If India Doesn’t Back India, Who Will?

There’s an old story about a town whose lifeblood was a single well, sunk deep into the earth by a trader from a far-off city.

The water was clear, and for years the price was modest. Life revolved around its steady flow, festivals, markets, marriages, all watered by that distant man’s generosity.

Then one summer, the rains failed. The trader, facing shortages of his own, raised his rates overnight. The town could pay or go thirsty. Many argued it was cheaper to endure than to toil; after all, digging a new well meant months of sweat, uncertainty, and the risk of finding nothing.

But a small group of farmers, masons, and a widow who had seen too many dry seasons, began to dig. Day after day, calloused hands cut into the stubborn earth. The work was slow, the setbacks frequent. Weeks turned into months. And then, in the heat of late summer, the ground softened, and water rose to meet them.

The new well did more than quench thirst. It shifted the town’s spine. They still drew from the trader’s well when it made sense, for special occasions, but they no longer feared the tightening of a distant fist. The choice, and the water, were theirs. And in that choice lay a kind of wealth that silver could never buy.

In capital, as in water, the wells you dig yourself change more than your supply, they change your spine. The well is only a story, but in truth we’ve lived it before – in our farms, our factories, our markets, moments when we dug for ourselves and found the reserves to carry us further than trade alone ever could.

And this August, as India marks its 79th Independence Day, that truth feels more real than ever. We have learned to trade with the world, to absorb its science, to ride its capital flows. But 2025 has reminded us, in tariffs, in technology bans, in the sheer volatility of global money – that the most enduring independence is the kind you fund yourself.

