Venture capital and private equity landscapes have long been enchanted by the allure of unicorns – those rare and mythical startups that soar to a valuation of $1 Bn or more. The journey from obscurity to unicorn status is a tale of high-risk, high-reward investments that can captivate the imagination of even the most seasoned investors.

Let’s delve into the numbers. Chart 1 paints a picture of exhilarating returns, showcasing the multiples of invested capital (MOIC) for early backers who rode the wave from a startup’s nascent stages to its unicorn coronation. With MOICs ranging from 130x to a staggering 2270x, it’s no wonder that unicorns have become the stuff of legend in the investment world.

But amid the fervour surrounding these unicorn success stories, a pertinent question arises: just how necessary are unicorns for achieving stellar returns?

The mission is to identify fund managers with a proven track record and the potential for future success, funds have engaged with numerous general partners (GPs) in the venture capital realm. Surprisingly, not a single GP who has passed through our rigorous due diligence process has made investing in unicorns a cornerstone of their strategy. Some are unequivocal in their stance that unicorn hunting is not their modus operandi.

The answer lies in two key factors.

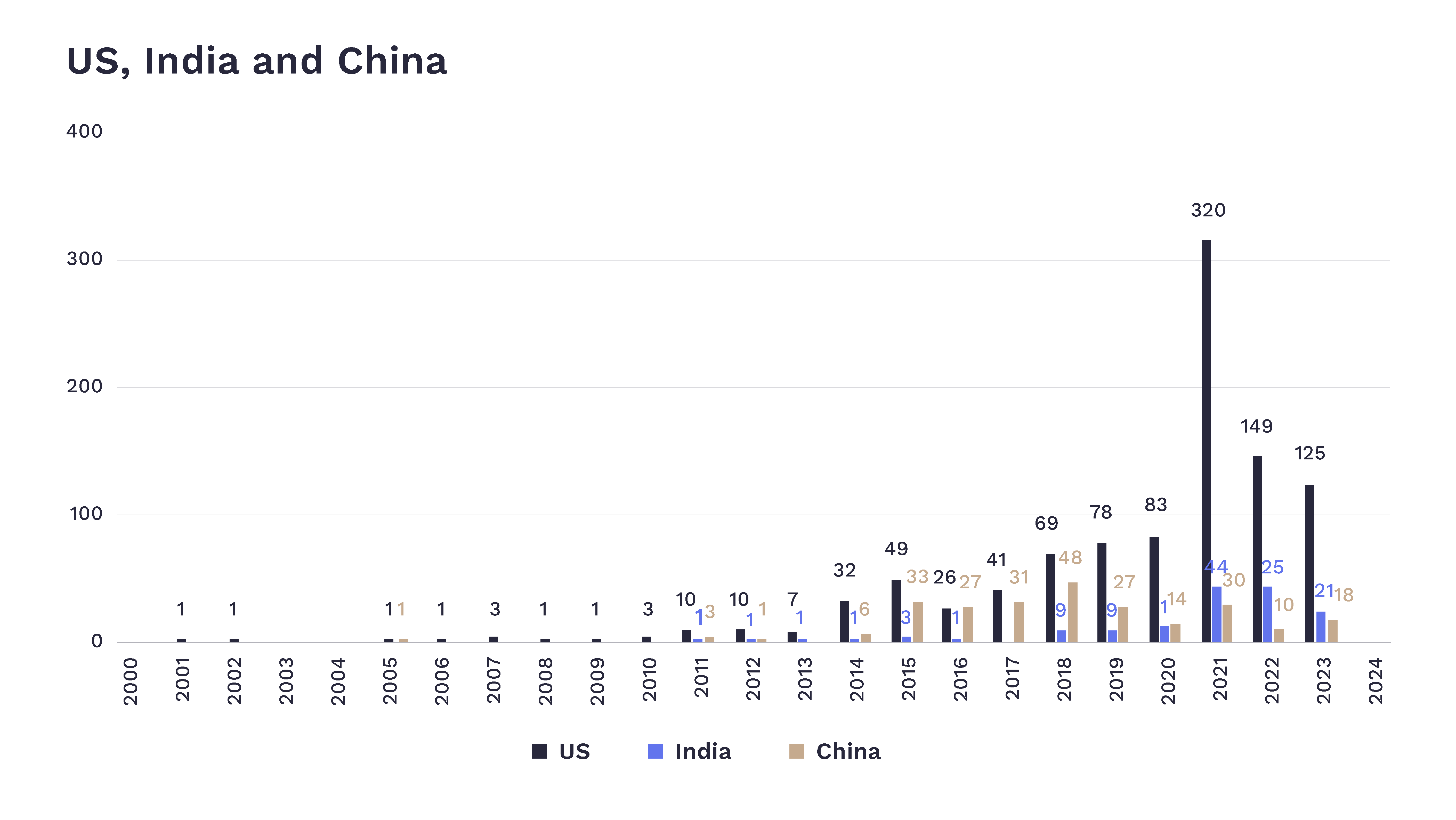

Firstly, unicorns are, by definition, rare. While there was a proliferation of unicorn sightings globally in 2021, fueled by low-interest rates, the landscape has since shifted. As illustrated in Chart 2, the unicorn population is once again dwindling, making it challenging to build a consistent investment strategy around these elusive beings.

Secondly, predicting which companies will ascend to unicorn status is akin to crystal ball gazing in a tempestuous market. Attaining a billion-dollar valuation hinges not only on the intrinsic quality of the company but also on the capricious mood of the market when valuations are set. This uncertainty makes it a rational choice for investors to seize the opportunity to cash in on a potential unicorn rather than holding out for an uncertain hope of an eventual billion-dollar payday.

