We all know the drill.

Stay the course. Good assets recover. Volatility, in time, fades into entry points.

But the more interesting question is how far that logic travels?

Periods of uncertainty tend to produce two things at once: more noise, and a greater need for perspective. Public markets usually offer plenty of both.

Investments are visible as they happen, recoveries can be tracked just as quickly, and over time these cycles have built a familiar playbook for how stressed periods tend to shape returns. They often create better entry points into strong assets. There is enough evidence behind it that the conviction feels earned.

Now, if staying the course is such a well-understood idea in public markets, how does that same idea actually play out in private markets?

For readers of Unlisted Intel, many contours of this will already be familiar. Fundamentally, the logic is the same. What differs in private markets is the way periods of stress are felt and expressed.

Private markets do not lack information, but the nature of the asset class means that information is more dispersed, less immediate, and less broadly circulated. That can make periods of stress harder to interpret from the outside, even when the underlying dynamics are fairly straightforward.

So here is how the pattern usually unfolds in private markets.

Liquidity becomes more valuable. The gap between investors who need to transact and those who can afford to wait starts to widen. As that happens, opportunity is shaped less by valuation alone and more by access, negotiation, and patience.

Such periods of dislocation are often fertile for disciplined capital. Illiquidity, uncertainty, and complexity tend to reduce competition, but they also create room for stronger underwriting, better structuring, and more selective entry. Over time, those advantages can translate into more than resilience. In private markets, that is often when better opportunities begin to emerge. They can create additional alpha.

Source: Moonfare

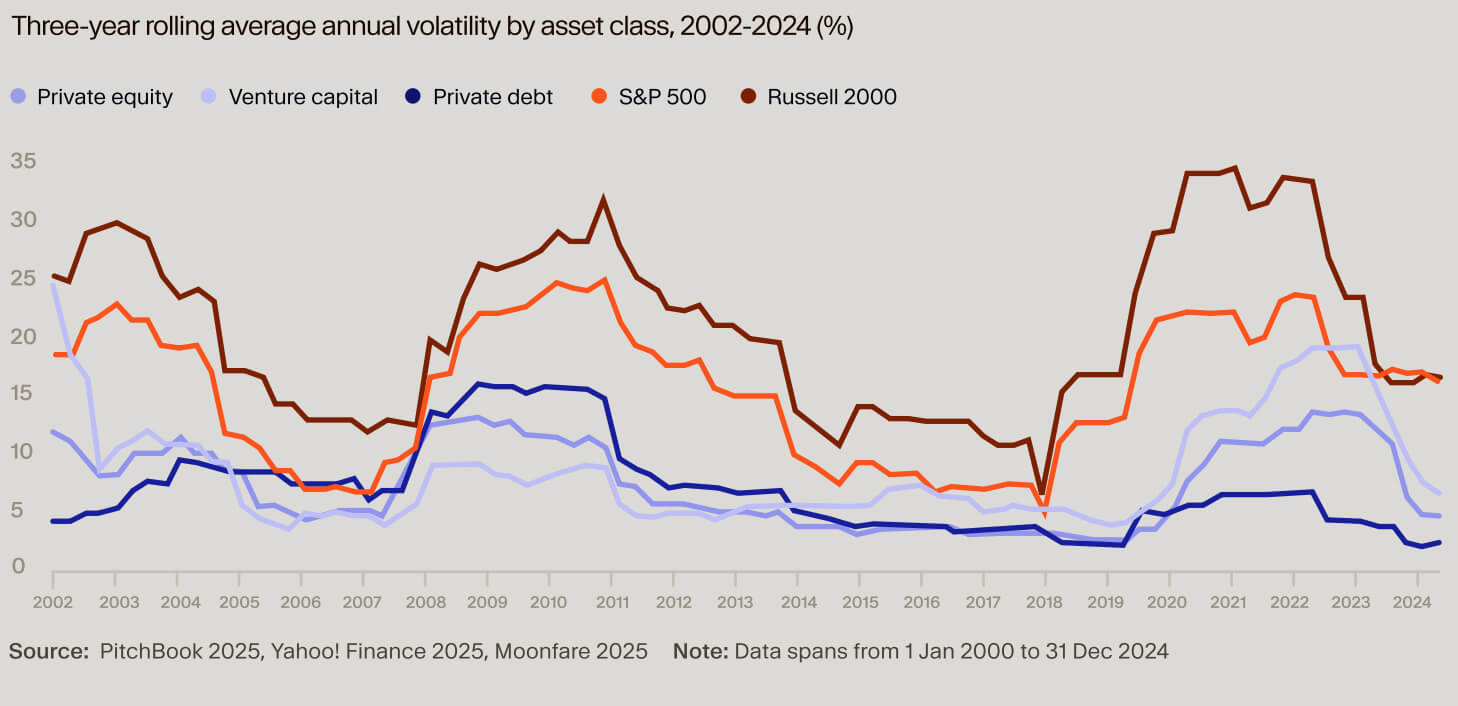

Public markets absorb fear immediately. Private markets register it more slowly, through exits, liquidity, financing conditions, and valuation resets. This is what creates room for disciplined capital to act. The vintage data makes that point clearly. Some of the strongest outcomes have come from the years investors found hardest to commit to.

The current moment is uncomfortable by any measure. But discomfort has a track record in private markets. It tends to age well.

To take that question further, we went back through the major shocks of the last two decades and looked at what stress actually did inside private markets. That feels like a more useful way to think about what staying the course means from here.

