Healthcare in India is not just a sector – it is an economic imperative, a structural growth engine, and an investment goldmine. From policy tailwinds to demographic surges, from underbuilt infrastructure to a digitally transforming delivery system, every signal points in one direction: this is India’s healthcare decade. For long-term capital, this sector offers a unique confluence of scale, defensiveness, formalization, and high-return potential.

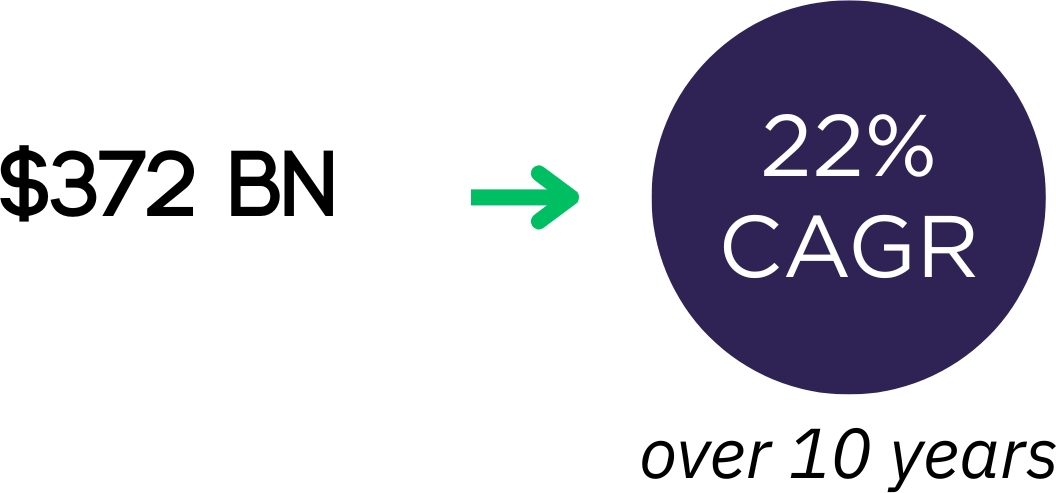

India’s healthcare market, valued at $372 Bn, has been growing consistently at a 22% CAGR over the past decade. This growth is not just a reflection of economic metrics; it underscores a deeper narrative: the nation’s burgeoning demand for quality healthcare services juxtaposed against a constrained supply infrastructure.

India’s healthcare market

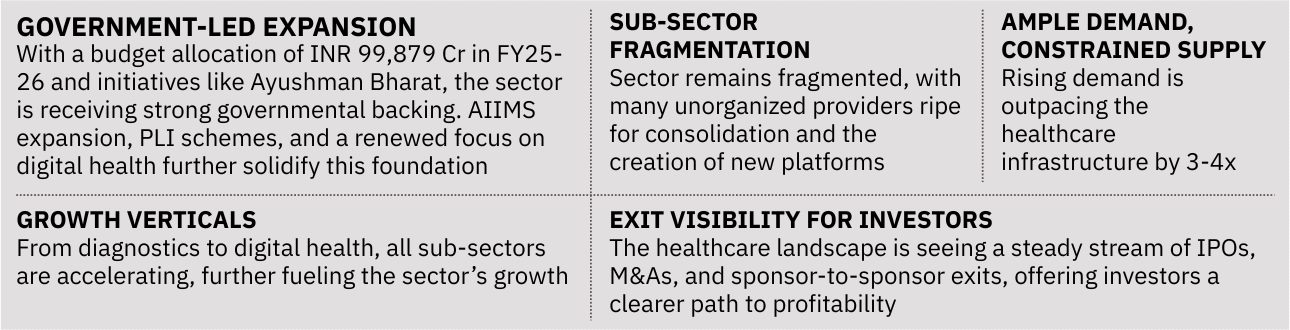

India’s healthcare sector is uniquely positioned to benefit from a rare convergence of key structural tailwinds:

