[TL;DR]

The legacy venture capital playbook in India has long been linear: raise primary capital, dilute equity, fund hyper-growth, seek a public listing, distribute returns. For two decades, that sequencing worked well enough. It no longer does.

As India’s technology and consumption ecosystems mature, the region’s most sophisticated market participants are executing a fundamentally different strategy. Companies like Lenskart, FirstCry, Swiggy, and Zepto are demonstrating that the run-up to a mega-IPO is no longer just about capital accumulation — it is an exercise in ownership architecture. When a private company achieves structural scale and robust unit economics, raising massive primary capital becomes counterproductive and dilutive. The smarter move is to use the private secondary market to orchestrate multi-million-dollar equity transitions where shares change hands entirely between existing backers and incoming institutional players, without a single rupee entering the company’s operational balance sheet.

India’s private secondary market has crossed a structural threshold. It has transformed from a fragmented, ad-hoc liquidity venue into a core capital market layer — operating with its own price discovery mechanisms, valuation frameworks, and institutional buyer ecosystems entirely separate from the mainboard.

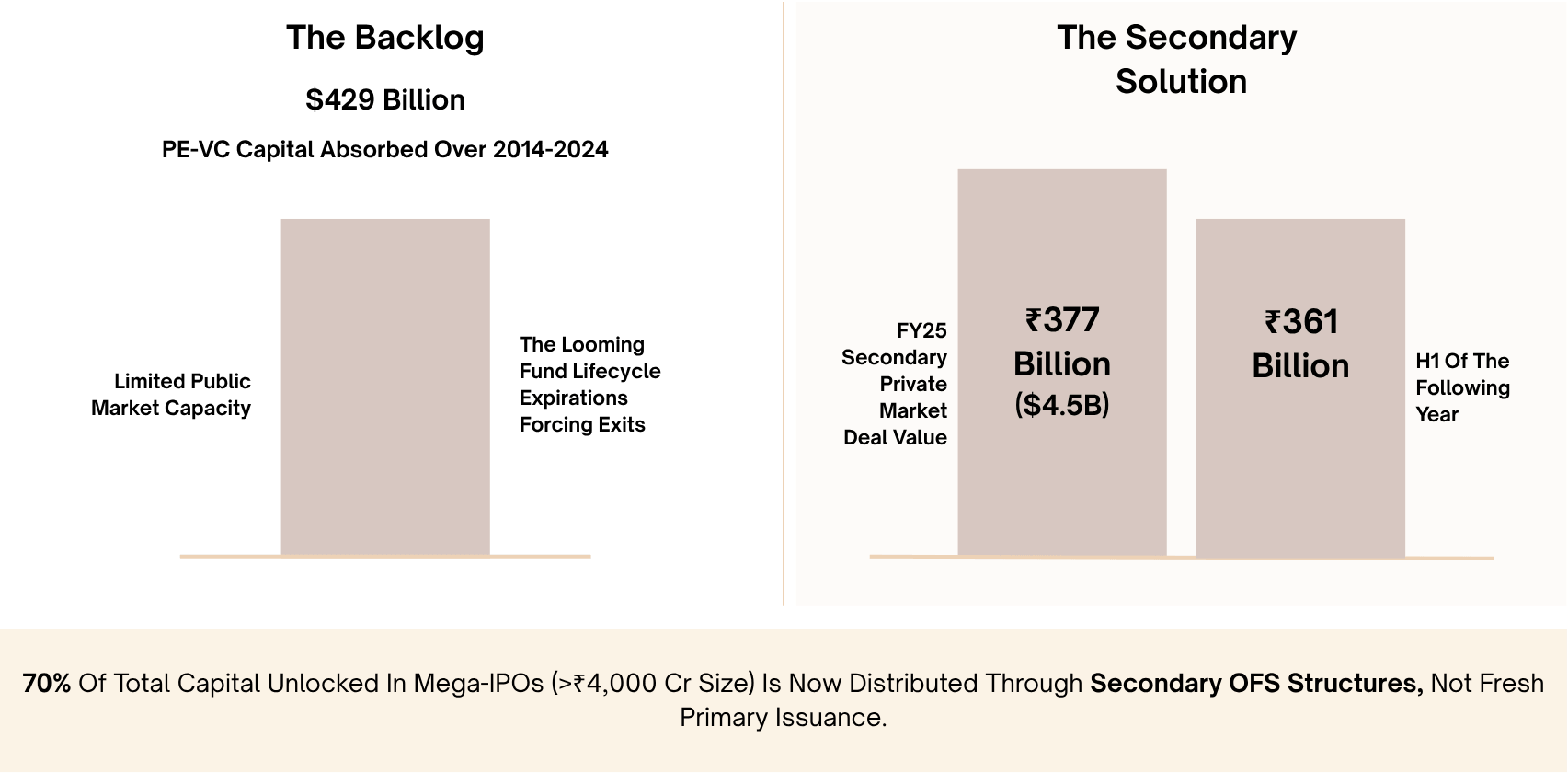

The structural reason is straightforward. Over the decade ending 2024, India’s PE-VC ecosystem deployed $429 billion across thousands of companies. With billions of this vintage now crossing the decade mark, fund lifecycles are forcing exits regardless of whether public markets are receptive. The supply-demand mismatch between assets seeking liquidity and available mainboard capacity has created an institutional-grade private asset class that now processes billions of dollars in transactions quarterly.

The most important signal embedded in recent data: public markets are increasingly being utilised as final capitalisation tables, not growth-funding engines. Up to 70% of capital unlocked during India’s mega-listings flows through secondary OFS structures to exiting shareholders rather than into company balance sheets. The IPO is the closing ceremony of a multi-year secondary strategy — not the opening act of a new growth chapter. The actual institutional matching occurs privately, months before the listing bell rings.