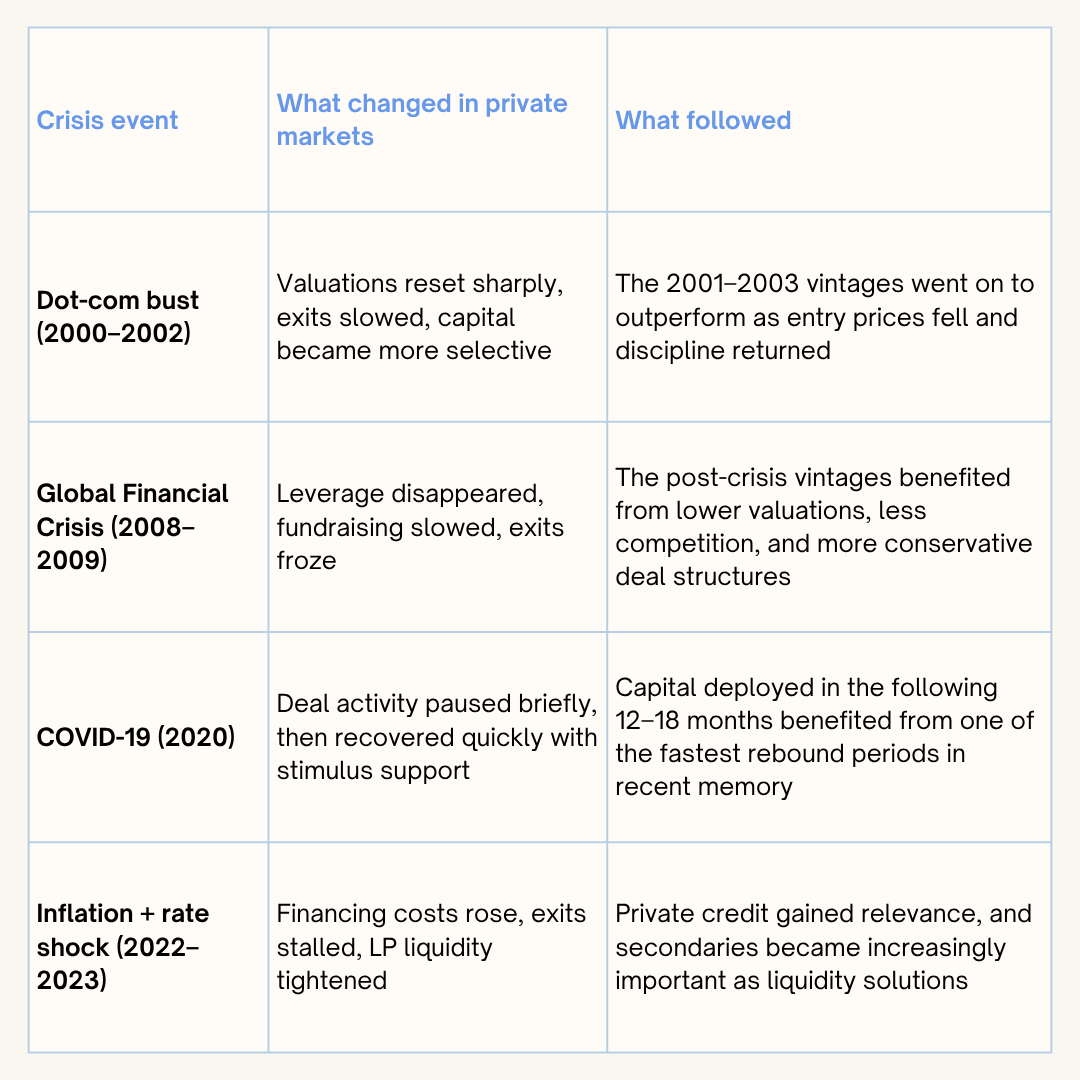

A Brief History of Stress: How Private Markets Actually Behaved

McKinsey’s latest work with IVCA on LP sentiment makes this visible in real time. India still screens as highly attractive, with 31% of surveyed LPs ranking it as their top private-markets destination in Asia-Pacific and 76% placing it in their top three. But the report also shows that enthusiasm is no longer broad or unqualified. The most committed allocators are focused on deployment opportunities, risk-adjusted returns, and manager quality, while others are paying closer attention to exit records, governance, disclosures, and cost discipline.

That feels true more broadly. After repeated shocks, capital does not usually leave the system; it becomes more selective. In India, the six largest GPs took 64% of fundraising in 2022–24, up from 59% in 2016–18. In US ventures, 33% of all investment in 2025 went to the top 1% of companies by valuation. The pattern is clear enough: after volatility, investors stop rewarding the broad story and start rewarding evidence.

What makes this shift more relevant now is who the investor base increasingly is. Domestic capital, particularly family offices and HNIs now accounts for a meaningful and growing share of AIF commitments. For many of them, private markets are a deliberate part of portfolio construction in pursuit of higher, differentiated returns. As that capital deepens, the need to understand how private markets behave across cycles becomes more important. Not just where to allocate, but when, and with whom.

