We enter 2024 with the lowest projections for medium term global GDP growth in decades. The IMF’s latest forecast for medium term global growth (defined as growth 5 years out) is 3.1% compared to 3.6% prior to Covid and 4.9% prior to the onset of the financial crisis in 2008. More than 80% of economies now have lower medium term growth forecasts than they had in 2008.

In the near term the IMF’s projections for GDP growth in 2024 are:

| World | 2.9% |

| Advanced Economies | 1.4% |

| Emerging and Developing Economies | 4.0% |

| China | 4.2% |

| India | 6.3% |

Reviewing the 2024 market outlook analysis of global banks, two themes and one common conclusion emerge.

The first theme is a return to a ‘normal’ financial landscape where real interest rates are positive and historical relationships between asset classes have returned. Asset allocation and portfolio construction are back in more familiar territory after the period of soft money and negative real yields.

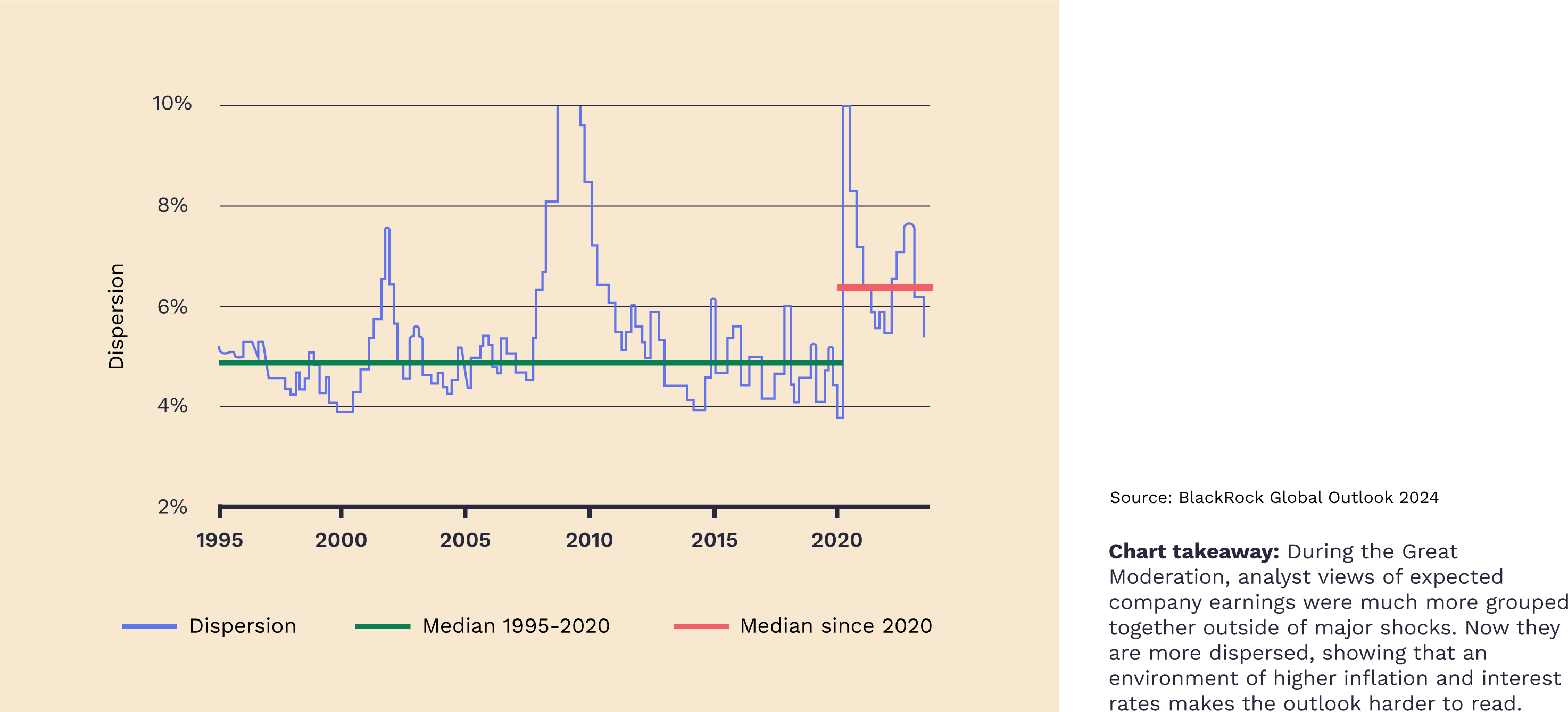

However, the return to normal relationships has occurred within a context of greater macro uncertainty, which is the second theme. One indicator of this greater uncertainty is the wider dispersion in US equity analysists’ earnings estimates. Dispersion in analysists’ estimates has increased noticeably since 2020 compared to the previous five year period because the greater macro uncertainty makes it harder to make predictions of market behavior.

The increase in uncertainty has several causes, amongst which the difficult policy trade-offs facing central banks, production constraints and the rise of populism stand out.

Ratings Downgrade: The rating downgrade of the United States reflects the expected fiscal deterioration over the next three years, a high and growing general government debt burden, and the erosion of governance relative to ‘AA’ and ‘AAA’ rated peers over the last two decades that has manifested in repeated debt limit standoffs and last-minute resolutions.

Erosion of Governance: In Fitch’s view, there has been a steady deterioration in standards of governance over the last 20 years, including on fiscal and debt matters, notwithstanding the June bipartisan agreement to suspend the debt limit until January 2025. The repeated debt-limit political standoffs and last-minute resolutions have eroded confidence in fiscal management. In addition, the government lacks a medium-term fiscal framework, unlike most peers, and has a complex budgeting process. These factors, along with several economic shocks as well as tax cuts and new spending initiatives, have contributed to successive debt increases over the last decade. Additionally, there has been only limited progress in tackling medium-term challenges related to rising social security and Medicare costs due to an aging population.