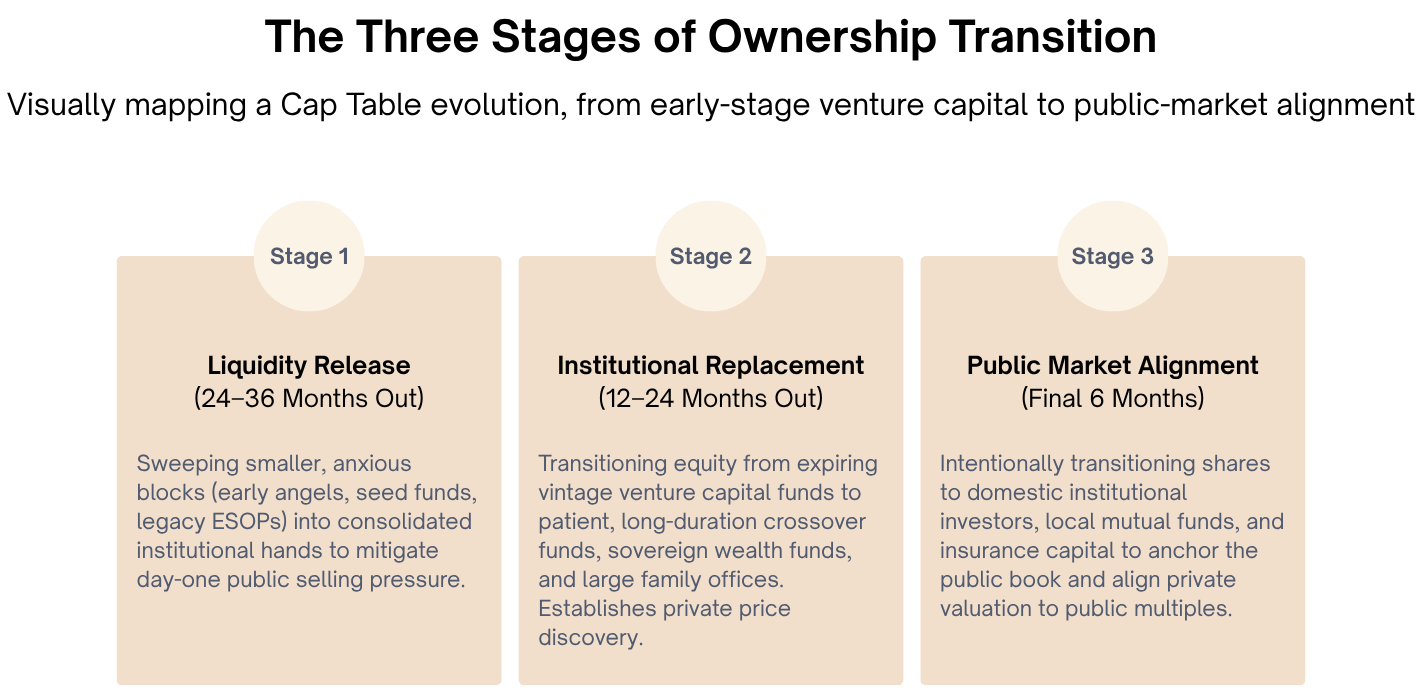

Understanding how the most sophisticated pre-IPO strategies operate requires viewing individual transactions through a unified framework of institutional ownership transition. Private market secondaries are the operational bridge connecting early-stage venture capital to the public mainboard through three distinct stages.

Stage 1 — Liquidity Release (24–36 months out): Issuers absorb shares from early angels, seed funds, and legacy ESOPs. Sweeping these smaller, anxious blocks into consolidated institutional hands mitigates day-one public selling pressure before it can form. This is structural housekeeping — clearing the long tail of early backers whose investment theses have been validated but whose continued presence on the cap table creates listing complexity.

Stage 2 — Institutional Replacement (12–24 months out): The cap table transitions from vintage venture capital funds — whose fund lifecycles mandate exits — to patient, long-duration global crossover funds, sovereign wealth funds, and large family offices. This stage establishes institutional price discovery entirely within the private domain, setting a valuation anchor that the public listing will reference.

Stage 3 — Public Market Alignment (final 6 months): Shares are intentionally transitioned to domestic institutional investors, local mutual funds, and insurance capital. This builds a local investor base that anchors the public book, aligns private valuation to public market multiples, and ensures stable opening day dynamics on the mainboard.