What Happened

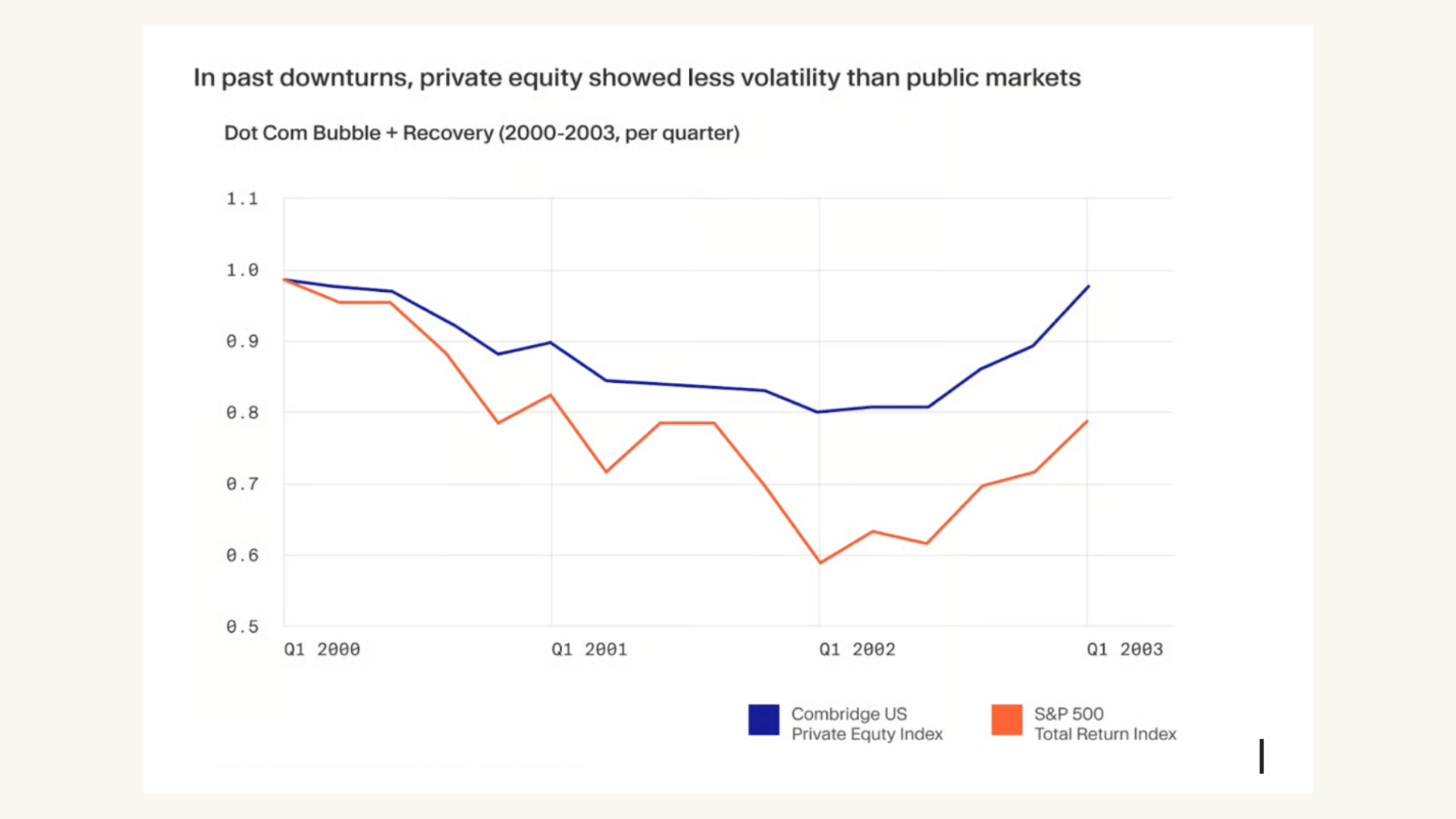

Through the late 1990s, abundant capital flooded into internet companies, many of them unprofitable. The NASDAQ peaked in March 2000 at 5,048, then lost 78% of its value by October 2002. The S&P 500 fell 49%. The “growth at any cost” era ended brutally, compounded by 9/11 in 2001.

What It Did to Private Markets

The venture market, which had funded much of the bubble, was hit hard. U.S. venture investment fell from $93.8 billion in 2000 to $34.6 billion in 2001, $19.4 billion in 2002, and $16.9 billion in 2003. Private equity proved more resilient in the years that followed. The 2001 private equity vintage went on to generate a 2.11x TVPI seven years into fund life, while the U.S. buyout market declined by less than 13% during the downturn, far less than public markets. Firms that kept deploying capital into undervalued businesses captured the best deals of the decade. Most didn’t, they froze, and missed the vintage of a generation.

The lesson: in private markets, the instinct to step back after a shock is understandable, but it is often the vintages raised and deployed in those periods that go on to be the strongest.

The vintage-year data suggests a familiar cycle in private markets: returns tend to be weaker for vintages raised at the top of a cycle and stronger for those deploying after valuations have reset. The 2001 vintage is a striking example.

The same pattern is visible at the index level. Private equity did not avoid the dot-com downturn, but it moved through it with far less visible volatility than public markets. It shows that public markets reprice immediately. Private markets absorb pressure more gradually, through slower valuation resets, tighter exits, and a more selective flow of capital.

TL;DR: The dot-com bust wiped out excess, especially in venture, but it also set up one of the strongest PE vintages in the years that followed. The lesson was clear: the periods that feel hardest to commit to often turn out to be the ones most worth staying invested through.

What Happened

Subprime mortgage stress cascaded into the worst financial crisis since the Great Depression. Lehman Brothers collapsed in September 2008, short-term funding markets were severely disrupted, and the S&P 500 fell 57% from its October 2007 peak to its March 2009 trough. Global output contracted in 2009 for the first time in the postwar period.

What It Did to Private Markets

The leveraged buyout market running at record volumes through 2006–07 stopped cold. The 2006 and 2007 vintages, loaded with highly leveraged deals at peak valuations, were badly exposed. Fundraising fell. Exits collapsed. LPs who needed liquidity had nowhere to go.

Firms that held their nerve told a different story. The 2008 vintage generated a 1.51x TVPI. McKinsey’s research across 120 of the largest PE firms explains the gap: firms with dedicated value-creation teams returned 23% net IRR during the crisis, five percentage points ahead of those without. More starkly, firms without operating teams saw fund sizes fall 82%. Those with them fell only 19%. The difference wasn’t just in returns. It was in survival.