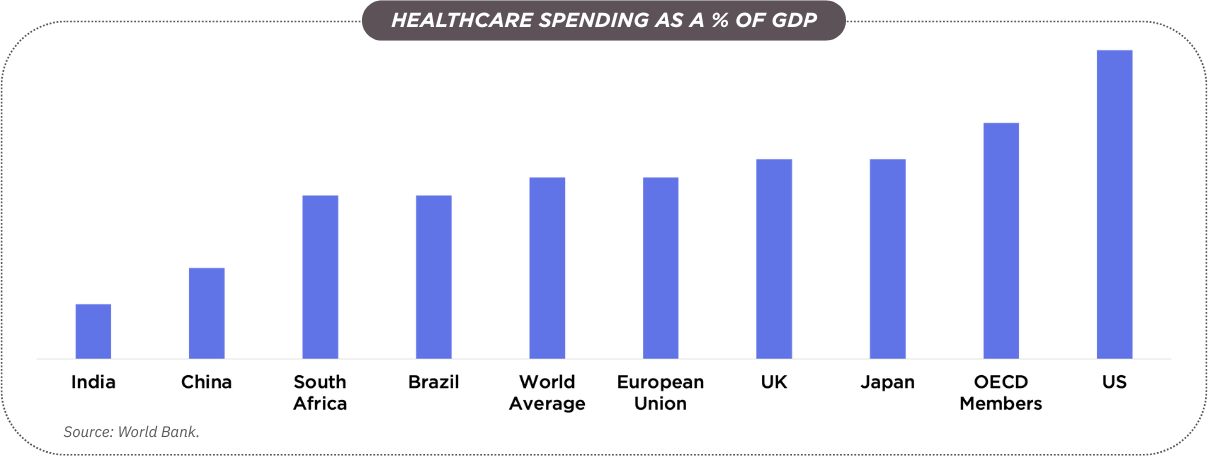

Despite the growing demand for healthcare and a positive government push, India’s healthcare spending as a percentage of GDP remains one of the lowest among major economies. This reflects the challenge of bridging the gap between demand and government expenditure in a sector that is both underfunded and underdeveloped. Below is a comparison of healthcare spending as a percentage of GDP, further highlighting the opportunity for growth and investment.