The transition to a period of greater macro uncertainty probably means that the potential gains from active portfolio management will be greater in the coming period.

The common conclusion is on India, which is consistently mentioned positively as an investment destination. In a world of larger uncertainties, this consistent endorsement stands out.

There is no doubt that India’s light is shining brightly, but it is the sole point of light in an otherwise grey and uncertain world.

We have seen that India is expected to have the strongest GDP growth of any country in 2024 and that it is consistently viewed as a good investment destination for 2024.

These expectations acknowledge the longer term reality that India is the only country to have implemented macro policies that seriously stimulate entrepreneurial activity and innovation over the last ten years.

Over the course of the 1990s many countries implemented policies that encouraged the growth of entrepreneurialism, but by 2005 the improvements in the policy, regulatory and legal environments stopped and in some cases began to reverse. To illustrate this point, the score of the five BRICS in the Franklin Institute’s Economic Freedom of the World Index (EFWI) increased by an average of 54% over 1980-2005 but increased an average of only 3% from 2005 to 2021.

India’s EFWI score is now above those of the other BRICS – and the EFWI does not consider the major contribution of India’s significant investments in roads, airports and the digital stack to the improved entrepreneurial environment.

Numerous policies of the Indian Government underwrite both the Inda macro story and the growth of India’s VC/PE space by encouraging entrepreneurialism and innovation:

A weak global macro environment combined with more uncertainty creates a structurally tougher environment in which achieving growth becomes more difficult for everyone. However, within this tougher environment India has two things in its favor that provide some insulation from the weaker global macro environment and that suggest that India can expect to retain its healthy GDP growth.

The first is that the present dynamic environment for entrepreneurial activity and innovation will continue to be supported by the bundle of policies and initiatives outlined in Box 2, and this will be combined with favorable demographics underpinning rising consumer demand.

The second is the importance of lower costs in a weak macro environment. In India innovation can be undertaken at relatively low cost and Indian business models are designed for a frugal market so that, in a weaker global macro situation, Indian businesses are likely to be able to expand both within India and offshore because they bring a strong value proposition at a competitive price.