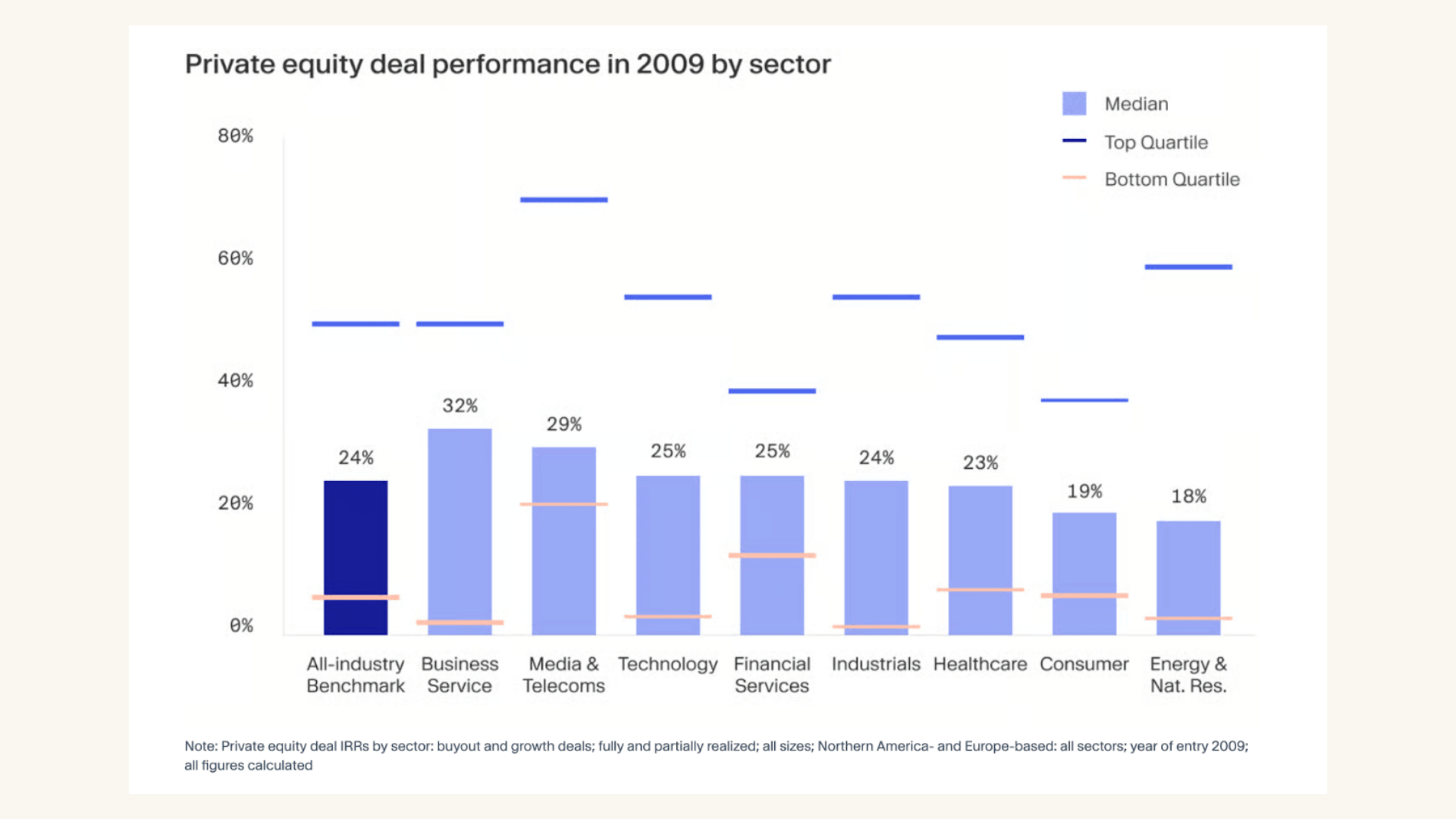

Sector-level data adds another layer to the story. Even in 2009, median deal-level returns were positive across most sectors, with especially strong outcomes in business services, media and telecom, technology, and financial services. The GFC was brutal for leverage-heavy deals struck at the top of the cycle, but once pricing reset, the opportunity set improved quickly for capital that was still willing to deploy.

The lesson: in a crisis, operational depth protects you on the way down. Conviction is what builds returns on the way back up.

TL;DR: The GFC froze private markets, but only for managers without the infrastructure to withstand it. Firms with operational depth and the discipline to keep deploying came out ahead. The 2008 vintage outperformed the two before it. As in 2001, the crisis itself wasn’t the problem. Being unprepared for it was.

What Happened

Just as the world was recovering from the GFC, Europe descended into a sovereign debt crisis. Greece, Portugal, Ireland, Spain, and Italy faced unsustainable borrowing costs. The euro itself came under existential threat. It took Mario Draghi’s now-famous pledge to do “whatever it takes” in July 2012 to finally stabilize markets, but not before two years of deep uncertainty had rattled European economies and investors alike.