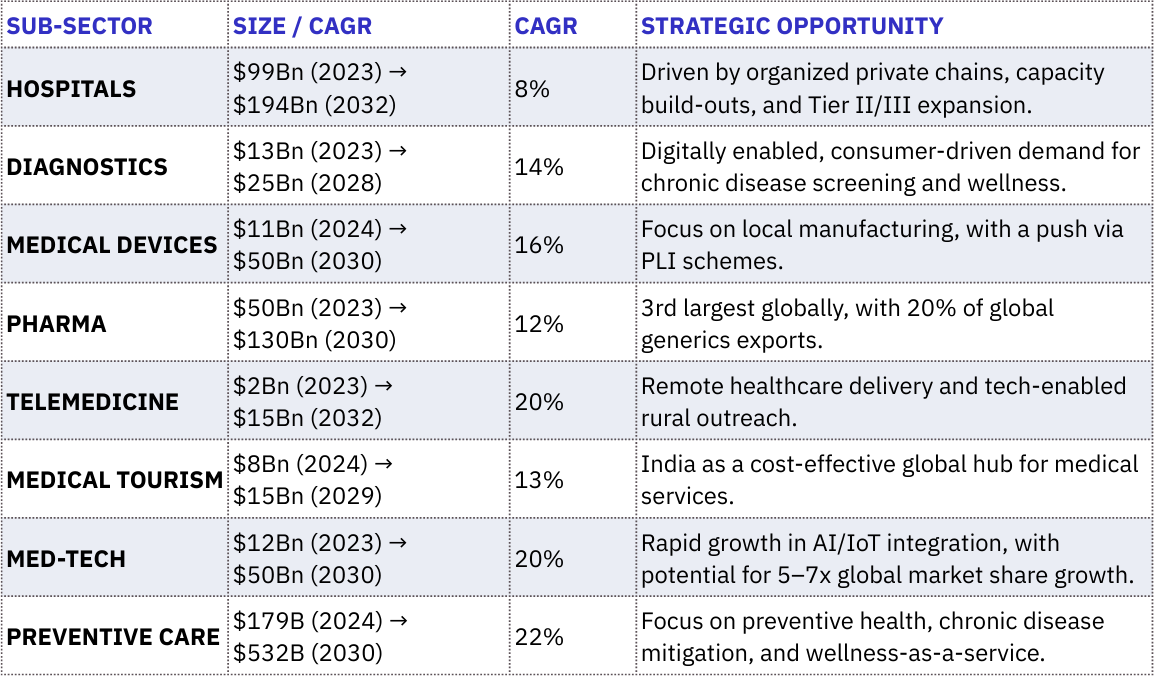

Several sub-sectors within India’s healthcare ecosystem are expected to grow exponentially.

These sub-sectors represent diverse opportunities for stakeholders to tap into a rapidly evolving market.

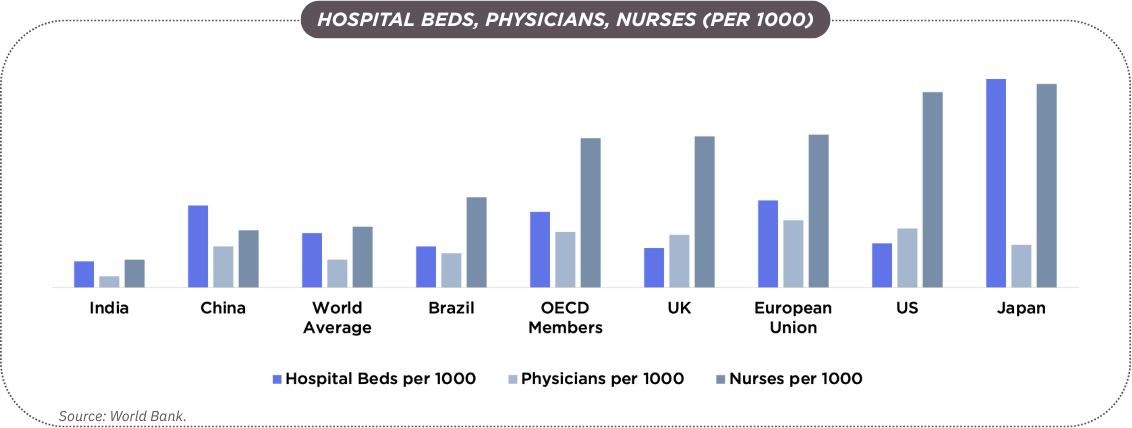

While India’s healthcare demand is soaring, driven by an expanding population, an increasing prevalence of non-communicable diseases, and growing health awareness, the supply side struggles to keep up. With a bed-to-patient ratio of 1.6:1000 and a doctor-to-patient ratio of 0.7:1000, India lags behind global standards. To meet international standards by 2034, India will need to add:

This supply-demand gap presents not only a challenge but also a massive opportunity: addressing the supply constraints can not only elevate healthcare standards but also unlock significant investment avenues.

