Waiting isn’t going away. But thanks to secondaries, investors now decide how the story ends.

Welcome, dear reader.

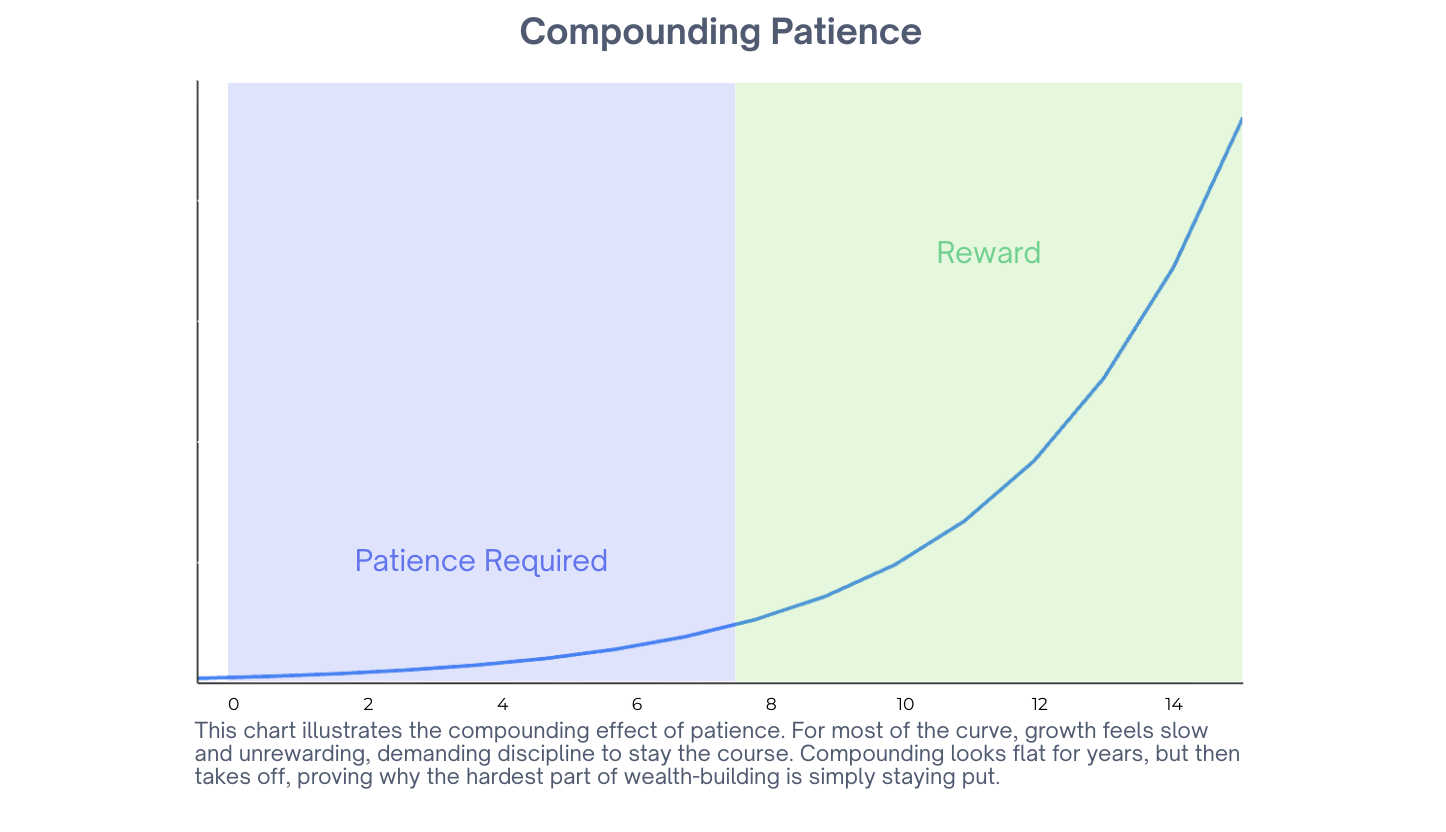

This edition of The Unlisted Intel is about Patience.

Patience is supposed to be a virtue. And if you’re anything like me, you can already think of a few places where you wish you had more of it.