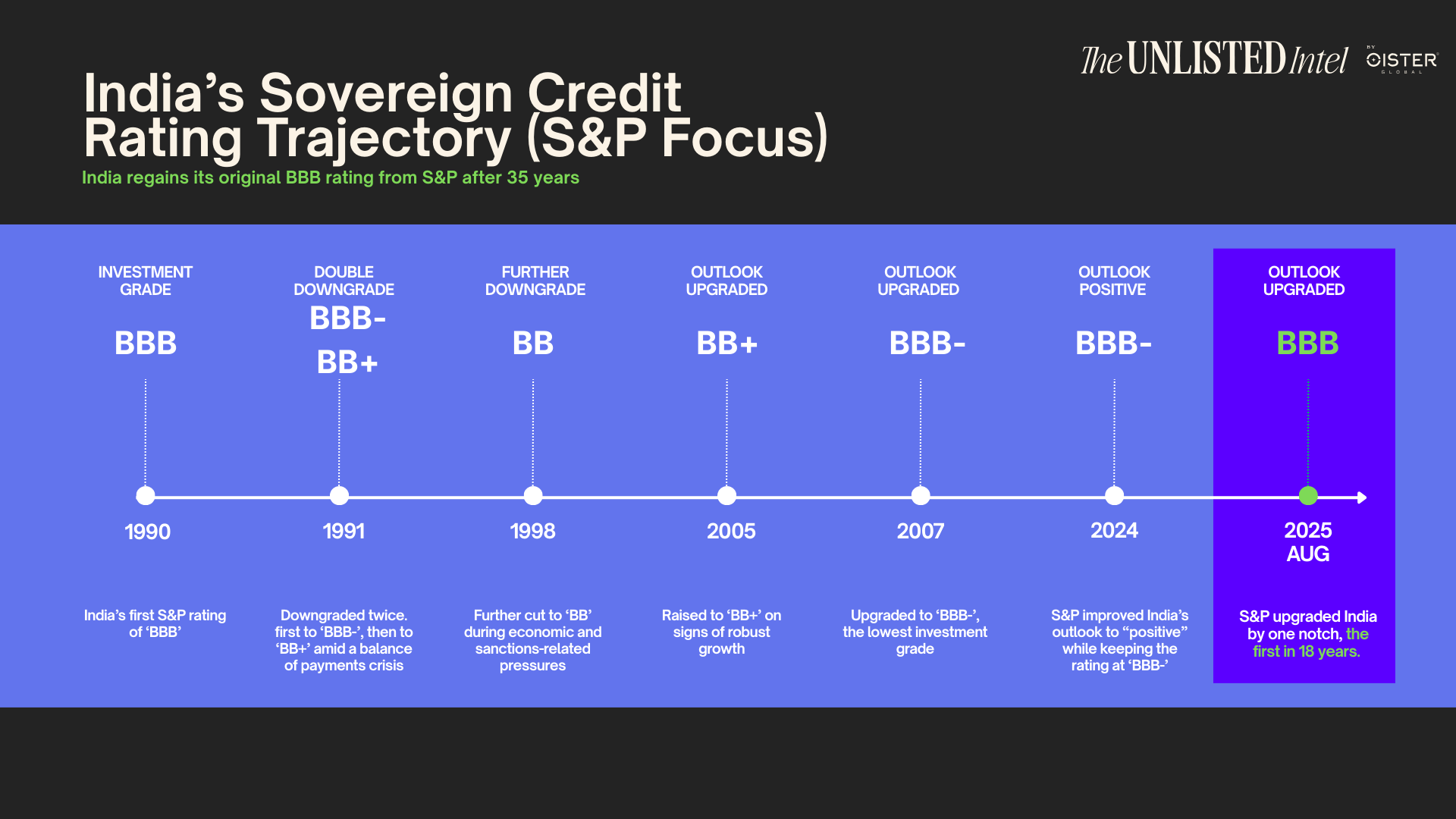

Which is why the announcement on the eve of Independence Day matters so much. For the first time in eighteen years, S&P upgraded India’s sovereign credit rating from BBB- to BBB. The last time we moved up a notch was in 2007.

Back then, GDP was $1.2 trillion. Foreign Exchange Reserves were $199.2 billion. Mutual fund AUM barely ₹5.2 trillion (~$110 billion). Today, GDP is nearing $4.2 trillion, reserves are $688 billion, and mutual fund AUM is over ₹75 trillion (~$860 billion).

The 2007 upgrade was an invitation to borrow from the world; the 2025 upgrade is recognition that the world wants to lend to us.