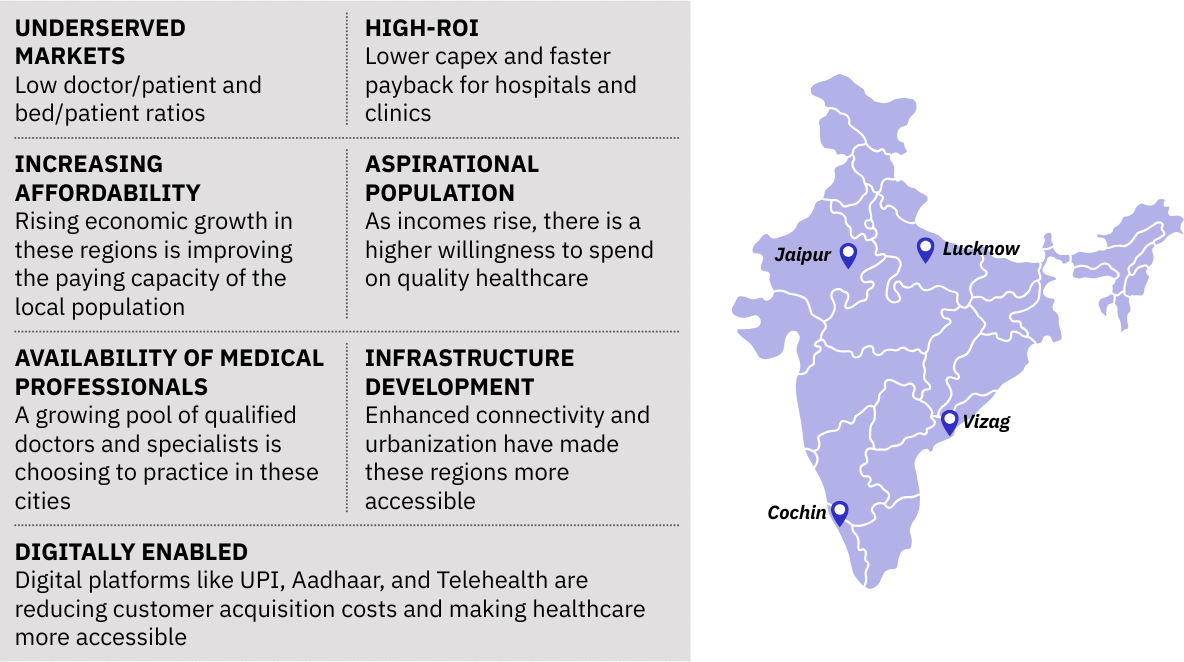

While metropolitan areas have traditionally been the hub for healthcare services, a paradigm shift is underway. By 2030, more than 50% of incremental healthcare demand will emerge from Tier II and III cities. Cities like Lucknow, Vizag, Jaipur, and Cochin are becoming the new frontiers for healthcare expansion. The factors fueling this transformation include:

This shift addresses the urban-rural divide and paves the way for scalable, sustainable healthcare models across India.

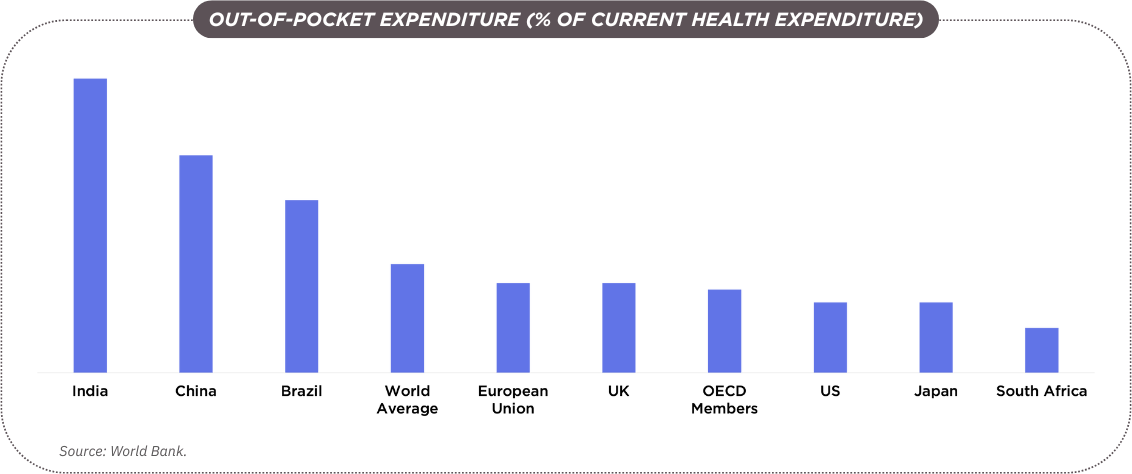

In India, out-of-pocket (OOP) expenditure remains the highest in the world. The chart below illustrates the high percentage of health spending that comes directly from individuals, underlining the financial strain on the population, especially in underserved areas. This financial burden further exacerbates the need for a more inclusive, accessible, and affordable healthcare system.