This is the world we live in: we cancel an Uber if it’s running five minutes late and feel cheated if our groceries don’t show up in under fifteen. We won’t sit through a 30-second ad, even though not long ago we’d watch a song buffer line-by-line on a computer screen. We refresh tracking links every hour, swipe away movies after ten minutes if they don’t grip us, and tap furiously when the Wi-Fi lags for two seconds. We used to wait weeks for letters in the post, today we’re offended if a WhatsApp text takes more than five seconds to get a blue tick.

And yet, for all our day-to-day impatience, we’ve built our wealth on waiting. Fixed deposits have been our heroes, compounding for decades. Across the country, there’s over ₹100 trillion parked in FDs. Then came the PPF, with its 15-year lock-in, usually the first thing your parents nudged you to open. Gold and land were never investments to be traded; they were heirlooms polished, prayed over, and passed down. The earliest Reliance shareholders held tiny allotments through volatile decades, watching them turn into dynastic wealth. Families with LIC policies in the 70s and 80s treated them as time capsules that matured just in time for a child’s wedding or business.

Patience, in short, has been the operating system of Indian wealth.

By now, you’ve probably connected the dots. Which brings me to the point. If there’s one asset class that should feel second nature to us, it’s private markets: the world of unlisted startups and businesses. They’ve always been about giving businesses the time to stumble, steady themselves, and eventually scale. In many ways, the entire premise of the asset class is summed up in that old line: all good things come to those who wait.

But here’s the twist: in today’s world, that kind of patience is wearing thin.

