Strong returns begin with stronger questions and sharper underwriting.

Bullish on Monday, cautious by Thursday. By the weekend, we’re somewhere between AI euphoria, IPO fever, and trade paranoia. Bulls and bears are swapping jerseys and capital doesn’t seem to care.

We don’t talk enough about how much we’ve adapted. In just five years, we’ve normalized things that once felt unthinkable. AI writes our emails. “World War 3” trends weekly. Trade policy is dinner-table conversation.

In that time, a decade’s worth of market drama has been crammed into one relentless cycle: whiplash interest rates, tech bubbles and bursts, rules rewritten mid-game.

But through it all, one thing has held steady: investor appetite.

And increasingly, that appetite is steering toward one destination: private markets.

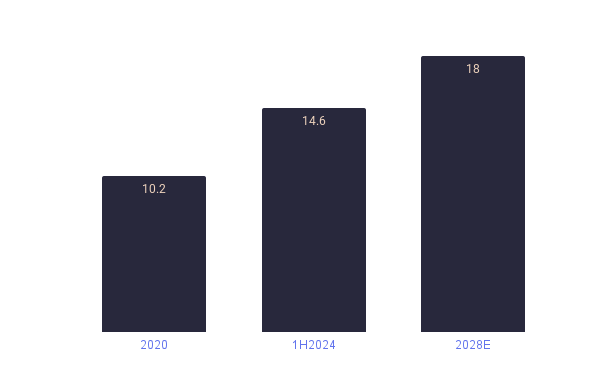

The numbers speak for themselves. Global private market AUM has grown from $10.2 trillion in 2020 to $14.6 trillion as of mid-2024, and is projected to hit $18 trillion by 2028. That’s a compound surge in just eight years and yet, it still represents just a third of the S&P 500’s market cap (as of December 2024). Which means: for all its scale, this asset class is still early in its mainstream adoption curve and has significant headroom for further growth.

Global private markets assets under management ($ trillion) | Source: UBS Private Markets Extended 2Q25

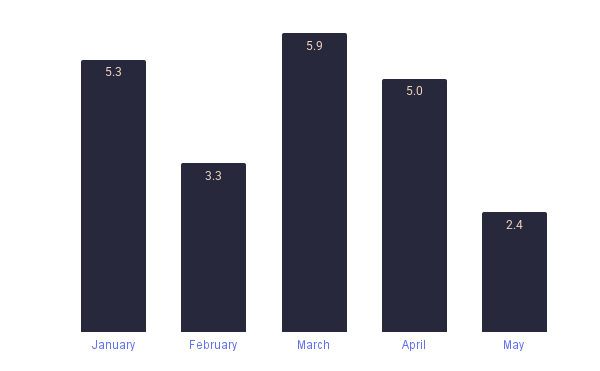

India tells a similar story. In the first five months of 2025 alone, PE-VC investments totaled approximately $22 billion, putting the country on track to surpass 2024’s total of $43 billion by year-end.

Monthly PE/VC Investments in India in 2025 ($ billion) | Source: IVCA EY Monthly PEVC Roundup May 2025

More tellingly, even traditionally public-markets focused institutions are making moves. Earlier this month, Vanguard announced its intention to offer private market access through its products, an unprecedented shift in tone from a firm built on passive public index funds. When a $10 trillion manager wants in, the writing is on the wall.

But as flows rise, so does the need for discernment. Private markets are not passive. There is no index to hide behind. And the spread in outcomes can be dramatic. Manager selection has become a critical driver of long-term return.

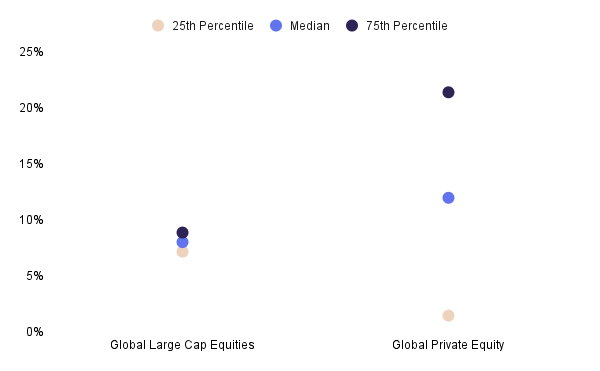

The chart below says it plainly: unlike public equities, the difference between top and bottom quartile managers in private equity isn’t marginal. Choosing the right manager is ultimately the gap between building wealth and missing the mark in private markets.

