The pains of cross-border regulatory complications are something that affects even the corporate giants in the world. Take the example of Meta, for instance. In 2023, Meta was fined $1.3 billion for failing to comply with the data privacy laws in the EU. This stern ruling from Ireland’s Data Protection Commission came after repeated warnings.

The private equity industry is no different. As investors look to expand their portfolios across borders, they are met with a multitude of regulations that can make surviving in this industry difficult.

To succeed in this high-stakes game, private equity firms need to be strategic and have a deep understanding of the nuances of cross-border regulations. Cross-border compliance includes things like managing risks, having good internal controls, doing research on partners and clients, keeping an eye on things and reporting back when needed, being aware of different cultures and ethics, and being careful with transferring data. It’s an ongoing process for the fund to know and follow the laws of all the places they operate in and want to operate in, to ensure they are responsible and transparent.

In this grey area, where opportunity and regulation collide, finding the right balance can be a great challenge. This chapter discusses the difficulties PE firms may face in the cross-border regulatory world and how they can overcome them.

The financial industry has always relied on conducting business activities across borders. However, with stricter regulations and increasing legal and reputational risks, financial institutions with an international customer base face significant challenges in complying with country-specific regulations.

To address this, ensuring strict adherence to local provisions has become a critical issue for any financial institution. This is known as cross-border compliance.

International private equity transactions can be tricky due to tax and structuring challenges. Investors who reside in their home country and conduct transactions and exits in the target country may face double taxation, which can take away a sizable chunk of their earnings.

However, there are ways to deal with this issue. To give an example, tax treaties and structuring investments through tax-efficient jurisdictions can help reduce the impact of double taxation.

In addition, it’s crucial to observe anti-money laundering (AML) and Know Your Customer (KYC) requirements when dealing with cross-border private equity deals. Investors must conduct a thorough AML due diligence process to prevent the misuse of funds for illicit activities.

A well-structured cross-border private equity transaction involves clear transaction terms and robust paperwork. It’s essential to give adequate attention to legal, regulatory, and commercial considerations when negotiating international agreements. Contractual and governance concerns are critical to protect the rights and interests of all parties involved.

Another critical element to consider is the protection of intellectual property rights (IPR). In cross-border transactions, IPR can be difficult to enforce, which makes it necessary to deploy severe safeguards to protect them and prevent associated risks.

Overall, cross-border private equity transactions require careful planning and execution to ensure their success. By following the right strategies and considerations, investors can minimise risks and maximise their returns while helping to prevent any potential legal or financial issues.

Operating in multiple countries can pose significant challenges for the fund when it comes to compliance. After all, people operate differently in different parts of the world. A greeting in one country could even be considered an offence in another if you’re not careful!

PE firms, too, have to be cautious when dealing with cross-border investments. The last thing they would want is to ruffle feathers and get into additional complications.

Cross-border compliance challenges can take various forms, including different regulatory frameworks, laws, and cultural norms. These complexities can create hurdles for organisations that must ensure compliance across economies, requiring them to address various legal, regulatory, and operational aspects.

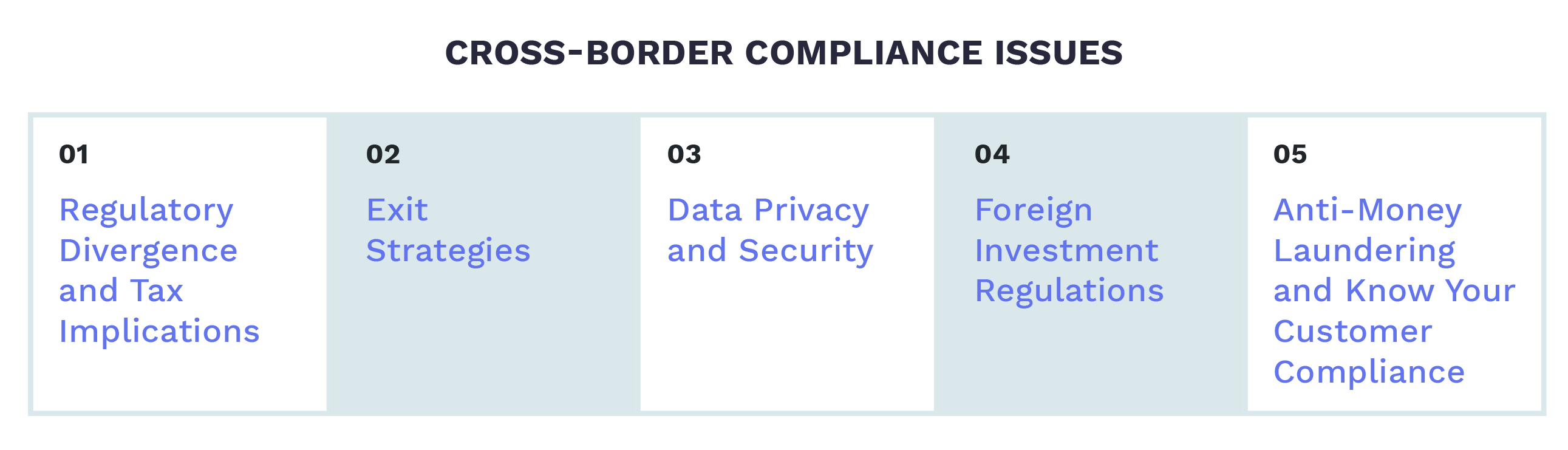

Some of the common cross-border compliance issues that the fund may face include:

For instance, each country has its own regulations governing taxes, investment activities, labor laws, and corporate governance. This means that private equity firms have to understand and comply with these regulations, which can differ significantly from one jurisdiction to another. They also need to navigate complex tax regimes, ensuring they comply with local tax laws while optimising their investment returns. Additionally, many countries impose restrictions or limitations on foreign investments, particularly in sensitive sectors such as defense, telecommunications, and finance.