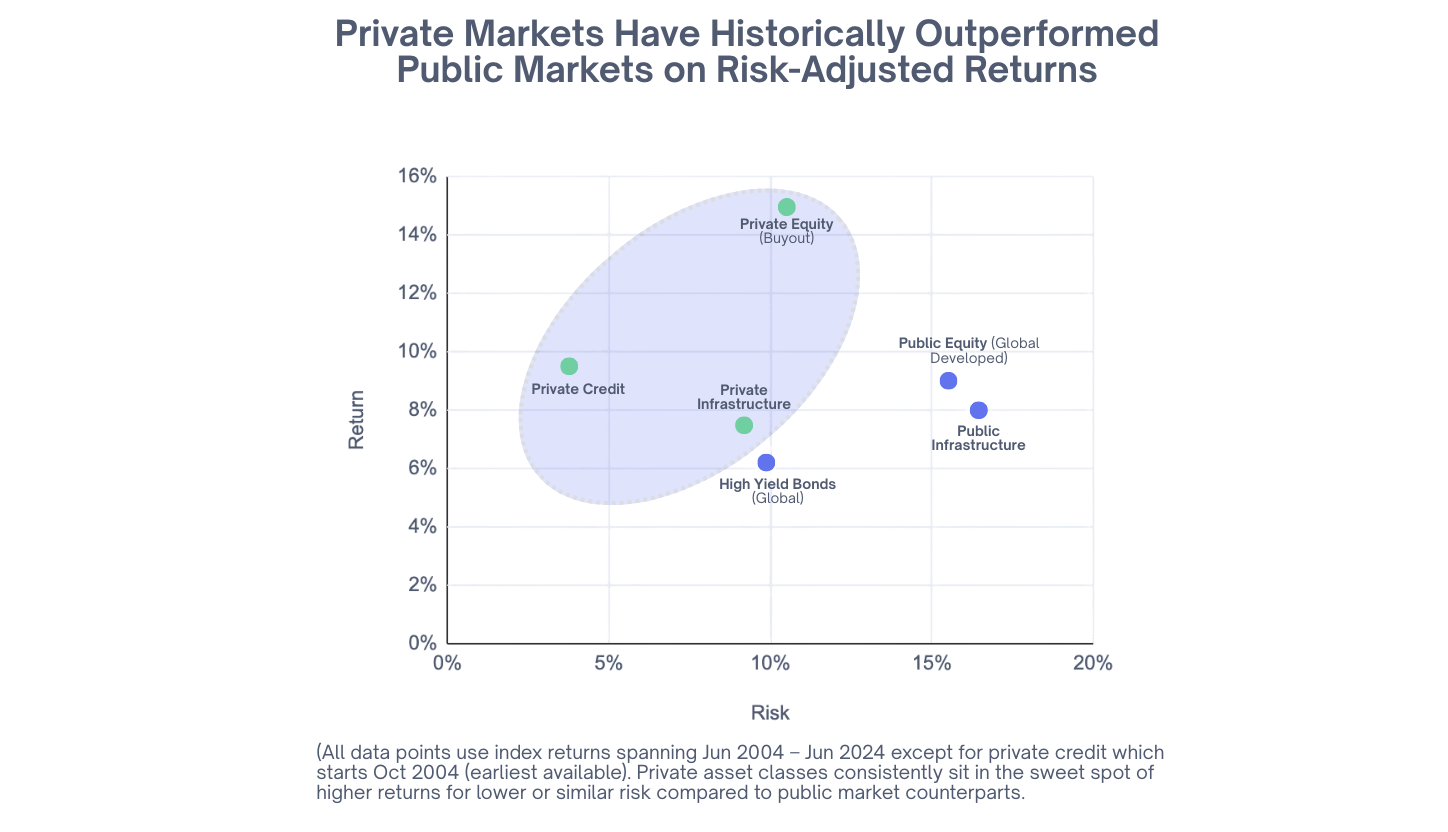

Indian investors, including institutions, family offices, HNIs, already understand the power of this asset class. Research we do with Crisil annually shows that AIFs in India have historically delivered alpha ranging from 5% to nearly 20% over multiple benchmarking cycles compared to public markets equivalents. Appetite is no longer in question; if anything, it’s stronger than ever.

Source: Ares Wealth Management Solutions

For investors used to liquidity on tap…mutual funds you can exit overnight, stocks you can sell in seconds, savings apps that move money with a swipe, the long lockups of private markets feel like another world. A decade may pass easily for a global pension fund. For an Indian HNI, it feels more like a test of conviction: a structure that demands trust, patience, and a different rhythm than what they see in the public markets.

And to be clear, this isn’t about naïve impatience. LPs today are far smarter and more deliberate than a decade ago. Funding winters have sharpened perspectives, and conversations today are far more sophisticated. The sharper questions aren’t why private markets, but how. How soon to liquidity? How much visibility along the way? Can capital be recycled without losing exposure? These signal a maturing market with participation not just deeper, but more discerning.