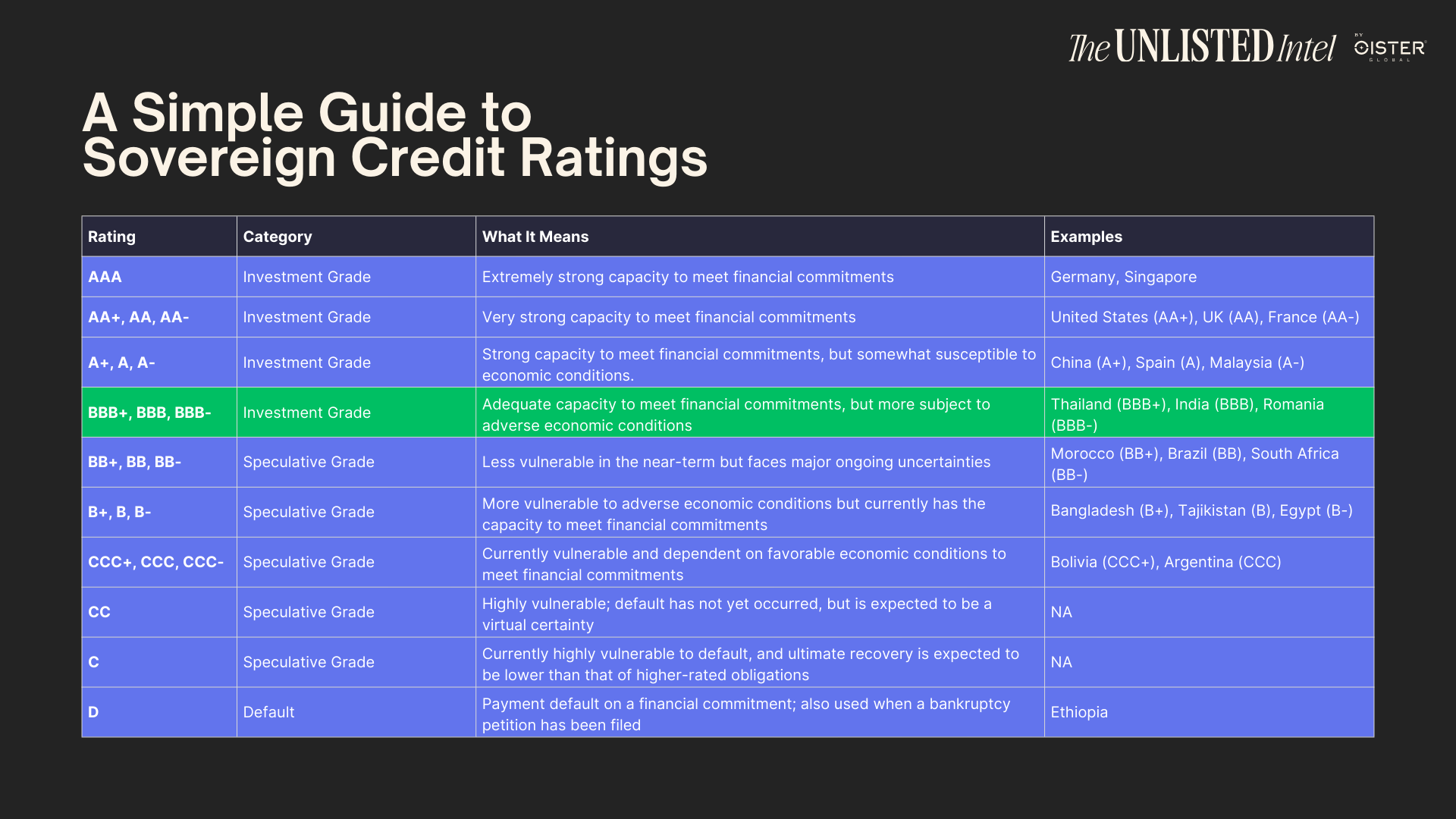

Sovereign ratings are like a country’s credit score , they decide who will lend to us, on what terms, and in what size. Moving from BBB- to BBB means more global pension funds, insurers, and bond indices can hold our debt. It means cheaper borrowing for infrastructure, industry, and innovation.

This rating is the byproduct of a deeper flywheel:

When we grow our own capital pools, we reduce dependence on external borrowing. When we depend less on external borrowing, our sovereign profile strengthens. When our profile strengthens, our ratings rise. Higher ratings lower the cost of capital. Cheaper capital fuels more growth at home. And that growth expands the depth of our own capital pools.

The more we have, the less we need from the world. The less we need, the more we get and on better terms.

India’s climb from BBB- to BBB has been unusually long with eighteen years on the bottom rung of investment grade. But time has worked in our favour. Those years weren’t idle; they were years spent building deeper reserves, a broader investor base, and the beginnings of a domestic capital market that can fund growth on its own terms.

India took its time. The growth wasn’t lacking, our GDP outpaced most peers, but only now do we have the balance sheet and the capital ecosystem to sustain it. While others raced upward on foreign inflows, India’s climb is increasingly powered by capital dug from its own well.

In the days before Independence Day, some of India’s most recognisable business voices: Harsh Goenka, Deepinder Goyal, struck the same note: it is time to build in India, for India.

The Prime Minister’s speech carried the same charge. For those of us in private markets, that call is not abstract. We are the builders of capital itself. We decide whether the next cycle of India’s growth is financed from Mumbai or Manhattan. The onus is ours, because the option is gone.

