Private markets have always required patience. But what’s changed is how capital allocators, especially those closer to wealth creation, are beginning to frame that patience not as a trade-off, but as a design choice.

As the Indian private capital landscape matures, investors are no longer asking just what the return could be, but how the return is shaped. And that answer, increasingly, has to do with liquidity, when you can access it, how predictable it is, and what you give up in order to reach for a different kind of outcome.

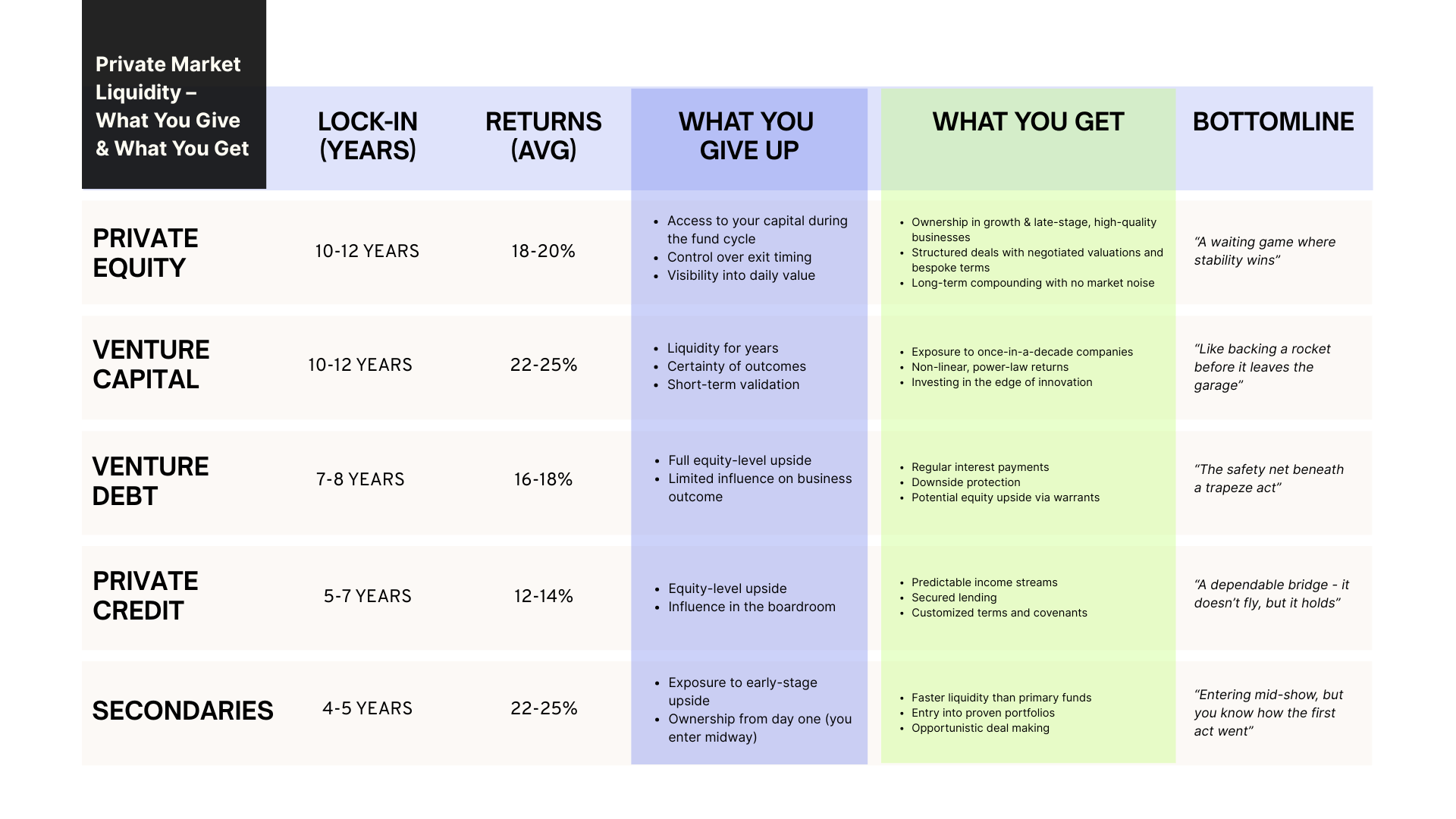

At the longest end of the spectrum sit private equity and venture capital. These are 10–12 year cycles. Once committed, the capital is locked, with no real access until a portfolio company exits. There is limited visibility into value along the way, and little control over exit timing. But in exchange, you enter early, participate fully, and benefit from attractive entry points. The outcomes are uneven, especially in venture, but the power-law dynamics are real. A few investments can drive the bulk of returns. These strategies are built around asymmetry.

This structure may feel rigid, but it mirrors the nonlinear nature of what it’s backing. The underlying high-growth companies need time, space, and patient capital to reach their maximum potential. For investors with long-term horizons and high-conviction theses, this model can deliver extraordinary outcomes. But it comes with a cost: long holding periods.

Credit strategies, private credit and venture debt, shift the equation. Here, investors give up equity-level upside, but receive income. Venture debt tends to sit alongside equity, but behaves more like a structured note, with interest payments, warrants, and downside protection. Private credit is more traditional: secured lending with predictable cash flows and negotiated covenants. Both carry lower return potential, but much higher visibility and predictability. They are cash-flow-based investments, increasingly used to bring stability into a private capital sleeve.

What makes credit strategies compelling in recent times is not just their yield, but their clarity. In an environment of slower distributions and macro volatility, investors are placing a premium on cash flows they can model. Private credit has emerged as the ballast in many sophisticated portfolios.