Public and Private Managers’ Returns Dispersion, (based on returns from 1Q15 – 1Q25) | Source: Guide to Alternatives – Q2 2025, J.P. Morgan Asset Management

In a market crowded with options, how do you know which funds are worth backing? What actually separates a product that performs from one that just promises? So if the money is real, the desire is sharp, and the questions are finally getting better –

Let’s get to it. What actually makes a private market product good?

Not every product is the same, nor should it be. Over the past few years, we’ve had the unusual vantage point of watching dozens of private market products move from pitch deck to deployment. Some flew off the shelf. Others needed time, iteration, and trust. We’ve sat in the room with families, institutions, and intermediaries, and heard the same question asked in different languages: Does this actually hold up?

As an alternative asset manager, we’ve invested across secondaries, fund-of-funds, and top-tier VC/PE funds, and private transactions across vintages, sectors, and geographies. That perspective doesn’t make us right. But it does make us grounded. What follows is what endures when the dust settles.

Here’s what tends to separate products that endure from those that don’t.

Strong underwriting starts with clarity.

Every deal should show:

You learn a lot by asking a manager one question: “What needs to go wrong for this to break?” The good ones don’t hesitate and don’t rely on vague themes or inflated narratives to justify themselves.

The core thesis is sound, assumptions are transparent, and the logic holds when tested. A good underwrite should make sense the first time you hear it.

It’s also where process matters. Every opportunity should run through a repeatable, institutional-grade lens, one that looks beyond the pitch to test durability. That means pressure-testing not just past performance, but how it was built: Is it repeatable? Is it concentrated or broad-based? Do team dynamics, carry splits, and decision rights support long-term value creation? Governance and downside protection also matter, what happens when things don’t go to plan?

Good underwriting is designed to ask the hard questions up front, so the answers hold up later. Good underwriting is designed to ask the hard questions up front so the answers hold up later.

Quick test: Can you explain the product’s core thesis in two sentences, without adjectives?

Strong products are built on real alignment.

In private markets, alignment is a design choice and great products engineer it with intent and clarity.

The strongest funds are built so that GPs and LPs win together, on the same timeline and under the same conditions. That means fee models that are transparent and reflect actual work. It means carry that rewards realised outcomes, not early paper gains. And it means GPs having meaningful capital at risk, committed for just as long as the LPs.

When incentives are structured well, they create trust. Everyone is rewarded the same way: by outcomes.

Quick test: Who gets paid, when, and based on what? If the answer isn’t simple, alignment might just be surface-deep.

Illiquidity only works when the asset justifies it.

A long hold period should be a tool to unlock value, not a cover for underpreparedness. What a strong asset looks like depends on its stage and strategy.

In early-stage VC, it looks like clarity of direction, founder-market fit, and an honest assessment of how time could compound the edge. Even belief-driven investments need to be grounded in a thesis that’s internally coherent and externally testable.

In growth and buyout, it is operational stability, visibility on cash flows, governance readiness, and clear levers for scale or efficiency.

Strong private market products align their structure to the state and stage of the asset. They don’t assume time will fix fundamentals, they ensure fundamentals are in place for time to do its job.

Quick test: Is the hold period serving the thesis or compensating for it?

Risk needs to be part of the product, not hidden around it.

Good private market products talk about risk upfront. They don’t bury the bad scenarios in footnotes or rely on fine print. The downside is made clear. Tail risks, the unlikely but serious ones, are acknowledged. And if the investment doesn’t work out, there’s a clear understanding of what that means.

When products handle risk with honesty, they tend to attract investors who do the same. That usually leads to better, more stable outcomes for everyone.

Quick test: Has the sponsor openly talked about how this could go wrong and what happens if it does?

Great products don’t depend on market timing, but they do understand context.

The best private market strategies are shaped by the environment they’re launched in. They reflect current realities without being limited by them. Strong design balances urgency with restraint. It should be designed to work across cycles. If a product only makes sense today, it may not make sense at all.

Quick test: Does this make sense now? Would it have made sense two years ago? Will it still make sense two years from now?

This is the hardest trait to quantify, but often the most telling: how the product feels to hold.

Good products offer clarity over time. They reduce noise. Conviction should grow with each passing quarter. If investors find themselves second-guessing the thesis or chasing updates to feel secure, something is off. A product that wouldn’t be offered to the sponsor’s own family capital signals misalignment. Emotional soundness shows up in trust and that makes all the difference.