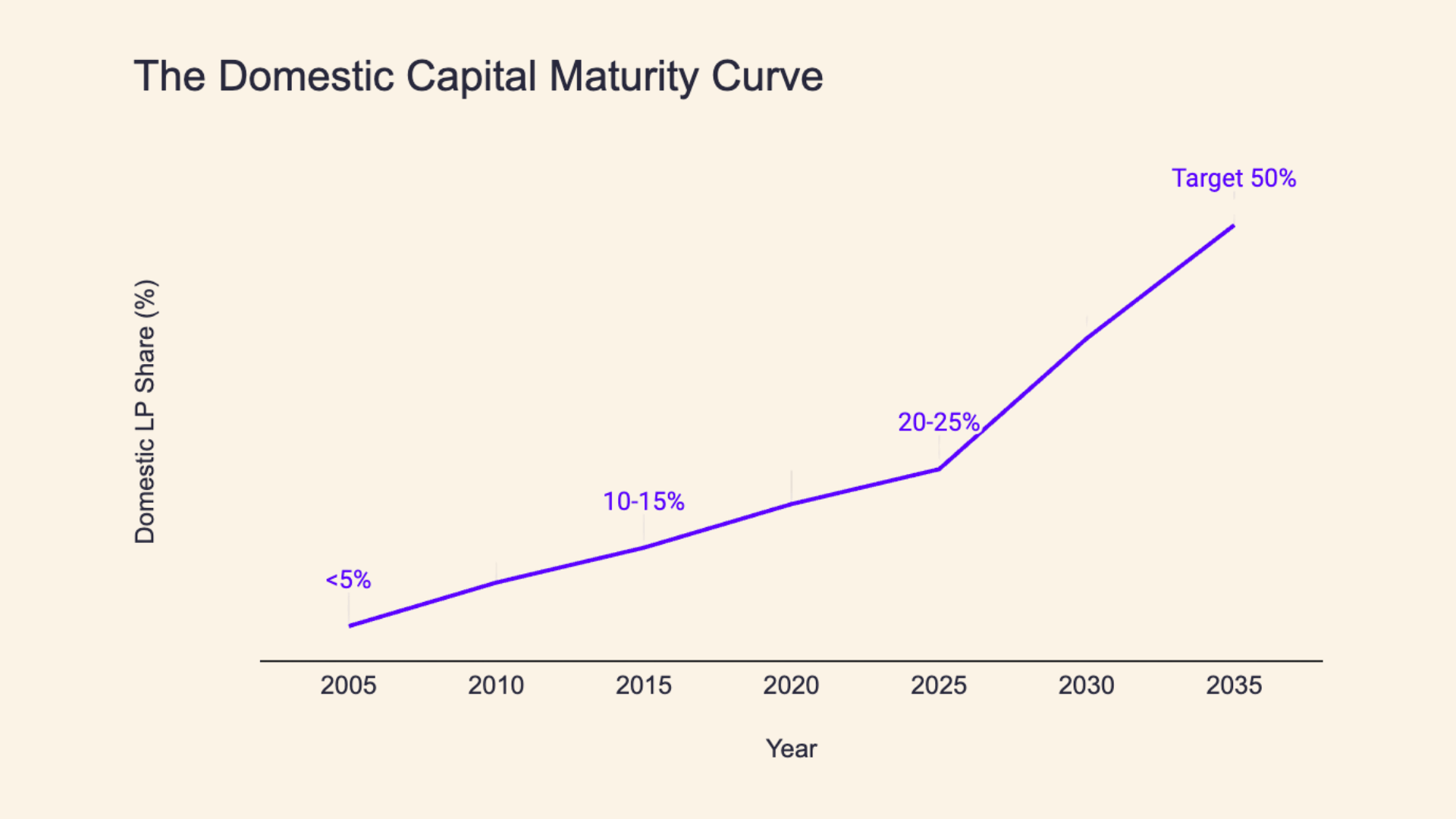

For most of India’s unicorn era, the fuel was overwhelmingly foreign. Global giants like Sequoia, Tiger Global, and SoftBank dominated the cap tables, shaping the ownership of household names from Flipkart and Paytm to Ola, Swiggy, and Zomato. This was not a failure. At the time, India simply did not have the deep domestic VC pools to match the ambition of its founders. But it also meant that when these companies exited, the majority of wealth was repatriated abroad.

Which means that for most of our unicorn era, every big exit sent more money back to foreign lands than it kept in Indian hands.

Note: The figures above are directional estimates, assembled from publicly available industry commentary and are not precise or audited datapoints. They represent a broad trend: domestic LP share in India’s PE/VC has risen over the last two decades, but still trails institutional global capital.

Local capital doesn’t demand currency hedges. It doesn’t flinch at every emerging-market headline. It doesn’t need a roadshow to believe in the India story. And when global liquidity tightens, the capital that stays is the capital you’ve grown yourself.

That tide is finally turning. According to Bain India Venture Capital Report , over 90% of new venture fundraising in India in 2023 came from domestic funds, a reversal as sharp as the one already seen in public markets, where domestic investors now drive the majority of daily trading volumes, a complete inversion from two decades ago.