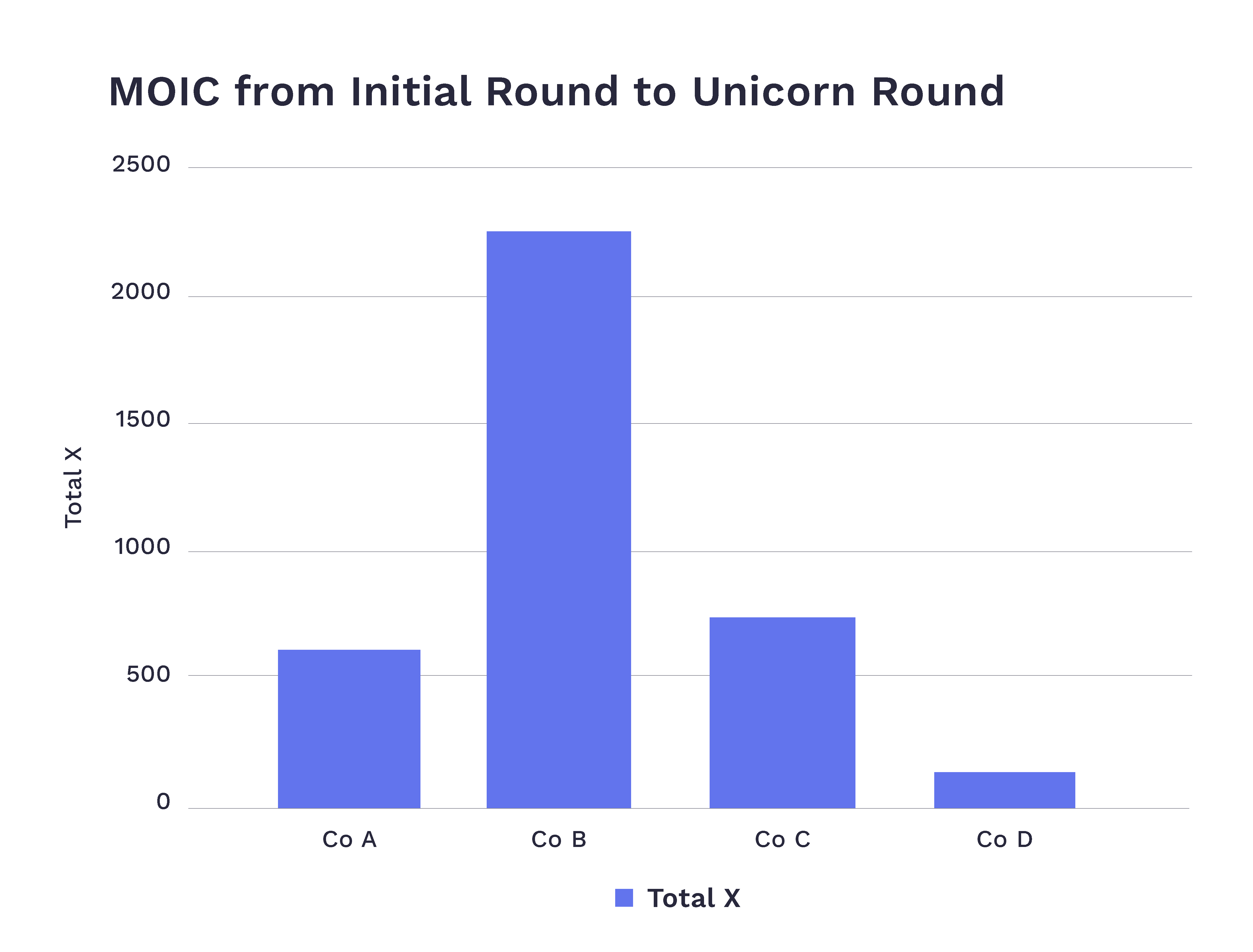

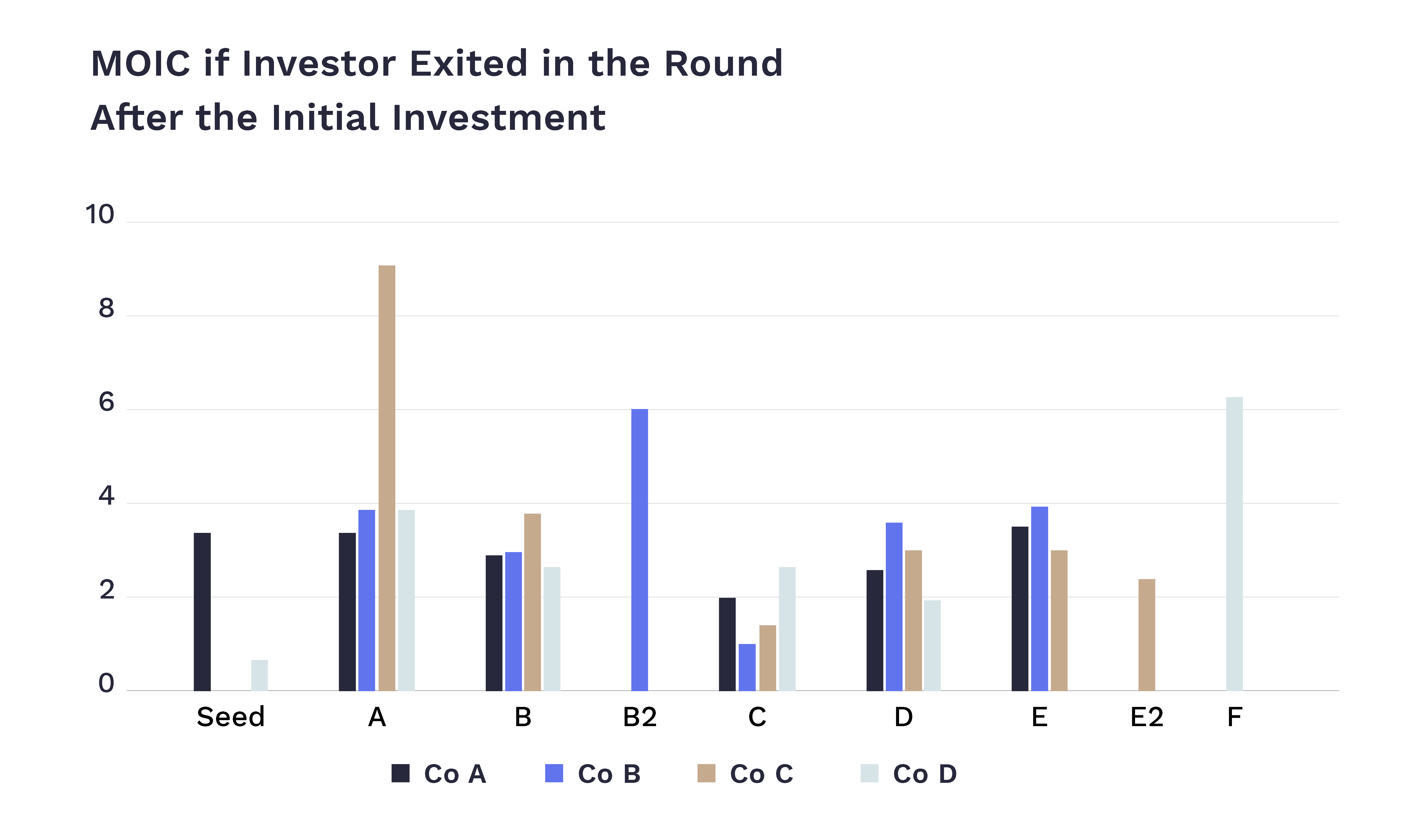

Chart 3 sheds light on the MOICs achieved at each funding round leading up to unicorn status for four real-world companies. On average each company went through six rounds of funding before it achieved unicorn status. The average MOIC per round was 3.3x. The average time between the first round and the round in which unicorn status was achieved was eight years, with a range of 5.5 years to 10.5 years.