What It Did to Private Markets

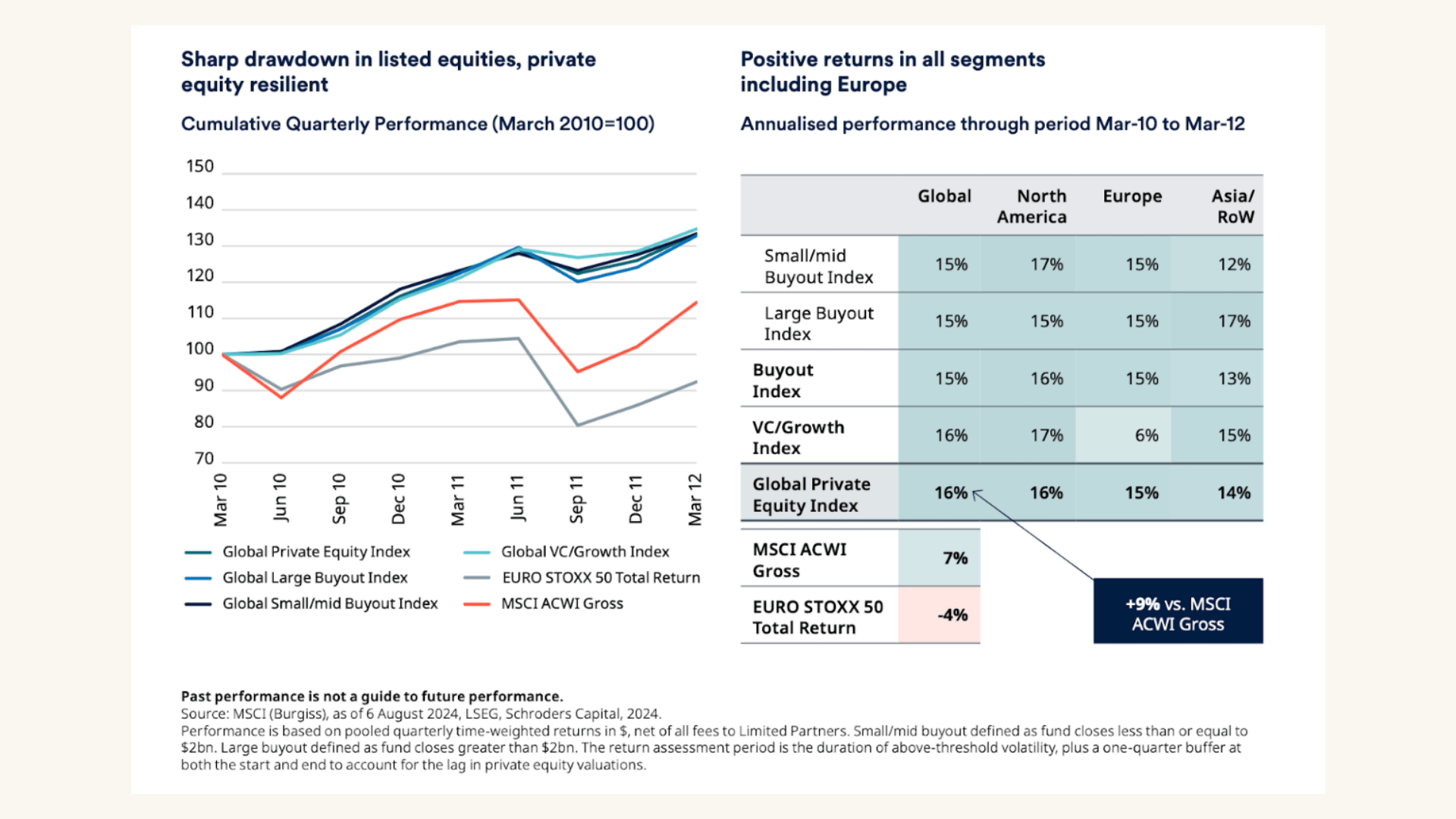

This crisis was more geographically contained than the GFC, but it still tightened financing conditions, widened risk spreads, and weakened the economic outlook across much of Europe. Yet private equity proved unusually resilient. From March 2010 to March 2012, global private equity returned 16% annualised, outperforming the MSCI ACWI Gross Index by 9 percentage points. Even more strikingly, European private equity delivered 15% annualised returns during a period in which the EURO STOXX 50 Total Return index fell 4%. Unlike most other crises in the past 25 years, this was one period in which private-equity performance held up consistently across strategies and regions, including Europe itself.

Public markets in Europe suffered a sharp drawdown, but private equity followed a different path. The takeaway is that private equity was still able to produce positive outcomes across segments even while public markets and sovereign credit were under severe pressure.

Hamilton Lane’s longer-horizon view of European private equity reaches a similar conclusion: the region has continued to justify its place as a core private-markets exposure, even through inflation, rate rises, war on European soil, and the aftereffects of Brexit.

The lesson: the Eurozone crisis showed that private-market resilience is not always about avoiding stress. Sometimes it is about preserving enough stability for capital to keep compounding while public markets remain trapped in volatility.

TL;DR: The Eurozone crisis hit European PE deal flow hard but private markets still outperformed public markets through the worst of it. The managers who stayed in Europe emerged stronger than those who pulled back.

What Happened

The COVID shock produced the fastest bear market in history. The S&P 500 fell 34% in 33 days as lockdowns brought large parts of the global economy to a sudden stop. Entire sectors such as travel, hospitality, live events, and offline retail saw revenues collapse almost overnight. Governments responded with extraordinary fiscal and monetary stimulus, and by August 2020, markets had returned to record highs.