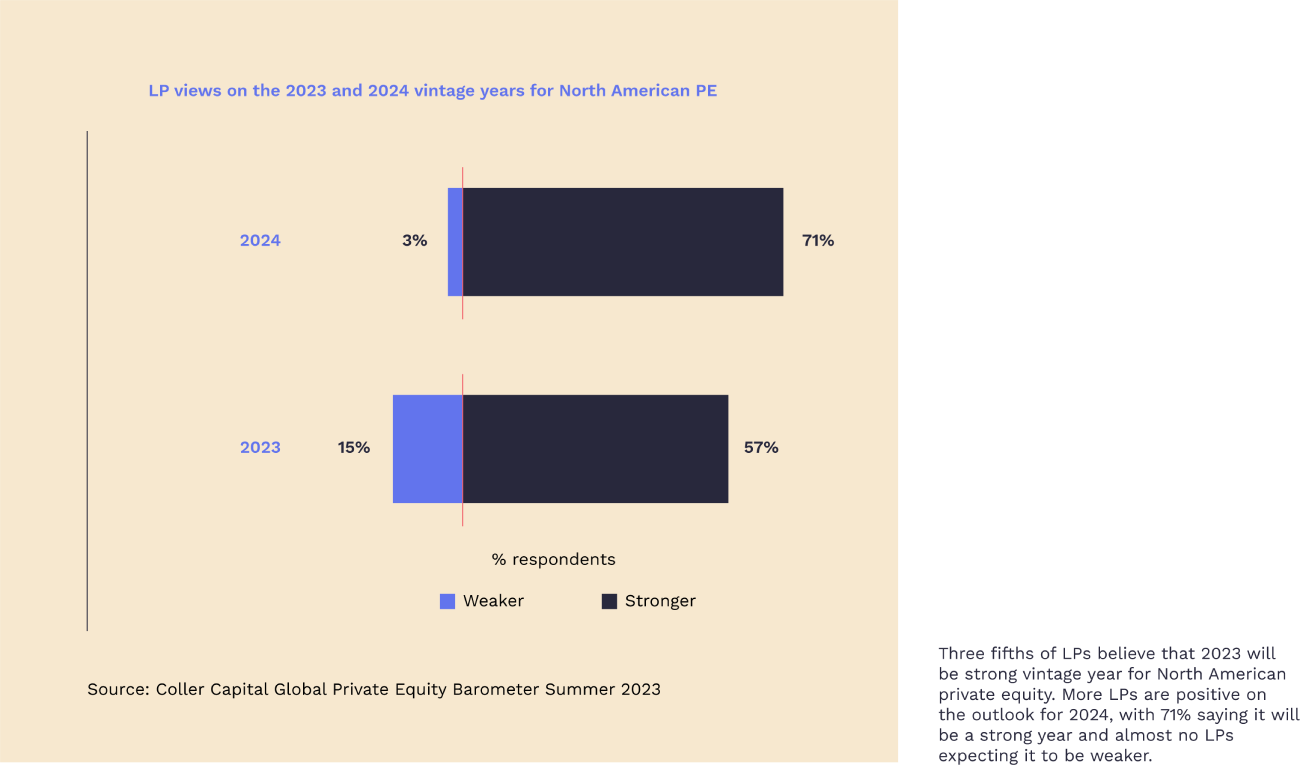

The performance of private market investments is judged based relative to the performance of the vintage year of the fund (the date of the first closing) because funds launched in different vintage years experience different market conditions in terms of entry (valuations, FOMO), value creation (weak versus strong demand) and exit (conditions in the IPO and M&A markets).

A good vintage year faces moderate valuations and lack of FOMO at the entry stage and the prospect of a buoyant exit market some time in the future.

There are indications that 2024 may be on the right side of the vintage year equation.

Valuations are moderating, particularly in later rounds. In the US the average pre-money valuations on later stage rounds are down 16%-20% from the peak year of 2021. The number of down-rounds in the US has also climbed from a quarterly average of 8% of all rounds over 2021 to 17% in Q3 2023. Indian valuations are also declining, with the most visible declines occurring among the unicorns.

While funds have considerable dry powder, fund raising has declined in both quantity and pace so pricing pressures and FOMO are not likely to return in the near future.