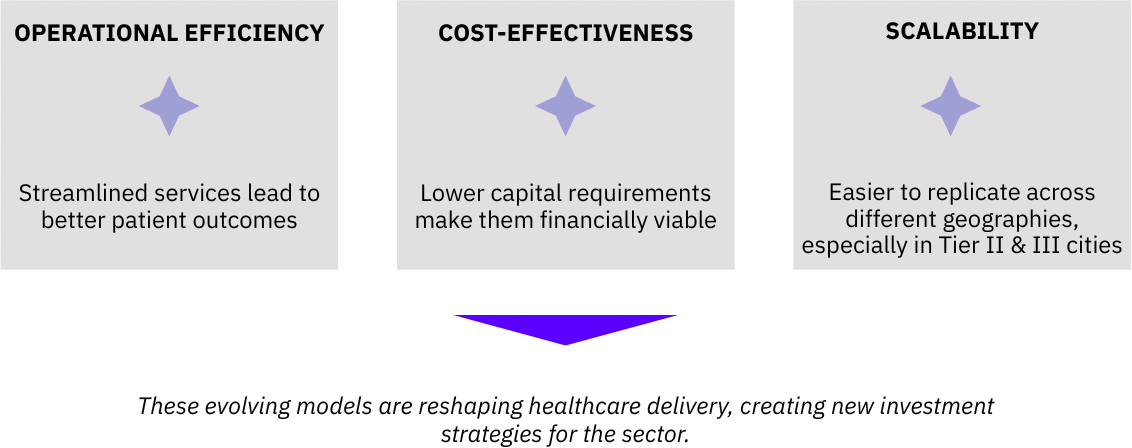

The traditional multi-specialty hospital model, while comprehensive, often entails significant capital expenditure and longer gestation periods. In contrast, Single-specialty hospitals in areas such as oncology, nephrology, and mother & child care are gaining traction. These smaller facilities (typically 40-50 beds) offer:

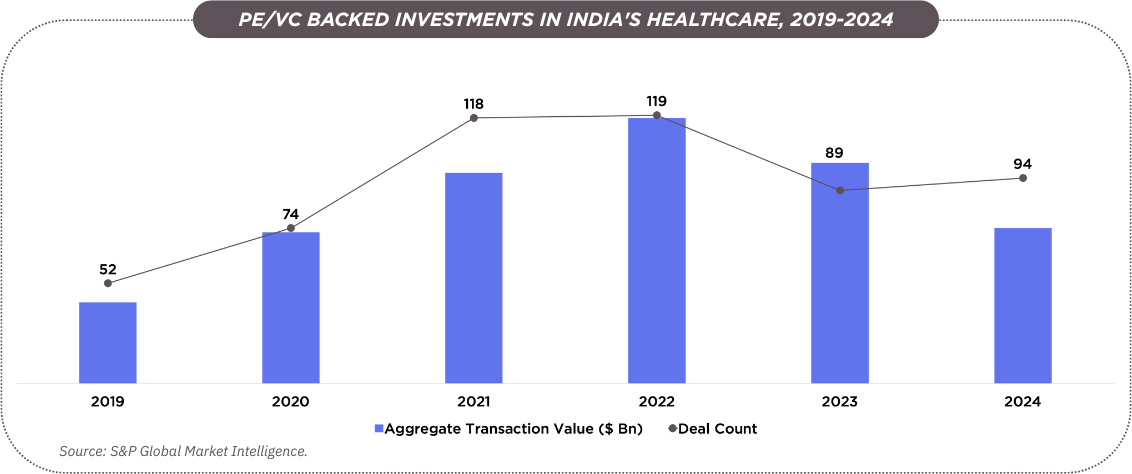

Over the past decade, India’s healthcare and pharmaceutical sectors have attracted significant investments. Between 2014 and 2024, 594 M&A and private equity transactions worth over $30 Bn took place, with hospitals accounting for nearly 40% of these deals.

This wave of investment underscores the sector’s attractiveness for those seeking long-term, transformative growth.