What It Did to Private Markets

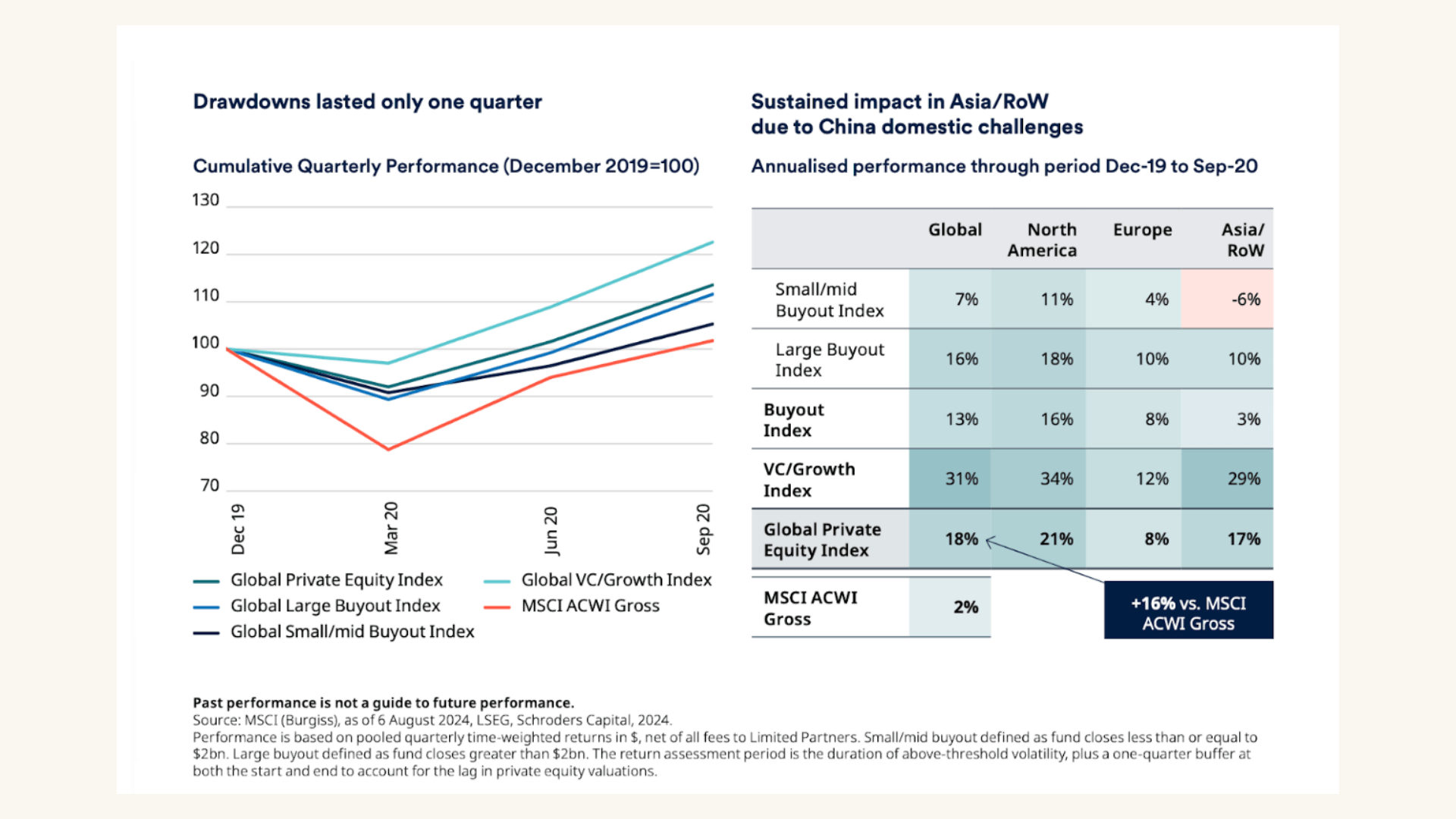

The initial shock to private markets was real. Deal activity paused abruptly in the second quarter of 2020 as firms turned inward, focused on portfolio support, liquidity preservation, and operational triage. Bain’s review of the year describes private equity as taking a sharp second-quarter hit before recovering with surprising speed as 2020 progressed.

The chart captures why this cycle looked so different from earlier crises. The drawdown in private equity lasted only one quarter, and from December 2019 to September 2020 the Global Private Equity Index returned 18% annualised, versus 2% for MSCI ACWI Gross. VC/growth was especially strong at 31% globally, while Asia/Rest of World lagged because of China-specific domestic pressures. In other words, COVID was a violent shock, but not a prolonged one for private markets. Once liquidity returned and stimulus took hold, the rebound came quickly.

The nuance matters though. The macro forces this time were very different from 2008. Investments post-GFC benefited from record-low rates, rising multiples, and steady GDP growth. COVID’s recovery, by contrast, eventually triggered inflation and rising interest rates, putting upward pressure on borrowing costs and making the road back considerably harder for leveraged strategies. The extraordinary 2020 performance triggered a flood of capital in 2021 and those who deployed at the top of that wave set up the next correction.

Bain & Company’s piece on COVID’s impact on PE is worth reading in full. Written at the height of the crisis, it’s a striking document, making the case for PE’s resilience while being honest about the unknowns. It reads differently with hindsight, and that’s precisely what makes it valuable.

The lesson: COVID showed that private markets can absorb even a sudden-stop shock when capital, policy support, and operating flexibility arrive quickly enough. The managers who moved fast to stabilise portfolios were the ones best positioned to benefit from the rebound that followed.

TL;DR: COVID delivered a sudden-stop shock to private markets, followed by one of the fastest recoveries in recent memory. Managers who moved quickly came out ahead, but the strength of that rebound also fed into the inflation and rate cycle of 2022–23, which made the next chapter much harder.

What Happened

After a decade of near-zero rates, inflation surged to multi-decade highs. Central banks responded with the fastest tightening cycle in a generation, and Russia’s invasion of Ukraine deepened the energy shock, keeping inflation elevated for longer than many investors expected. The result was a market environment defined by higher financing costs, weaker growth expectations, and a much less forgiving backdrop for risk assets.

What It Did to Private Markets

This was the first difficult period in years that private markets could not simply outrun. Rising rates hit from every direction. Financing became more expensive, entry and exit multiples reset lower, and the old tailwinds of cheap leverage and multiple expansion faded quickly. McKinsey report noted that two-thirds of buyout returns on deals entered in 2010 or later and exited by 2021 had come from market multiple expansion and leverage. By 2023, that engine was no longer working the same way.

The strain showed up most clearly in fundraising and liquidity. Global private-markets fundraising fell 22% in 2023 to just over $1 trillion, the lowest level since 2017. Managers held onto assets rather than sell into a lower-multiple environment, which left LPs starved of distributions and less able to recommit. The exit backlog became the defining problem: global PE exits by count fell 23%, dollar-volume exits fell to $840 billion, and average holding periods rose to a record 6.8 years.