Pre-Seed and Seed rounds in India have a large component of rupee capital, however in later rounds foreign capital is in the majority and both the optimism and the pessimism of foreign investors has an impact on the availability of capital and on valuations.

We mentioned earlier that a common conclusion of foreign banks’ 2024 market outlook reports is that India is a good destination for portfolio allocation, so might we expect an influx of foreign capital into Indian VC and PE in 2024?

We do not think the positive India view will translate into an influx of foreign capital into VC and PE in 2024. We think it will come, but not in the near term, and this potentially creates an opportunity for domestic investors.

Recent surveys of institutional LPs indicate that the love shown to India by the market analysts is not shared by their VC/PE colleagues.

While a large majority of LPs expect more down-rounds on their existing US VC portfolios, a majority also think that 2023 will be a good vintage year for the US market and a larger majority expect 2024 to be a strong vintage year.

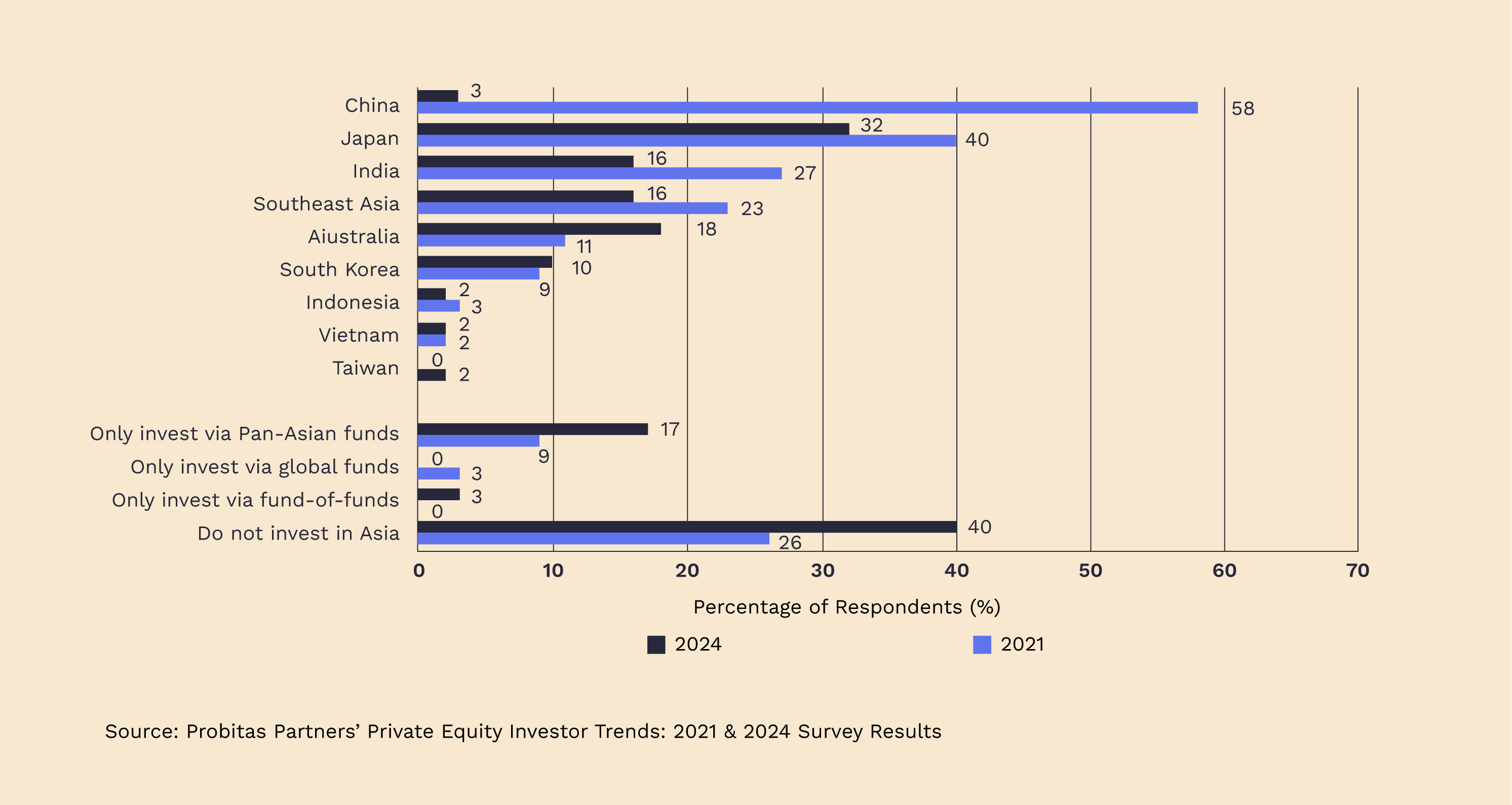

However, when looking beyond the US, institutional investors’ views are much more cautious. While 70% of Asia-Pacific LPs in the survey thought that 2024 would be a strong year for PE in the Asia-Pacific region, interest from US and EU based LPs in markets outside their home countries has declined significantly.

In another survey of LPs 51% of respondents (and 61% of North American LPs) said they did not invest in emerging markets, up 11% from 2021.

Digging into this decline in interest in private markets outside the US, it appears that the issue is the decline in the attractiveness of China which is spilling over into a more generally negative view on VC/PE in Asia. Between 2021 and 2024 LPs interested in China declined from 58% to 3%, and LPs who do not invest in Asia increased from 26% to 40%.

These survey results align with anecdotal evidence. From multiple conversations our impression is that the capital being pulled out of China by Western LPs is being kept at home for now.

However, the future opportunity can be seen in the difference in mind-set between LPs who have experience of Indian VC and PE over the last decade and those who are unfamiliar with the Indian market.

Foreign LPs with experience want to reinvest because their experience has been good and they understand not only the India macro opportunity but also the market. The foreign LPs without experience need to ascend a learning curve before they invest in India and, with the return of attractive interest rates in their home markets, they do not feel pressured to accelerate their learning journey.

