Dear Reader,

Halfway through 2025 already, time’s flying like it’s chasing IRR. In six short months, India became the world’s fourth-largest economy, global markets got whiplash, and even your family WhatsApp group became a source of breaking news.

But last week reminded us how swiftly momentum can turn into stillness.

The Air India crash in Ahmedabad brought with it a wave of collective pause, grief, reflection, and a sharp sense of fragility. As participants in this ecosystem, we extend our quiet solidarity to the families affected, the teams connected, and the responders still absorbing its weight.

So today, we’re stepping off the carousel. No predictions. No FOMO. Just a quiet meditation on what draws us in, especially when everyone seems to want the same thing.

Humans are wired to want what others want. In evolutionary terms, mimicry was a survival mechanism. If someone in your tribe ate a particular fruit, built a certain kind of shelter, or chose a mate with specific traits, you followed. Mimicry kept us alive, adaptive, and aligned. In the wild, going with the crowd meant protection. In markets today, it still lingers. Oversubscribed rounds trigger the same reflex: If others want it, I must be missing something. A top-tier fund backing a founder speeds up the round, even if the model is hazy. A WhatsApp group of angels fills an allocation in hours, and people commit – carried by urgency, long before conviction has time to land. The form is different. But the emotional software hasn’t changed.

FOMO, coined in 2004, mainstreamed by 2011, entered the Indian investing vocabulary shortly after. But the emotion long predates the term. That flutter when others act before you do. That tightening happens when a deal closes without you. We didn’t always have a word for it, because long before there was language, there was instinct. And instinct said: belonging feels safer than thinking alone.

This pattern shows up everywhere. In school, it’s matching hoodies. In adulthood, mimicry gets dressed up- subtler, costlier, no less communal. Take the Labubu charm craze. What began as a niche collectable in East Asia now hangs from Hermès and Goyard bags across South Bombay and Delhi. The instinct never left. It simply started carrying a Centurion.

Real estate, our oldest allocation instinct, reflects the same mimicry. DLF’s Dahlias moved ₹12,000 crore in months. Trump Towers sold ₹3,250 crore on Day One. Now, India’s top four developers are chasing ₹1 trillion in FY26 sales. The market feels buoyant, eyes fixed on the crowd. Bookings spark movement. Instinct rushes in. FOMO drives the sellout, tower by tower.

The sheer cultural appetite for shows like The White Lotus or the recent Jon Hamm starrer on Apple TV – Your Friends and Neighbours points to something deeper than voyeurism. They go beyond portraying affluence, they decode its emotional cost. Who gets the best room? Who belongs. Who pretends not to care. Wealth as performance. Anxiety. The quiet, coded humiliations of being almost rich, newly rich, rich yet excluded. The same tension in WhatsApp investor groups. The same choreography across cap tables.

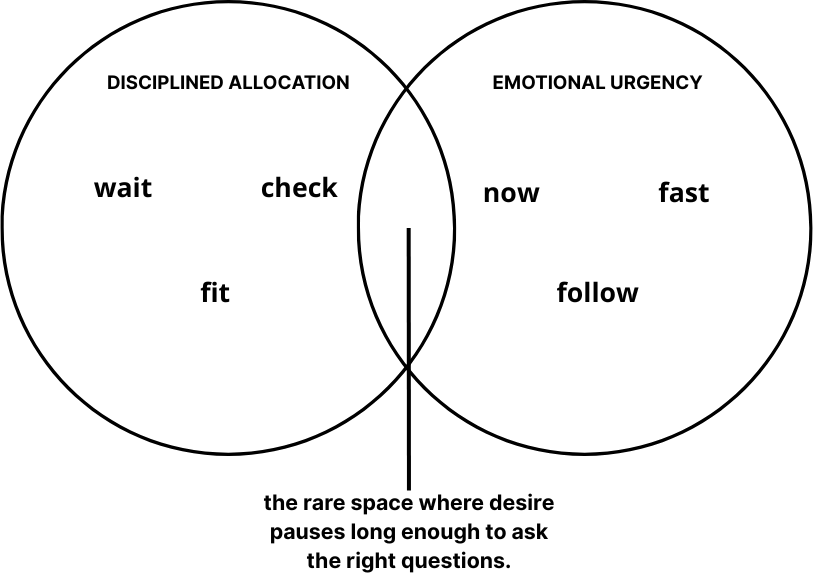

In Indian private capital, a countercurrent is gaining strength. Over the past two years, in our role as alternative asset managers, we’ve sat across from hundreds of allocators – legacy money, family offices, underwritten UHNIs, and felt the shift viscerally. The questions are sharper. Investors no longer ask how early they are. They ask how aligned. They want underwriting that mirrors their pace, their principles, and their preferred path.

