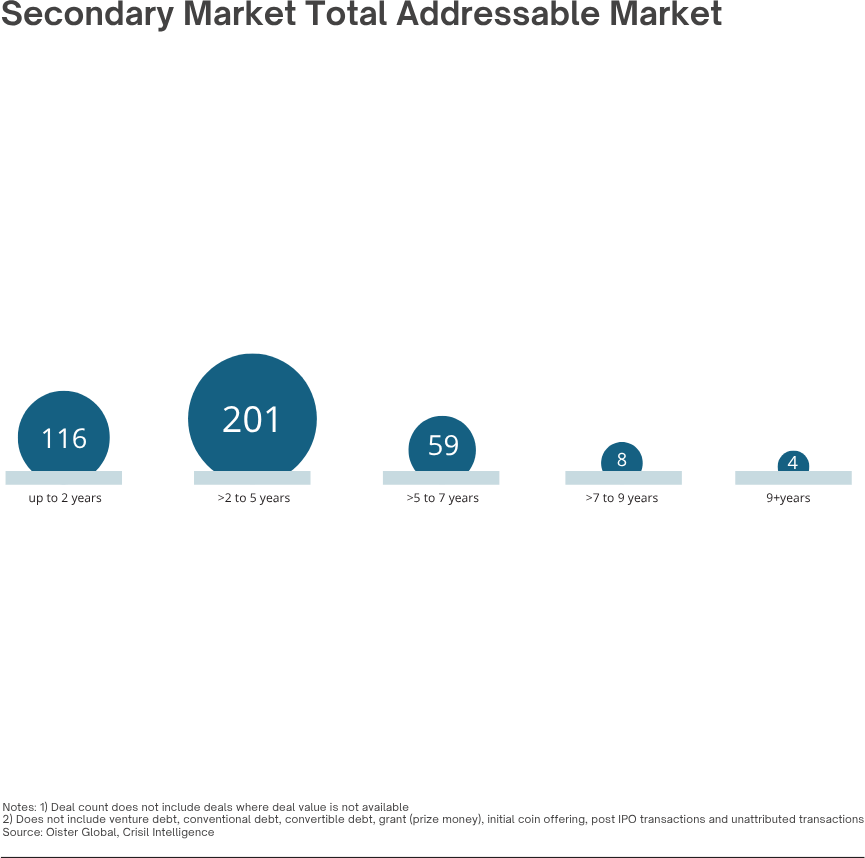

Half of Tracked Funded Startups Are Entering Liquidity Windows.

201 startups have moved from early-stage to growth in just 2–5 years.

That pace points to $26–$52B of secondary supply potentially ripening over 3–4 years.

Chart pg 35

We recently had the privilege of presenting this report to India’s Honourable Finance Minister, Smt. Nirmala Sitharaman. We see that moment as a reflection of how far India’s private markets have progressed. The conversation around private capital is now central to the country’s economic development, and we are grateful to contribute to it through this work.

The evidence points in one direction. India has the institutional foundation, the policy alignment, and the domestic savings base to deepen private markets at scale. What comes next is execution and the headroom to do more is real.

Trust follows transparency. That is why this report exists, and why we will keep doing it.

To everyone in the Unlisted Intel community, who reads carefully, shares generously, and pushes back when the data deserves harder questions, thank you. You are what keeps this report honest. We would love to hear your thoughts, as always.

See you in March!

Jai Hind

TERMS OF USE

Thank you for your interest in our Website at https://unlistedintel.com/. Your use of this Website, including the content, materials and information available on or through this Website (together, the “Materials”), is governed by these Terms of Use (these “Terms”). By using this Website, you acknowledge that you have read and agree to these Terms.

NO OFFER, SOLICITATION OR ADVICE

Our site is provided for informational purposes only. It does not constitute to constitute (i) an offer, or solicitation of an offer, to

purchase or sell any security, other assets, or service, (ii) investment, legal, business, or tax advice, or an offer to provide such advice or (iii) a basis for making any investment decision.

The Materials are provided for informational purposes and have been prepared by Oister Global for informational purposes to acquaint existing and prospective underlying funds, entrepreneurs, and other company founders with Oister Global's recent and historical investment activities.

Please note that any investments or portfolio companies referenced in the Materials are illustrative and do not reflect the performance of any Oister Global fund as a whole. There is no obligation for Oister Global to update or alter any forward-looking statements, whether as a result of new information, future events, or otherwise.

PURPOSE LIMITATION AND ACCESS TO YOUR PERSONAL DATA:

We will only collect your personal data in a fair, lawful, and transparent manner. We will keep your personal data accurate and up to date. We will process your personal data in line with your legal rights. We use your name and contact details, such as email, postal address, and contact number to continue communications with you. We may also use your contact information to invite you to events we are hosting or to keep you updated with our news.

USE OF COOKIES OR SIMILAR DEVICES

We use cookies on our website. This helps us to provide you with a better experience when you browse our website and also allows us to make improvements to our site. You may be able to change the preferences on your browser or device to prevent or limit your device’s acceptance of cookies, but this may prevent you from taking advantage of some of our features.

MATERIAL

The material displayed on our site is provided “as is”, without any guarantees, conditions, or warranties as to its accuracy, completeness, or reliability. You should be aware that a significant portion of the Materials includes or consists of information that has been provided by third parties and has not been validated or verified by us. In connection with our investment activities, we often become subject to a variety of confidentiality obligations to funds, investors, portfolio companies, and other third parties. Any statements we make may be affected by those confidentiality obligations, with the result that we may be prohibited from making full disclosures.

MISCELLANEOUS

This Website is operated and controlled by Oister Global in India. We may change the content on our site at any time. If the need arises, we may suspend access to our site, or close it indefinitely. We are under no obligation to update any material on our site.

CONTACT INFORMATION

Any questions, concerns or complaints regarding these Terms should be sent to info@oisterglobal.com