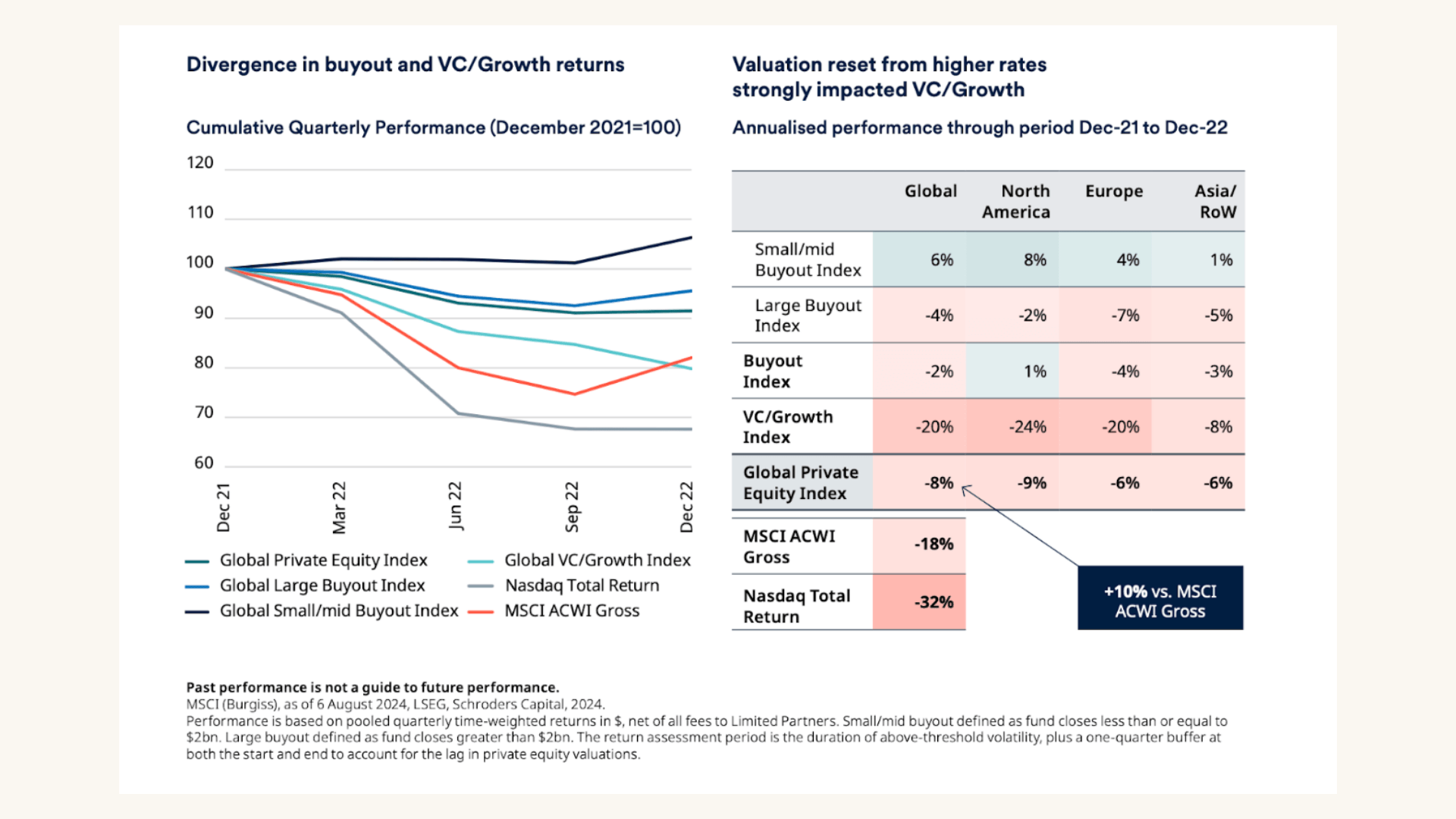

The chart captures the internal split this cycle created. Buyout was bruised, but venture and growth were hit much harder by the valuation reset. From December 2021 to December 2022, the Global Private Equity Index fell 8% annualised, versus an 18% decline for MSCI ACWI Gross and a 32% drop for the Nasdaq. But within private equity, outcomes diverged sharply: small and mid buyouts still delivered +6% globally, while VC/growth fell 20%. This was less a broad private-markets crash than a repricing of duration, leverage, and growth expectations.

Scale mattered too. The 25 largest fundraisers collected 41% of all commitments to closed-end funds, while smaller and newer managers struggled badly. Fewer than 1,700 sub-$1 billion funds closed in 2023, half as many as in 2022, and new manager formation fell to its lowest level since 2012. Private debt stood out as one of the more resilient areas of private markets in a higher-rate world, even if it was not immune.

The lesson: this cycle did not reward speed. It rewarded patience, scale, and realistic underwriting. In a slower, higher-rate world, private-market resilience depended less on outrunning the downturn and more on surviving the liquidity squeeze without forcing bad decisions.

TL;DR The rate shock did not break private markets overnight but it did wear them down. The private markets were forced into patience mode. In this cycle, resilience came less from boldness than from scale, discipline, and the ability to wait.

What’s happening now

The current Iran conflict is still unfolding, which makes this different from the earlier episodes in this piece. Since late February, markets have had to absorb a renewed geopolitical shock layered on top of an already fragile macro backdrop. Oil has swung sharply as fighting has continued and disruption around the Strait of Hormuz has raised the risk of a more persistent energy shock. Brent has recently traded back above $100 after sharp moves in both directions, a sign that markets are still struggling to price the duration and severity of the conflict.

What it could mean for private markets

Private markets were already in the process of normalizing before the conflict, with exits and distributions recovering gradually. This shock adds another layer of uncertainty to that backdrop. In that environment, secondary markets naturally become more relevant, because they remain one of the few channels through which liquidity can still move when traditional exits stall. Crucially, that is happening against a backdrop of substantial dry powder, which should continue to support stronger assets even as volatility rises. The result is a market more likely to reprice selectively than seize up altogether.

Franklin Templeton’s highest-conviction call within private markets is also secondaries. The structural need for liquidity only intensifies in a prolonged conflict, creating a durable advantage for secondary strategies that can step in and provide that liquidity.

(Excerpt from Franklin Templeton)

What to watch

It is too early to draw conclusions about vintage outcomes. The more useful question for now is where the strain shows up first. The key watchpoints are oil, inflation expectations, the pace of exit recovery, and whether liquidity pressure pushes more investors toward secondaries. With the situation still unfolding, this remains an active test of how private markets respond to renewed geopolitical volatility.