Family offices and HNIs have stepped up as anchor LPs in mid-market funds. Large domestic institutions are beginning to enter selectively, supported by gradual regulatory changes. Government-backed fund-of-funds through SIDBI and NIIF have played a catalytic role in seeding Indian venture funds over the past two decades.

But the big pools, pensions and insurers remain largely untapped. Unlocking them could double domestic LP share within a decade. Indian capital funding Indian innovation. Indian innovation creating Indian wealth. Indian wealth reinvested in the next cycle.

At Oister, as one of India’s premier alternative assets managers, we’ve tried to walk this talk from day one. In just over two years, every fund we’ve launched has carried the same throughline: deepen the domestic LP base so Indian companies are powered by Indian capital. We know we are one of many players in a vast $4.2 trillion economy. But we believe our work is part of the long game, where every rupee raised at home strengthens the sovereign balance sheet, reduces dependence on foreign capital, and compounds into a more resilient Bharat.

If you’re reading this, you already care about India’s private markets as a force shaping our economic destiny. In 2024, India’s PE/VC market closed $43 billion in deals, second only to China in Asia. We now have more than 120 unicorns. Private-capital-backed companies have become a meaningful part of India’s economy, contributing materially to growth and employment. This asset class is now one of the engines driving India forward. And yet, a significant part of the capital fuelling it still comes from overseas LPs. With each passing day, the urge to build in India and keep the wealth it creates at home grows stronger. India needs to build India.

Last year, we wrote about how the world had underestimated India, and why that was a mistake. This year, the proof came stamped in our sovereign upgrade. By the time we meet for our 80th Independence Day, I hope we will see a nation that dug deeper wells, kept more of its wealth at home, and proved that the more we have, the less we need.

Thank you and Jai Hind!

TERMS OF USE

Thank you for your interest in our Website at https://unlistedintel.com/. Your use of this Website, including the content, materials and information available on or through this Website (together, the “Materials”), is governed by these Terms of Use (these “Terms”). By using this Website, you acknowledge that you have read and agree to these Terms.

NO OFFER, SOLICITATION OR ADVICE

Our site is provided for informational purposes only. It does not constitute to constitute (i) an offer, or solicitation of an offer, to

purchase or sell any security, other assets, or service, (ii) investment, legal, business, or tax advice, or an offer to provide such advice or (iii) a basis for making any investment decision.

The Materials are provided for informational purposes and have been prepared by Oister Global for informational purposes to acquaint existing and prospective underlying funds, entrepreneurs, and other company founders with Oister Global's recent and historical investment activities.

Please note that any investments or portfolio companies referenced in the Materials are illustrative and do not reflect the performance of any Oister Global fund as a whole. There is no obligation for Oister Global to update or alter any forward-looking statements, whether as a result of new information, future events, or otherwise.

PURPOSE LIMITATION AND ACCESS TO YOUR PERSONAL DATA:

We will only collect your personal data in a fair, lawful, and transparent manner. We will keep your personal data accurate and up to date. We will process your personal data in line with your legal rights. We use your name and contact details, such as email, postal address, and contact number to continue communications with you. We may also use your contact information to invite you to events we are hosting or to keep you updated with our news.

USE OF COOKIES OR SIMILAR DEVICES

We use cookies on our website. This helps us to provide you with a better experience when you browse our website and also allows us to make improvements to our site. You may be able to change the preferences on your browser or device to prevent or limit your device’s acceptance of cookies, but this may prevent you from taking advantage of some of our features.

MATERIAL

The material displayed on our site is provided “as is”, without any guarantees, conditions, or warranties as to its accuracy, completeness, or reliability. You should be aware that a significant portion of the Materials includes or consists of information that has been provided by third parties and has not been validated or verified by us. In connection with our investment activities, we often become subject to a variety of confidentiality obligations to funds, investors, portfolio companies, and other third parties. Any statements we make may be affected by those confidentiality obligations, with the result that we may be prohibited from making full disclosures.

MISCELLANEOUS

This Website is operated and controlled by Oister Global in India. We may change the content on our site at any time. If the need arises, we may suspend access to our site, or close it indefinitely. We are under no obligation to update any material on our site.

CONTACT INFORMATION

Any questions, concerns or complaints regarding these Terms should be sent to info@oisterglobal.com