| Company | Estimated/Actual IPO Size | OFS Component / Share | Core Secondary Strategy |

|---|---|---|---|

| Lenskart | $5B valuation | ₹5,313 crore block | Stage 3 via Temasek / Fidelity $200M round |

| FirstCry | ₹4,193 crore | 60.2% (₹2,527 crore) | SoftBank sold to domestic family offices pre-IPO |

| Swiggy | ₹11,327 crore | ~60% (₹6,828 crore) | Private price discovery at $9.3–9.6B before listing |

| Zepto | ~₹11,000–12,000 crore (Est.) | 11.35 crore shares | ₹8,010Cr fresh issue; Nexus holds 77.5% of OFS pool |

Lenskart is the gold standard for Stage 3 alignment. By generating steady internal cash flows, it focused its capital architecture entirely on ownership optimisation rather than primary fundraising. A $200M Temasek/Fidelity secondary round transitioned equity to public-market-ready institutions, and the clean post-lock-in block deal execution of ₹5,313 crore at ₹473.4 per share validated the architecture’s precision.

Swiggy executed one of the most sophisticated Stage 2 price discovery exercises in Indian venture history. In the 90 days before filing, it opened targeted secondary blocks to HNIs and wealth managers at ₹350 per share — implying a $9.3–9.6B valuation — a calculated 20% discount to its $12B+ target listing price. This built concentrated domestic demand well before formal book-building began. The result: an OFS component of ₹6,828 crore representing roughly 60% of the entire ₹11,327 crore issue.