Secondaries are different and increasingly relevant. These transactions allow investors to enter mid-cycle, often at more informed valuations, with shorter holding periods. The capital is still illiquid, but it’s tied to companies with established performance. The return potential remains strong, especially when the entry is opportunistic. What’s given up is early-stage upside. But what’s gained is clarity. This is where many wealth owners who want private market exposure but not the full illiquidity curve are starting to enter.

Secondaries also introduce another dimension: optionality. Investors can deploy capital more tactically, entering vintage years or sectors that align with their broader views, without committing to a blind pool. With the rise of GP-led transactions and continuation funds, secondaries now offer curated exposure to high-conviction assets, managed by teams with proven track records.

The structure of each of these strategies reflects a different philosophy of return. Venture capital trades liquidity for the chance to back something non-linear. Private credit does the opposite; it caps the return, but offers certainty. Secondaries meet in the middle, enough upside to matter, enough visibility to stay committed.

They are long-hold, high-friction positions, and they test not just appetite, but temperament. Liquidity is not free. But in private markets, neither is access.

And what sits in between patience, structure, and clarity is increasingly where the design conversation is shifting.

In public markets, liquidity is assumed. In private markets, it’s engineered. And every layer of liquidity, or its absence, comes with trade-offs.

The real question for allocators isn’t “which private market asset class is better?” but “which matches my mandate, horizon, and tolerance?” Each strategy is a different response to the same challenge: how to convert capital into long-term value under varying levels of control and visibility.

Bottom line: The wait time could be long but if the bet pays off, the curve bends upward sharply. Compounding with silence and scale.

Bottom line: A high-conviction game of outliers. You don’t need many wins, just a few that change the shape of your portfolio. Expect noise, be patient for power laws.

Bottom line: You lend into growing companies with warrant optionality. The upside is modest, the protection is built-in. A yield play with downside protection.

Bottom line: Predictability over potential. Regular income, senior rights, negotiated terms. Returns don’t swing, they accrue.

Bottom line: You miss Act 1, but step in with a script. It’s about pacing, price, and clarity. May not give you an edge in being early, but you benefit from knowing what you’re entering.

In many ways, the growing seriousness around private markets reflects something broader, a recalibration in how capital wants to behave.

For a long time, illiquidity was a deterrent. Now, it’s understood as a design choice. Investors are increasingly willing to lock up capital not out of compulsion, but out of alignment. They’re choosing structure, intention, and clarity of role.

What was once seen as “alternative” is being absorbed into the core of how sophisticated portfolios are built. Private market investing is about being part of capital journeys that public markets don’t always allow. About owning exposure where value isn’t constantly repriced by sentiment. And about recognising that patience, when paired with good underwriting, has its own return curve.

That doesn’t mean every investor is ready for every strategy. Venture capital tests conviction. Private equity requires time. Credit demands comfort with caps. Secondaries trade early risk for mid-cycle clarity. Each comes with its own contract, written as much in an investor’s temperament as in numbers.

But what unites them is this: the understanding that some things grow better when they aren’t pulled at every quarter. That value, in many cases, is created over time, in boardrooms and factories, in codebases and warehouses, long before a headline.

Private markets are becoming more deliberate, more accessible, and more aligned with how serious capital thinks.

TERMS OF USE

Thank you for your interest in our Website at https://unlistedintel.com/. Your use of this Website, including the content, materials and information available on or through this Website (together, the “Materials”), is governed by these Terms of Use (these “Terms”). By using this Website, you acknowledge that you have read and agree to these Terms.

NO OFFER, SOLICITATION OR ADVICE

Our site is provided for informational purposes only. It does not constitute to constitute (i) an offer, or solicitation of an offer, to

purchase or sell any security, other assets, or service, (ii) investment, legal, business, or tax advice, or an offer to provide such advice or (iii) a basis for making any investment decision.

The Materials are provided for informational purposes and have been prepared by Oister Global for informational purposes to acquaint existing and prospective underlying funds, entrepreneurs, and other company founders with Oister Global's recent and historical investment activities.

Please note that any investments or portfolio companies referenced in the Materials are illustrative and do not reflect the performance of any Oister Global fund as a whole. There is no obligation for Oister Global to update or alter any forward-looking statements, whether as a result of new information, future events, or otherwise.

PURPOSE LIMITATION AND ACCESS TO YOUR PERSONAL DATA:

We will only collect your personal data in a fair, lawful, and transparent manner. We will keep your personal data accurate and up to date. We will process your personal data in line with your legal rights. We use your name and contact details, such as email, postal address, and contact number to continue communications with you. We may also use your contact information to invite you to events we are hosting or to keep you updated with our news.

USE OF COOKIES OR SIMILAR DEVICES

We use cookies on our website. This helps us to provide you with a better experience when you browse our website and also allows us to make improvements to our site. You may be able to change the preferences on your browser or device to prevent or limit your device’s acceptance of cookies, but this may prevent you from taking advantage of some of our features.

MATERIAL

The material displayed on our site is provided “as is”, without any guarantees, conditions, or warranties as to its accuracy, completeness, or reliability. You should be aware that a significant portion of the Materials includes or consists of information that has been provided by third parties and has not been validated or verified by us. In connection with our investment activities, we often become subject to a variety of confidentiality obligations to funds, investors, portfolio companies, and other third parties. Any statements we make may be affected by those confidentiality obligations, with the result that we may be prohibited from making full disclosures.

MISCELLANEOUS

This Website is operated and controlled by Oister Global in India. We may change the content on our site at any time. If the need arises, we may suspend access to our site, or close it indefinitely. We are under no obligation to update any material on our site.

CONTACT INFORMATION

Any questions, concerns or complaints regarding these Terms should be sent to info@oisterglobal.com