While public initiatives lay the foundation, private capital is accelerating healthcare development. As per Bain’s report titled, “Global Healthcare Private Equity Report 2025”, India became the largest healthcare private equity (PE) market in Asia-Pacific in 2024, accounting for 26% of all deal volume in the region. Private investments have enabled hospital chains and healthcare providers to expand, integrate new technologies, and diversify their services.

The collaboration between public policy and private expertise ensures that India’s healthcare challenges are met with a holistic approach, fostering sustainable growth and development in the sector.

Reflecting on the strength and attractiveness of the Indian markets, Joseph Bae, Co-CEO of KKR, highlighted in an interview with Economic Times the significance of the country’s stability and infrastructure growth:

“The political stability of this country has been a huge positive. The pro-growth mindset around infrastructure investing has been a huge tailwind to growth in the country.”

Bae also emphasized how the Indian markets’ evolution has benefitted private equity investors, particularly in terms of liquidity:

“One of the most fundamental things that has changed in India for private equity investors versus 10 years back is the path to liquidity. Private equity investors, including ourselves, have a lot more comfort if we make large-scale investments in India in really great businesses, the ability to exit and monetize those investments at good prices is better today than it’s ever been.”

India’s healthcare sector stands at the threshold of a transformative decade. The convergence of rising demand, infrastructural needs, governmental support, and innovative healthcare models creates an environment primed for comprehensive growth. Addressing the sector’s supply constraints is not just a necessity but a monumental opportunity to redefine healthcare delivery in India.

Stakeholders who align with this vision will play a pivotal role in building a resilient, inclusive, and efficient healthcare ecosystem in India, which could well become one of the most rewarding investment opportunities of the next decade.

TERMS OF USE

Thank you for your interest in our Website at https://unlistedintel.com/. Your use of this Website, including the content, materials and information available on or through this Website (together, the “Materials”), is governed by these Terms of Use (these “Terms”). By using this Website, you acknowledge that you have read and agree to these Terms.

NO OFFER, SOLICITATION OR ADVICE

Our site is provided for informational purposes only. It does not constitute to constitute (i) an offer, or solicitation of an offer, to

purchase or sell any security, other assets, or service, (ii) investment, legal, business, or tax advice, or an offer to provide such advice or (iii) a basis for making any investment decision.

The Materials are provided for informational purposes and have been prepared by Oister Global for informational purposes to acquaint existing and prospective underlying funds, entrepreneurs, and other company founders with Oister Global's recent and historical investment activities.

Please note that any investments or portfolio companies referenced in the Materials are illustrative and do not reflect the performance of any Oister Global fund as a whole. There is no obligation for Oister Global to update or alter any forward-looking statements, whether as a result of new information, future events, or otherwise.

PURPOSE LIMITATION AND ACCESS TO YOUR PERSONAL DATA:

We will only collect your personal data in a fair, lawful, and transparent manner. We will keep your personal data accurate and up to date. We will process your personal data in line with your legal rights. We use your name and contact details, such as email, postal address, and contact number to continue communications with you. We may also use your contact information to invite you to events we are hosting or to keep you updated with our news.

USE OF COOKIES OR SIMILAR DEVICES

We use cookies on our website. This helps us to provide you with a better experience when you browse our website and also allows us to make improvements to our site. You may be able to change the preferences on your browser or device to prevent or limit your device’s acceptance of cookies, but this may prevent you from taking advantage of some of our features.

MATERIAL

The material displayed on our site is provided “as is”, without any guarantees, conditions, or warranties as to its accuracy, completeness, or reliability. You should be aware that a significant portion of the Materials includes or consists of information that has been provided by third parties and has not been validated or verified by us. In connection with our investment activities, we often become subject to a variety of confidentiality obligations to funds, investors, portfolio companies, and other third parties. Any statements we make may be affected by those confidentiality obligations, with the result that we may be prohibited from making full disclosures.

MISCELLANEOUS

This Website is operated and controlled by Oister Global in India. We may change the content on our site at any time. If the need arises, we may suspend access to our site, or close it indefinitely. We are under no obligation to update any material on our site.

CONTACT INFORMATION

Any questions, concerns or complaints regarding these Terms should be sent to info@oisterglobal.com