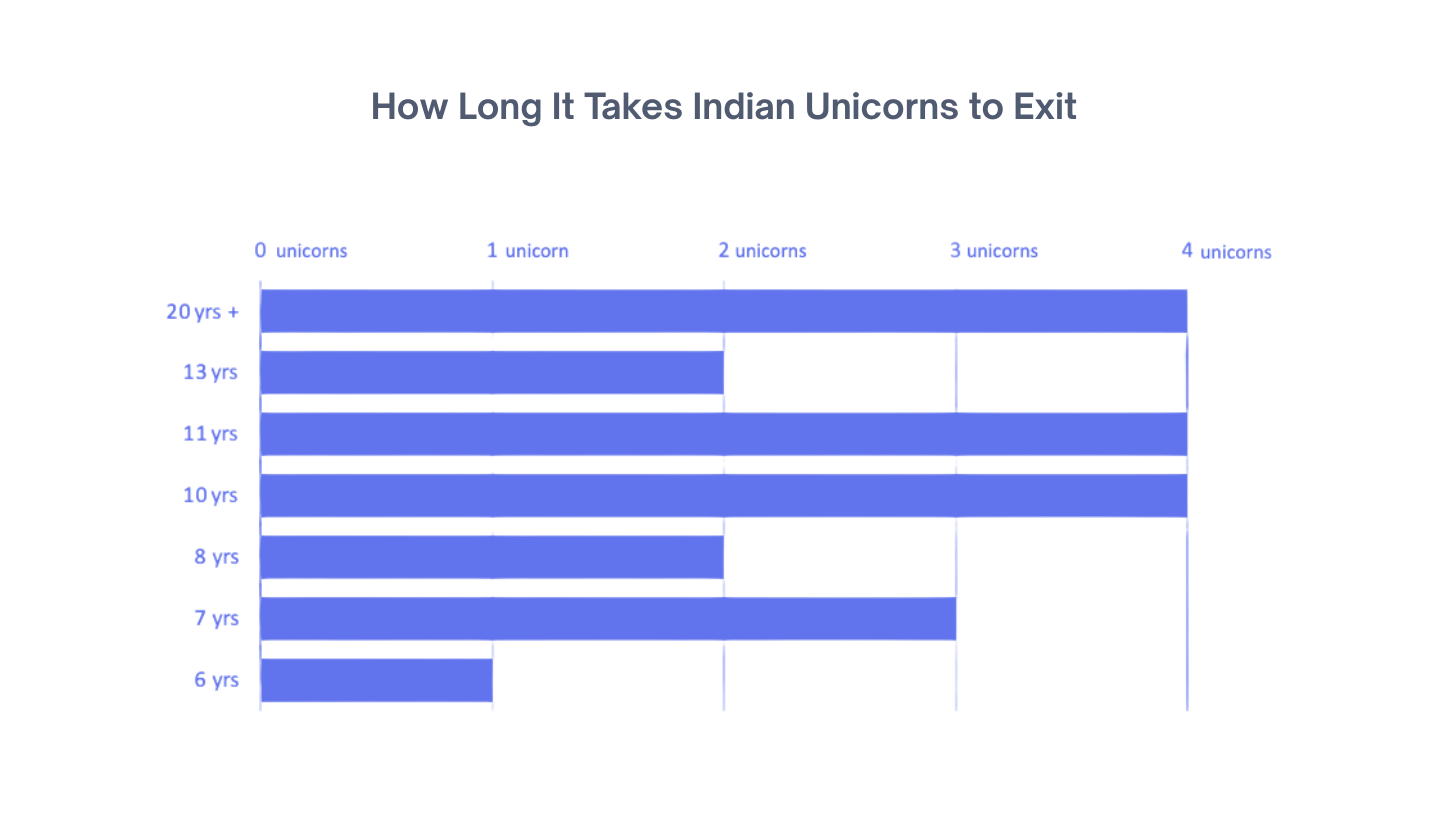

That scrutiny is right on cue. The very nature of timelines has shifted. Across the globe, the traditional 10+2 year VC/PE model is under pressure. The average holding period for buyouts in the US and Canada spiked to 7.1 years in 2023, the longest in over two decades. As per SVB’s State of the Markets H1 2025 report, top-quartile funds now often take 16–20 years to fully return capital. Unicorns like Zomato, Nykaa, and Paytm went public 9–13 years after founding. High IPO activity that we have witnessed in India recently doesn’t mean shorter timelines; companies are still taking longer to scale before they list, as they should.

Source: PrivateCircle Research

Seen in this light, extended holds aren’t failures, but rather deliberate execution taking cycles of evolution. Building global-scale companies takes time. Top Indian funds often hold flagship assets 8–10 years before seeking liquidity. Exits are scrutinised more, DPI valued above paper mark-ups, and managers are building with more rigor. For an economy like ours, that discipline is healthy.

But discipline alone isn’t enough. Patience, on its own, eventually runs into limits. And this is where the real unlock lies.

Innovation has become the hero, doing what patience alone could not: bringing more people comfortably into the fold. And at the center of that innovation is one structure above all: secondaries.