The first thing to notice from Chart 3 is that the ‘Wow!’ multiples in Chart 1 don’t come quickly or all at once. It takes time and multiple rounds of funding to get there. If you only held for one round (you sold out at the round after you invested) on average you made 3.3x and this gets us to the first reason why GPs do not rely on achieving the MOICs in Chart 1.

Remarkably, even without reaching unicorn status, early investors reaped impressive returns, with an average MOIC of 3.3x per round. This underscores the attractiveness of cashing out at opportune moments along the investment journey, especially when the risk-reward calculus favours taking profits.

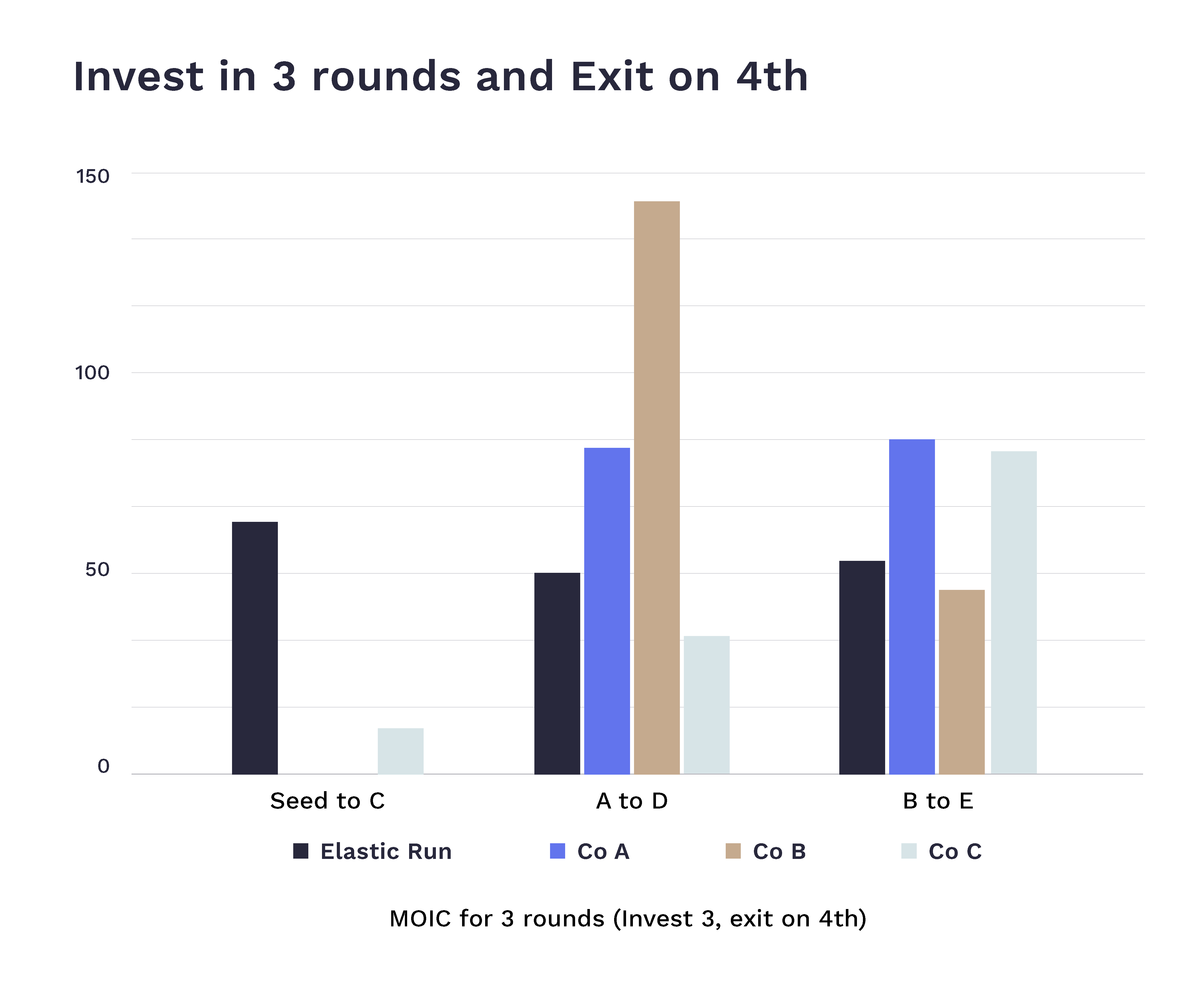

Chart 4 further underscores this point, revealing that exiting just two rounds after the initial investment yielded an average MOIC of 20x. The average holding period is 1.75 years with a range of 0.5 years to three years.