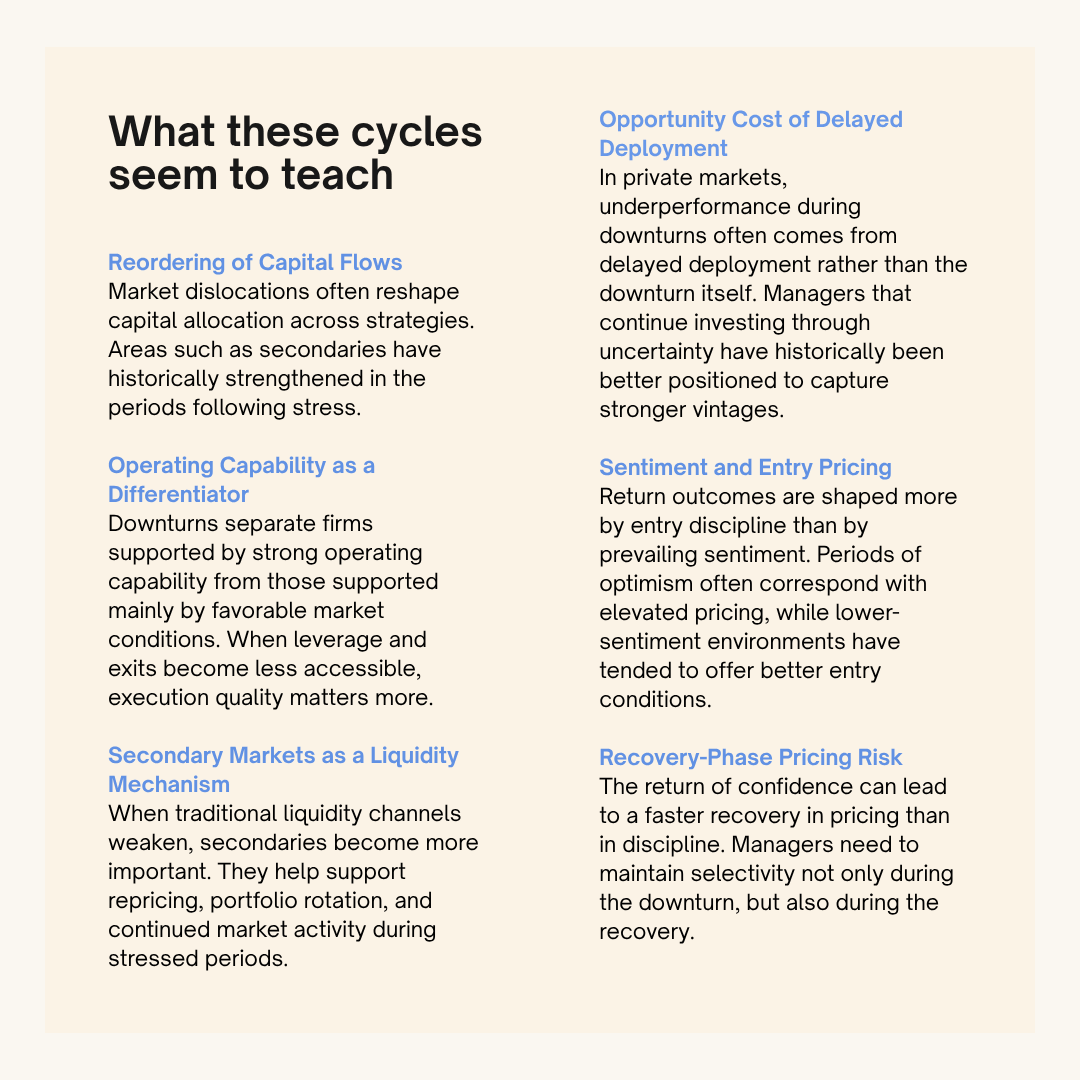

The pattern across every major crisis of the modern era stands out clearly. Quality in private markets is counter-cyclical, and high-quality private market opportunities tend to perform even better in periods of uncertainty.

The managers who came out ahead were the ones who had the operational infrastructure to protect value on the way down, the discipline not to overpay on the way up, and the conviction to keep deploying when everything around them said stop.

History suggests private markets do recover. The last 25 years of data point in the same direction that private markets have outperformed listed markets through five major crises- the difference, in practice, comes down to staying committed.

Jai Hind

TERMS OF USE

Thank you for your interest in our Website at https://unlistedintel.com/. Your use of this Website, including the content, materials and information available on or through this Website (together, the “Materials”), is governed by these Terms of Use (these “Terms”). By using this Website, you acknowledge that you have read and agree to these Terms.

NO OFFER, SOLICITATION OR ADVICE

Our site is provided for informational purposes only. It does not constitute to constitute (i) an offer, or solicitation of an offer, to

purchase or sell any security, other assets, or service, (ii) investment, legal, business, or tax advice, or an offer to provide such advice or (iii) a basis for making any investment decision.

The Materials are provided for informational purposes and have been prepared by Oister Global for informational purposes to acquaint existing and prospective underlying funds, entrepreneurs, and other company founders with Oister Global's recent and historical investment activities.

Please note that any investments or portfolio companies referenced in the Materials are illustrative and do not reflect the performance of any Oister Global fund as a whole. There is no obligation for Oister Global to update or alter any forward-looking statements, whether as a result of new information, future events, or otherwise.

PURPOSE LIMITATION AND ACCESS TO YOUR PERSONAL DATA:

We will only collect your personal data in a fair, lawful, and transparent manner. We will keep your personal data accurate and up to date. We will process your personal data in line with your legal rights. We use your name and contact details, such as email, postal address, and contact number to continue communications with you. We may also use your contact information to invite you to events we are hosting or to keep you updated with our news.

USE OF COOKIES OR SIMILAR DEVICES

We use cookies on our website. This helps us to provide you with a better experience when you browse our website and also allows us to make improvements to our site. You may be able to change the preferences on your browser or device to prevent or limit your device’s acceptance of cookies, but this may prevent you from taking advantage of some of our features.

MATERIAL

The material displayed on our site is provided “as is”, without any guarantees, conditions, or warranties as to its accuracy, completeness, or reliability. You should be aware that a significant portion of the Materials includes or consists of information that has been provided by third parties and has not been validated or verified by us. In connection with our investment activities, we often become subject to a variety of confidentiality obligations to funds, investors, portfolio companies, and other third parties. Any statements we make may be affected by those confidentiality obligations, with the result that we may be prohibited from making full disclosures.

MISCELLANEOUS

This Website is operated and controlled by Oister Global in India. We may change the content on our site at any time. If the need arises, we may suspend access to our site, or close it indefinitely. We are under no obligation to update any material on our site.

CONTACT INFORMATION

Any questions, concerns or complaints regarding these Terms should be sent to info@oisterglobal.com