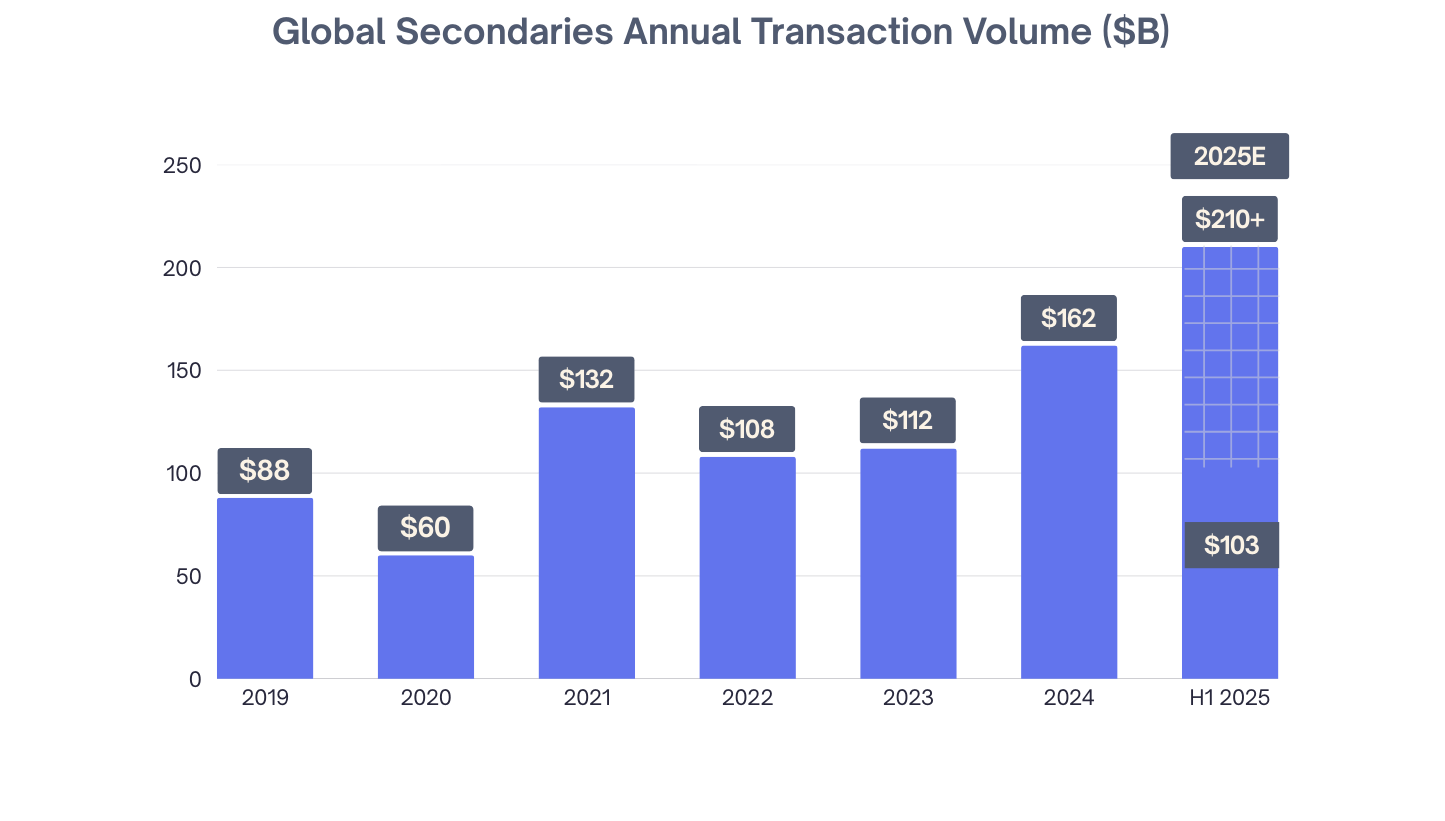

Secondaries aren’t new. Decades ago, they were little more than an escape hatch for an LP who couldn’t wait out a cycle and was looking to sell to someone who could. What’s innovative today is their reinvention. From distressed trades on the margins, they’ve become front-line tools of portfolio strategy: deliberately structured, GP-led, and scaled into a $160 billion global market. That reinvention is innovation. Secondaries no longer just transfer ownership; they reshape the rhythm of patience in private markets.

In 2024, global secondary volumes jumped 45% to $162 billion. The first half of 2025 has already crossed $103 billion. The real shift isn’t just in size but in shape: GP-led deals, once rare, now make up nearly half the market. Managers themselves are using secondaries to hold their best companies longer, while still giving LPs the option of liquidity.

Source: Jefferies H1 2025 Global Secondary Market Review

Continuation funds share the same logic. First conceived to extend the life of strong assets when the clock ran out, they’re now part of the mainstream playbook, sometimes even extending into “continuations of continuations.”

India is firmly part of this evolution. Annual secondary deal activity here is projected around $20 billion. In the first half of 2024, more than a third of $50–500 million transactions were secondaries, which was unthinkable just a few years ago. Liquidity is clearly not just an afterthought anymore.

The number of players has grown sharply. Just last month, IVCA hosted a full-day conference on secondaries, and the turnout was proof of how quickly depth is forming. What was once niche is becoming mainstream, with both domestic and global houses putting serious weight behind the market. At Oister, secondaries remain a core, though not the only, strategy, and the momentum around us makes it clear: India is building real depth in this space.

For Indian HNIs and family offices, this shift is significant. But while secondaries bring enormous power, they aren’t without their gaps. For them to truly fulfil their promise, investors need visibility. The real innovation lies in going well beyond the sparse disclosures of a new fund, including naming companies, sharing performance, and mapping growth trajectories upfront. At Oister, that’s something we’ve been working toward in our own funds, and we’ve seen how much more confidence investors have when they can see what they’re stepping into. Over time, this kind of transparency will become as valuable as the liquidity secondaries provide and it’s what will draw more domestic investors into private markets.