Exiting investments in developed countries is relatively easy due to established financial infrastructures and regulations. However, in developing countries, it can be challenging and expensive due to varying financial institutions and laws. Repatriating proceeds requires a good understanding of investment laws, tax, and employment regulations to ensure profitability.

Cross-border investments also involve the transfer and storage of sensitive data across multiple jurisdictions, which raises concerns about data privacy and cybersecurity. Private equity firms face challenges regarding data protection laws, such as GDPR, when handling sensitive information in cross-border transactions. These firms need to ensure compliance with data protection laws and implement robust security measures to safeguard confidential information.

Foreign investments in certain industries or sectors are restricted in many countries due to national security or strategic reasons. Private equity firms must comply with these regulations, which may differ across jurisdictions.

The disputes arising from cross-border transactions may involve legal proceedings in multiple jurisdictions, each with its own legal system and enforcement mechanisms. Private equity firms need to anticipate potential disputes and develop effective strategies for resolving conflicts, including arbitration or mediation

Private equity firms must check their investors and counterparties to comply with Anti-Money Laundering (AML) and KYC regulations. However, meeting these regulations in different places is hard because of different standards and requirements.

Information, information, information. Overcoming these challenges is all about being in the know. PE firms need to focus on getting the tea when it comes to cross-border regulatory requirements.

Let’s understand how PE firms can overcome these challenges:

Investing in emerging markets can be challenging due to limited access to reliable information. Private equity investors must conduct thorough primary data collection and analysis of the portfolio companies, government regulations, and cultural, religious, and environmental issues. This due diligence is crucial for success, but it’s new to most private equity investors. The key is to be willing to invest in understanding the market.

Finding and hiring top local management talent is crucial for successful investment in most developing countries. However, the pool of local managers is often limited. In such cases, an HR firm with local networks is essential to hire a local executive manager or bring in an expat.

Private equity firms investing in developing countries need to plan exit strategies early, considering ownership restrictions, local currency regulations, and taxes. Regulations and tax codes in these economies are often volatile, so investors must continuously monitor and reposition their investments. Being proactive and adaptable is key to success.

Private equity firms should work closely with tax advisors when doing cross-border transactions. They need to focus on creating tax-efficient deal structures and follow transfer pricing regulations to optimise tax implications. This is essential to minimise tax-related risks.

Private equity firms must adapt to meet regulatory requirements in different regions by designing flexible transaction structures. This involves considering alternative deal structures or financing options that align with specific regulatory rules. The key is to be flexible and find creative solutions.

Private equity firms need a regulatory intelligence system to stay updated on global regulatory changes. Regular monitoring of legal and compliance requirements is a must to adapt strategies and control cross-border compliance issues. The key is to be proactive and adaptable.

TERMS OF USE

Thank you for your interest in our Website at https://unlistedintel.com/. Your use of this Website, including the content, materials and information available on or through this Website (together, the “Materials”), is governed by these Terms of Use (these “Terms”). By using this Website, you acknowledge that you have read and agree to these Terms.

NO OFFER, SOLICITATION OR ADVICE

Our site is provided for informational purposes only. It does not constitute to constitute (i) an offer, or solicitation of an offer, to

purchase or sell any security, other assets, or service, (ii) investment, legal, business, or tax advice, or an offer to provide such advice or (iii) a basis for making any investment decision.

The Materials are provided for informational purposes and have been prepared by Oister Global for informational purposes to acquaint existing and prospective underlying funds, entrepreneurs, and other company founders with Oister Global's recent and historical investment activities.

Please note that any investments or portfolio companies referenced in the Materials are illustrative and do not reflect the performance of any Oister Global fund as a whole. There is no obligation for Oister Global to update or alter any forward-looking statements, whether as a result of new information, future events, or otherwise.

PURPOSE LIMITATION AND ACCESS TO YOUR PERSONAL DATA:

We will only collect your personal data in a fair, lawful, and transparent manner. We will keep your personal data accurate and up to date. We will process your personal data in line with your legal rights. We use your name and contact details, such as email, postal address, and contact number to continue communications with you. We may also use your contact information to invite you to events we are hosting or to keep you updated with our news.

USE OF COOKIES OR SIMILAR DEVICES

We use cookies on our website. This helps us to provide you with a better experience when you browse our website and also allows us to make improvements to our site. You may be able to change the preferences on your browser or device to prevent or limit your device’s acceptance of cookies, but this may prevent you from taking advantage of some of our features.

MATERIAL

The material displayed on our site is provided “as is”, without any guarantees, conditions, or warranties as to its accuracy, completeness, or reliability. You should be aware that a significant portion of the Materials includes or consists of information that has been provided by third parties and has not been validated or verified by us. In connection with our investment activities, we often become subject to a variety of confidentiality obligations to funds, investors, portfolio companies, and other third parties. Any statements we make may be affected by those confidentiality obligations, with the result that we may be prohibited from making full disclosures.

MISCELLANEOUS

This Website is operated and controlled by Oister Global in India. We may change the content on our site at any time. If the need arises, we may suspend access to our site, or close it indefinitely. We are under no obligation to update any material on our site.

CONTACT INFORMATION

Any questions, concerns or complaints regarding these Terms should be sent to info@oisterglobal.com