Quick test: Could you hold this through a rough quarter without losing sleep, or your investor’s confidence?

Before we go further, it’s worth stating clearly: even the best frameworks have limits. Structure helps, but it can’t see the future.

No framework is perfect. This one doesn’t:

So with all that in mind – caveats, nuance, and lived experience, we now come to the deeper layer behind every product decision:

While structure matters, it never exists in a vacuum. The same product can look brilliant to one allocator and baffling to another. Context changes everything. Which brings us to a critical, often overlooked question: who’s buying?

Even the best-designed product performs differently depending on who’s across the table. A family principal, an institutional allocator, and a UHNWI may be looking at the same deck, but they’re reading it through completely different lenses.

None of these perspectives are better or worse. But they are not interchangeable. A good product knows who it is built for and builds accordingly.

Just as a strong design lands differently across buyer types, a weak one tends to reveal itself in the same way, fast. If the earlier section showed what to look for, the next shows what to avoid.

Strong products tend to follow patterns. But weak ones leave traces too, often from the first conversation. We’ve seen structures that collapse under a second layer of questions. Red flags include:

There’s no definitive rulebook here, and the rules themselves are still evolving. But if this cycle has taught us anything, it’s that certain fundamentals still matter. Strong design always shows up in the fundamentals: a clear thesis, disciplined structure, and behaviour that holds up in tough times.

This cycle may have more surprises in store. The last half-decade has taught us that we rarely know where we’ll sit five years from now, just like we didn’t in 2015, or even 2020. But we’ve also learned to pay closer attention to the structures we build, the products we back, and the questions we ask.

The underwriting is getting sharper. The ecosystem is maturing. And while we won’t pretend to know where this all leads, we’ll always bet on this: stronger markets are shaped by stronger investors, and better products make both possible.

Here’s to building with that in mind.

If you’re holding the same questions we are, about structure, alignment, or timing, drop us a line. We like talking to people who think in drafts.

TERMS OF USE

Thank you for your interest in our Website at https://unlistedintel.com/. Your use of this Website, including the content, materials and information available on or through this Website (together, the “Materials”), is governed by these Terms of Use (these “Terms”). By using this Website, you acknowledge that you have read and agree to these Terms.

NO OFFER, SOLICITATION OR ADVICE

Our site is provided for informational purposes only. It does not constitute to constitute (i) an offer, or solicitation of an offer, to

purchase or sell any security, other assets, or service, (ii) investment, legal, business, or tax advice, or an offer to provide such advice or (iii) a basis for making any investment decision.

The Materials are provided for informational purposes and have been prepared by Oister Global for informational purposes to acquaint existing and prospective underlying funds, entrepreneurs, and other company founders with Oister Global's recent and historical investment activities.

Please note that any investments or portfolio companies referenced in the Materials are illustrative and do not reflect the performance of any Oister Global fund as a whole. There is no obligation for Oister Global to update or alter any forward-looking statements, whether as a result of new information, future events, or otherwise.

PURPOSE LIMITATION AND ACCESS TO YOUR PERSONAL DATA:

We will only collect your personal data in a fair, lawful, and transparent manner. We will keep your personal data accurate and up to date. We will process your personal data in line with your legal rights. We use your name and contact details, such as email, postal address, and contact number to continue communications with you. We may also use your contact information to invite you to events we are hosting or to keep you updated with our news.

USE OF COOKIES OR SIMILAR DEVICES

We use cookies on our website. This helps us to provide you with a better experience when you browse our website and also allows us to make improvements to our site. You may be able to change the preferences on your browser or device to prevent or limit your device’s acceptance of cookies, but this may prevent you from taking advantage of some of our features.

MATERIAL

The material displayed on our site is provided “as is”, without any guarantees, conditions, or warranties as to its accuracy, completeness, or reliability. You should be aware that a significant portion of the Materials includes or consists of information that has been provided by third parties and has not been validated or verified by us. In connection with our investment activities, we often become subject to a variety of confidentiality obligations to funds, investors, portfolio companies, and other third parties. Any statements we make may be affected by those confidentiality obligations, with the result that we may be prohibited from making full disclosures.

MISCELLANEOUS

This Website is operated and controlled by Oister Global in India. We may change the content on our site at any time. If the need arises, we may suspend access to our site, or close it indefinitely. We are under no obligation to update any material on our site.

CONTACT INFORMATION

Any questions, concerns or complaints regarding these Terms should be sent to info@oisterglobal.com