The effect goes beyond investors. When LPs get liquidity, GPs can show DPI earlier, and founders see fresh capital flow in, the entire ecosystem gains confidence.

Porter’s recent round underscored how secondaries let early investors exit cleanly and make room for the next set of backers without slowing the company’s trajectory. Last year’s secondary transactions in Swiggy ahead of its IPO showed a different use case: long-held stakes changing hands to lock in decade-old gains, while new investors step in with conviction and large shareholders adjust positions for regulatory reasons. Together, these deals underscore that secondaries are instruments of liquidity, price discovery, and capital circulation that keep companies moving forward.

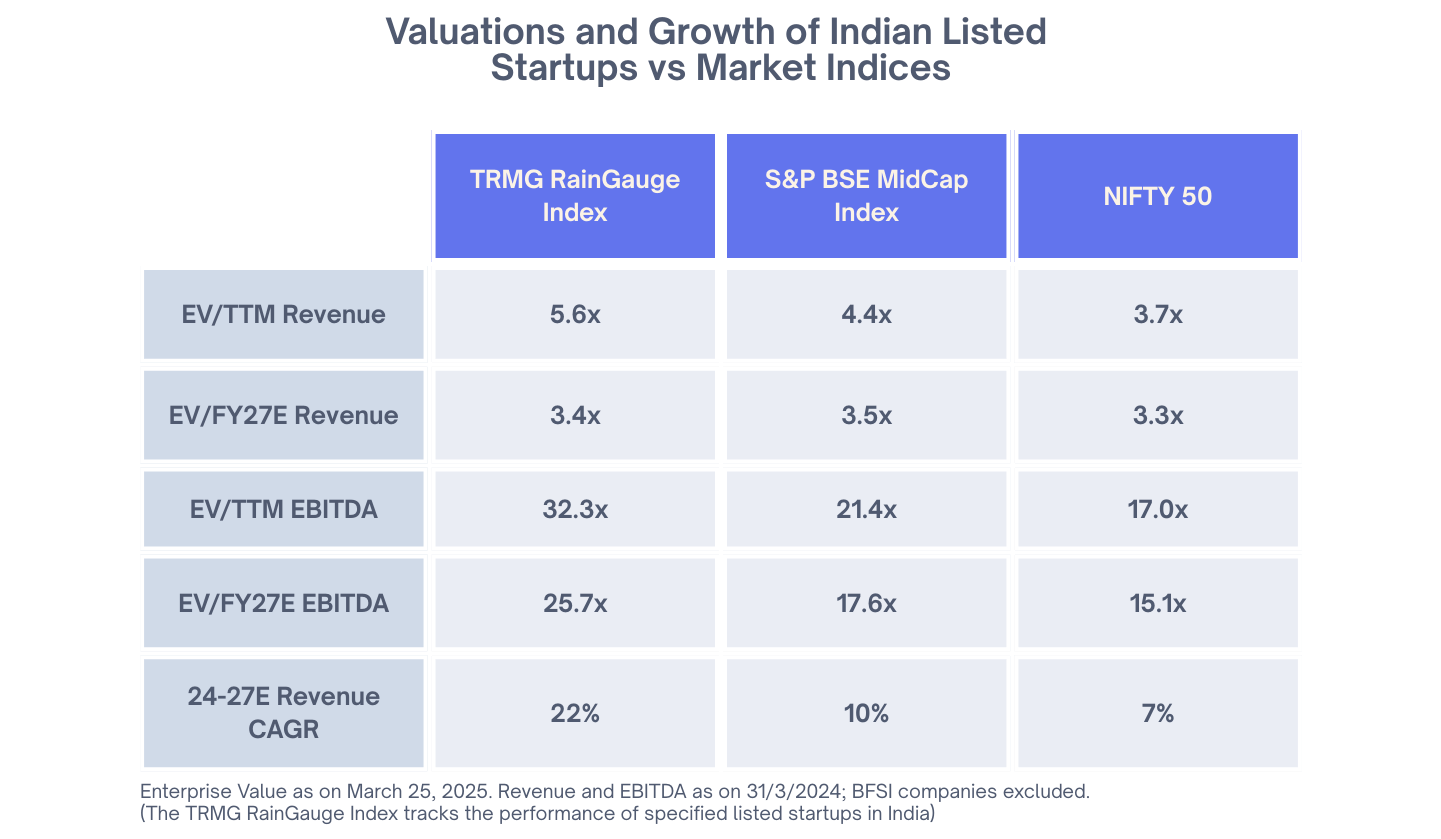

Part of why secondary activity is surging in India is that these are also conviction trades. The fundamentals of India’s new economy companies are solid. Even in public markets, listed startups command premium multiples, backed by higher revenue growth than mid-cap peers and large caps. These are businesses scaling faster, with deeper moats, which is why capital is flowing into them through both primary and secondary rounds.