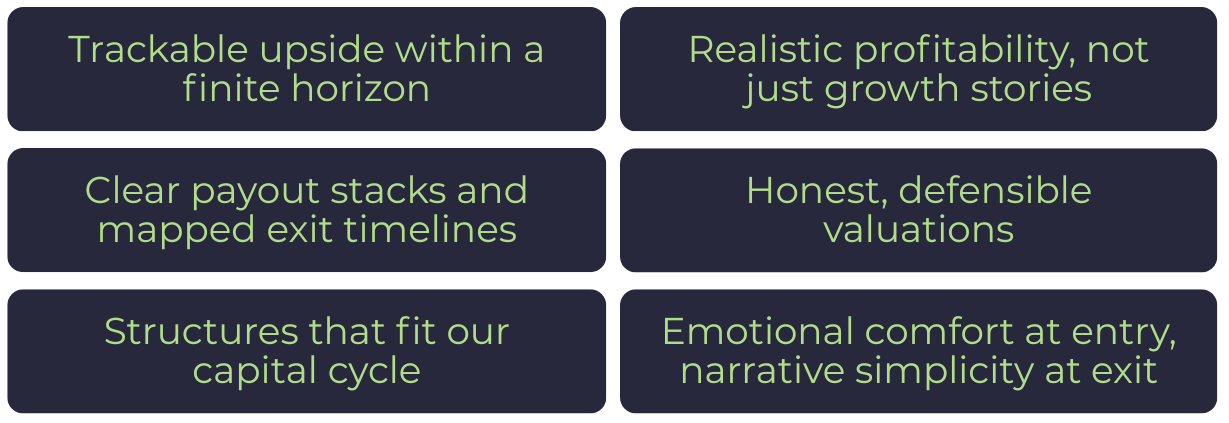

“How early are we?” has become “What’s the payout stack?” IRRs still matter, but only after liquidity schedules are mapped. A 30–60% upside holds value not just for magnitude, but for measurability. Storytelling opens doors, but structure sustains conviction.

Returns matter. But the questions surrounding them have matured. What risk am I underwriting to get those returns? What is the liquidity window? Is this business generating cash? What does real profitability look like in this category? Questions about EBITDA margins, cash flow conversion, margin bridges, and debt structure are now routine. Most allocators read these breakdowns with the fluency of an analyst. If the fundamentals don’t hold, no narrative closes the gap.

Even when growth, governance, and product traction align, a single misaligned valuation can stall momentum. The most thoughtful allocators focus as much on what they avoid as on what they pursue.

Social momentum once made deal flow smoother. Now, it sets off alarms. If multiple firms are marketing the same cap table in the same month, allocators detect risk. No one wants to be the last one holding optimism. Emotional comfort now commands a premium. Long-horizon funds still hold their place, but more investors lean toward vehicles with clean architecture and mapped outcomes. The premium sits with simplicity – credible backers, short tenures, defined exits.

Consumer brands continue to raise quickly. Not because they are superior businesses, but because they are easier to relate to. If you’ve used the product, the diligence feels internalized. Liquidity in this cycle favors comfort over complexity.

Mature capital, capital with memory and method, moves with discernment. The most experienced investors are not treating allocation as a speed test. They track behaviour, both others’ and their own. They underwrite people, timing, and the choreography of exit. Investing goes beyond perfect foresight. It’s about deliberate exposure.

In this macro climate, the contrast has become clear. Some investors lean out. Others lean in, but only when the fit is calibrated. Everyone sees the same deals. The advantage now lies in what gets skipped. Fit matters more than flash.

The arc of wealth always moves from exposure to insulation. From flex to focus. From being seen in rooms to deciding who enters yours. The next edge lives in discipline. In knowing which signals carry weight. And which are just echoes.

That’s how intelligence behaves in a crowded market. Mimicry helped us survive. Discernment helps us grow.

Sources:

TERMS OF USE

Thank you for your interest in our Website at https://unlistedintel.com/. Your use of this Website, including the content, materials and information available on or through this Website (together, the “Materials”), is governed by these Terms of Use (these “Terms”). By using this Website, you acknowledge that you have read and agree to these Terms.

NO OFFER, SOLICITATION OR ADVICE

Our site is provided for informational purposes only. It does not constitute to constitute (i) an offer, or solicitation of an offer, to

purchase or sell any security, other assets, or service, (ii) investment, legal, business, or tax advice, or an offer to provide such advice or (iii) a basis for making any investment decision.

The Materials are provided for informational purposes and have been prepared by Oister Global for informational purposes to acquaint existing and prospective underlying funds, entrepreneurs, and other company founders with Oister Global's recent and historical investment activities.

Please note that any investments or portfolio companies referenced in the Materials are illustrative and do not reflect the performance of any Oister Global fund as a whole. There is no obligation for Oister Global to update or alter any forward-looking statements, whether as a result of new information, future events, or otherwise.

PURPOSE LIMITATION AND ACCESS TO YOUR PERSONAL DATA:

We will only collect your personal data in a fair, lawful, and transparent manner. We will keep your personal data accurate and up to date. We will process your personal data in line with your legal rights. We use your name and contact details, such as email, postal address, and contact number to continue communications with you. We may also use your contact information to invite you to events we are hosting or to keep you updated with our news.

USE OF COOKIES OR SIMILAR DEVICES

We use cookies on our website. This helps us to provide you with a better experience when you browse our website and also allows us to make improvements to our site. You may be able to change the preferences on your browser or device to prevent or limit your device’s acceptance of cookies, but this may prevent you from taking advantage of some of our features.

MATERIAL

The material displayed on our site is provided “as is”, without any guarantees, conditions, or warranties as to its accuracy, completeness, or reliability. You should be aware that a significant portion of the Materials includes or consists of information that has been provided by third parties and has not been validated or verified by us. In connection with our investment activities, we often become subject to a variety of confidentiality obligations to funds, investors, portfolio companies, and other third parties. Any statements we make may be affected by those confidentiality obligations, with the result that we may be prohibited from making full disclosures.

MISCELLANEOUS

This Website is operated and controlled by Oister Global in India. We may change the content on our site at any time. If the need arises, we may suspend access to our site, or close it indefinitely. We are under no obligation to update any material on our site.

CONTACT INFORMATION

Any questions, concerns or complaints regarding these Terms should be sent to info@oisterglobal.com