Zepto is the most technically precise execution of this framework yet. Filed under SEBI Regulation 6(2) — the pathway for pre-profit high-growth companies — its June 2026 UDRHP structures an ₹8,010 crore fresh issue alongside an 11.35 crore share OFS block designed explicitly as an exit vehicle for early international venture capital. Nexus Venture Partners holds 77.5% of the secondary supply pool, offering up to 87.97 million shares. The defining detail: Zepto’s founders are completely sitting out of the OFS, retaining 100% of their equity exposure post-listing. In the language of private markets, a founder who does not sell into the IPO is making the strongest possible statement about where they believe value creation is still ahead.

The National Stock Exchange represents a category entirely its own — permanent secondary liquidity without an exchange listing. Because of prolonged regulatory intervals holding up its official public float, NSE generates massive operational cash flows from domestic trading volumes without needing a single rupee of primary capital. Yet institutional blocks, private equity firms, and corporate treasuries routinely clear trades in closed private institutional secondary networks, driving its unlisted market capitalisation past ₹5 Lakh Crore.

NSE is absolute proof that when an asset is sufficiently profitable and backed by rigid corporate governance, a formal IPO is not the only pathway to continuous price discovery and liquidity. It is the secondary market’s most extreme validation case.

TERMS OF USE

Thank you for your interest in our Website at https://unlistedintel.com/. Your use of this Website, including the content, materials and information available on or through this Website (together, the “Materials”), is governed by these Terms of Use (these “Terms”). By using this Website, you acknowledge that you have read and agree to these Terms.

NO OFFER, SOLICITATION OR ADVICE

Our site is provided for informational purposes only. It does not constitute to constitute (i) an offer, or solicitation of an offer, to

purchase or sell any security, other assets, or service, (ii) investment, legal, business, or tax advice, or an offer to provide such advice or (iii) a basis for making any investment decision.

The Materials are provided for informational purposes and have been prepared by Oister Global for informational purposes to acquaint existing and prospective underlying funds, entrepreneurs, and other company founders with Oister Global's recent and historical investment activities.

Please note that any investments or portfolio companies referenced in the Materials are illustrative and do not reflect the performance of any Oister Global fund as a whole. There is no obligation for Oister Global to update or alter any forward-looking statements, whether as a result of new information, future events, or otherwise.

PURPOSE LIMITATION AND ACCESS TO YOUR PERSONAL DATA:

We will only collect your personal data in a fair, lawful, and transparent manner. We will keep your personal data accurate and up to date. We will process your personal data in line with your legal rights. We use your name and contact details, such as email, postal address, and contact number to continue communications with you. We may also use your contact information to invite you to events we are hosting or to keep you updated with our news.

USE OF COOKIES OR SIMILAR DEVICES

We use cookies on our website. This helps us to provide you with a better experience when you browse our website and also allows us to make improvements to our site. You may be able to change the preferences on your browser or device to prevent or limit your device’s acceptance of cookies, but this may prevent you from taking advantage of some of our features.

MATERIAL

The material displayed on our site is provided “as is”, without any guarantees, conditions, or warranties as to its accuracy, completeness, or reliability. You should be aware that a significant portion of the Materials includes or consists of information that has been provided by third parties and has not been validated or verified by us. In connection with our investment activities, we often become subject to a variety of confidentiality obligations to funds, investors, portfolio companies, and other third parties. Any statements we make may be affected by those confidentiality obligations, with the result that we may be prohibited from making full disclosures.

MISCELLANEOUS

This Website is operated and controlled by Oister Global in India. We may change the content on our site at any time. If the need arises, we may suspend access to our site, or close it indefinitely. We are under no obligation to update any material on our site.

CONTACT INFORMATION

Any questions, concerns or complaints regarding these Terms should be sent to info@oisterglobal.com