Source: TRMG RainGauge Index Report Q3FY25

Let’s pause on that. India’s leading startups are proving their fundamentals, and secondaries have become a way for investors to access them early, long before they hit public markets. These deals offer liquidity for some and opportunity for others, but more importantly, they bring visibility: what’s being held, how it’s compounding, and when liquidity windows may open. When investors can see the journey, they’re far more willing to stay on it.

In the end, patience will always be the cornerstone. Good businesses don’t get built in quarters; they take years of compounding, pivots, and steady hands.

The scale of what’s possible is clear. In the US, private equity contributed nearly $2 trillion to GDP in 2024, making up ~7% of the total US GDP. India’s private markets likely account for only 1–2% of its GDP today. Yet even a modest step-change to 5–6% over the next decade would mean billions in patient capital funding jobs, infrastructure, and innovation before public markets ever touch them. It would also signal a cultural shift: domestic wealth behaving less like restless cash and more like long-term capital.

For that to happen, we’ll need both discipline and imagination. Discipline, to let time do its work. Imagination, to keep innovating with structures that give investors the visibility and trust they need. That’s how domestic capital will step in with conviction, and why the ecosystem will flourish stronger than ever. In the end, this market will be defined not by speed, but by staying power.

And in private markets, as in life, all good things still come to those who wait.

Thank you and see you in October.

TERMS OF USE

Thank you for your interest in our Website at https://unlistedintel.com/. Your use of this Website, including the content, materials and information available on or through this Website (together, the “Materials”), is governed by these Terms of Use (these “Terms”). By using this Website, you acknowledge that you have read and agree to these Terms.

NO OFFER, SOLICITATION OR ADVICE

Our site is provided for informational purposes only. It does not constitute to constitute (i) an offer, or solicitation of an offer, to

purchase or sell any security, other assets, or service, (ii) investment, legal, business, or tax advice, or an offer to provide such advice or (iii) a basis for making any investment decision.

The Materials are provided for informational purposes and have been prepared by Oister Global for informational purposes to acquaint existing and prospective underlying funds, entrepreneurs, and other company founders with Oister Global's recent and historical investment activities.

Please note that any investments or portfolio companies referenced in the Materials are illustrative and do not reflect the performance of any Oister Global fund as a whole. There is no obligation for Oister Global to update or alter any forward-looking statements, whether as a result of new information, future events, or otherwise.

PURPOSE LIMITATION AND ACCESS TO YOUR PERSONAL DATA:

We will only collect your personal data in a fair, lawful, and transparent manner. We will keep your personal data accurate and up to date. We will process your personal data in line with your legal rights. We use your name and contact details, such as email, postal address, and contact number to continue communications with you. We may also use your contact information to invite you to events we are hosting or to keep you updated with our news.

USE OF COOKIES OR SIMILAR DEVICES

We use cookies on our website. This helps us to provide you with a better experience when you browse our website and also allows us to make improvements to our site. You may be able to change the preferences on your browser or device to prevent or limit your device’s acceptance of cookies, but this may prevent you from taking advantage of some of our features.

MATERIAL

The material displayed on our site is provided “as is”, without any guarantees, conditions, or warranties as to its accuracy, completeness, or reliability. You should be aware that a significant portion of the Materials includes or consists of information that has been provided by third parties and has not been validated or verified by us. In connection with our investment activities, we often become subject to a variety of confidentiality obligations to funds, investors, portfolio companies, and other third parties. Any statements we make may be affected by those confidentiality obligations, with the result that we may be prohibited from making full disclosures.

MISCELLANEOUS

This Website is operated and controlled by Oister Global in India. We may change the content on our site at any time. If the need arises, we may suspend access to our site, or close it indefinitely. We are under no obligation to update any material on our site.

CONTACT INFORMATION

Any questions, concerns or complaints regarding these Terms should be sent to info@oisterglobal.com