A 20x return on a single investment is possibly enough to return a fund – that is, get to a DPI of 1x via a single exit! The risk/return calculus begins to swing in favour of taking the exit. If you can effectively de-risk your fund for your investors with a single exit it takes a lot of conviction to take the risk and continue to hold.

Beyond the calculus of risk and return, there is a question of for how many rounds an investor can stay in the game.

The VC ecosystem places boundaries on what is feasible. Each fund has limited capital and a limited life. Investors, especially early-stage VC investors, will structure their funds with significant reserves so that they can follow the strongest performers in a fund for the next one or two rounds. However, eventually, each fund runs out of both time and money.

The typical fund has restrictions which aim to ensure that it winds up in time. It can make primary investments for 5 years and continue to invest in follow-on rounds until the sixth year and must exit all investments by year 10. In our sample of four Unicorns, two took 10 or more years to become Unicorns.

With each fund bound by restrictions that dictate investment horizons and exit timelines, the reality is that riding a future unicorn from inception to unicorn status is a rare feat. This, coupled with the inherent scarcity of unicorns, explains why GPs who have passed the due diligence eschew unicorn chasing as a core strategy.

In conclusion, while unicorns may dazzle with their allure, achieving exceptional returns in the venture capital landscape does not hinge solely on capturing these mythical creatures. Prudent investment decisions, timely exits, and strategic portfolio management are equally vital in navigating the unpredictable terrain of startup investing. As investors chart their course in pursuit of success, the quest for unicorns may continue to captivate, but its necessity remains open to interpretation.

TERMS OF USE

Thank you for your interest in our Website at https://unlistedintel.com/. Your use of this Website, including the content, materials and information available on or through this Website (together, the “Materials”), is governed by these Terms of Use (these “Terms”). By using this Website, you acknowledge that you have read and agree to these Terms.

NO OFFER, SOLICITATION OR ADVICE

Our site is provided for informational purposes only. It does not constitute to constitute (i) an offer, or solicitation of an offer, to

purchase or sell any security, other assets, or service, (ii) investment, legal, business, or tax advice, or an offer to provide such advice or (iii) a basis for making any investment decision.

The Materials are provided for informational purposes and have been prepared by Oister Global for informational purposes to acquaint existing and prospective underlying funds, entrepreneurs, and other company founders with Oister Global's recent and historical investment activities.

Please note that any investments or portfolio companies referenced in the Materials are illustrative and do not reflect the performance of any Oister Global fund as a whole. There is no obligation for Oister Global to update or alter any forward-looking statements, whether as a result of new information, future events, or otherwise.

PURPOSE LIMITATION AND ACCESS TO YOUR PERSONAL DATA:

We will only collect your personal data in a fair, lawful, and transparent manner. We will keep your personal data accurate and up to date. We will process your personal data in line with your legal rights. We use your name and contact details, such as email, postal address, and contact number to continue communications with you. We may also use your contact information to invite you to events we are hosting or to keep you updated with our news.

USE OF COOKIES OR SIMILAR DEVICES

We use cookies on our website. This helps us to provide you with a better experience when you browse our website and also allows us to make improvements to our site. You may be able to change the preferences on your browser or device to prevent or limit your device’s acceptance of cookies, but this may prevent you from taking advantage of some of our features.

MATERIAL

The material displayed on our site is provided “as is”, without any guarantees, conditions, or warranties as to its accuracy, completeness, or reliability. You should be aware that a significant portion of the Materials includes or consists of information that has been provided by third parties and has not been validated or verified by us. In connection with our investment activities, we often become subject to a variety of confidentiality obligations to funds, investors, portfolio companies, and other third parties. Any statements we make may be affected by those confidentiality obligations, with the result that we may be prohibited from making full disclosures.

MISCELLANEOUS

This Website is operated and controlled by Oister Global in India. We may change the content on our site at any time. If the need arises, we may suspend access to our site, or close it indefinitely. We are under no obligation to update any material on our site.

CONTACT INFORMATION

Any questions, concerns or complaints regarding these Terms should be sent to info@oisterglobal.com