However, given the favorable view of the India macro opportunity we believe that they will eventually take the journey and join their fellow LPs with experience of India to back Indian funds. We think their capital is likely to arrive in time to improve the exit environment for the 2023, 2024 and 2025 vintages of Indian VC and PE funds.

TERMS OF USE

Thank you for your interest in our Website at https://unlistedintel.com/. Your use of this Website, including the content, materials and information available on or through this Website (together, the “Materials”), is governed by these Terms of Use (these “Terms”). By using this Website, you acknowledge that you have read and agree to these Terms.

NO OFFER, SOLICITATION OR ADVICE

Our site is provided for informational purposes only. It does not constitute to constitute (i) an offer, or solicitation of an offer, to

purchase or sell any security, other assets, or service, (ii) investment, legal, business, or tax advice, or an offer to provide such advice or (iii) a basis for making any investment decision.

The Materials are provided for informational purposes and have been prepared by Oister Global for informational purposes to acquaint existing and prospective underlying funds, entrepreneurs, and other company founders with Oister Global's recent and historical investment activities.

Please note that any investments or portfolio companies referenced in the Materials are illustrative and do not reflect the performance of any Oister Global fund as a whole. There is no obligation for Oister Global to update or alter any forward-looking statements, whether as a result of new information, future events, or otherwise.

PURPOSE LIMITATION AND ACCESS TO YOUR PERSONAL DATA:

We will only collect your personal data in a fair, lawful, and transparent manner. We will keep your personal data accurate and up to date. We will process your personal data in line with your legal rights. We use your name and contact details, such as email, postal address, and contact number to continue communications with you. We may also use your contact information to invite you to events we are hosting or to keep you updated with our news.

USE OF COOKIES OR SIMILAR DEVICES

We use cookies on our website. This helps us to provide you with a better experience when you browse our website and also allows us to make improvements to our site. You may be able to change the preferences on your browser or device to prevent or limit your device’s acceptance of cookies, but this may prevent you from taking advantage of some of our features.

MATERIAL

The material displayed on our site is provided “as is”, without any guarantees, conditions, or warranties as to its accuracy, completeness, or reliability. You should be aware that a significant portion of the Materials includes or consists of information that has been provided by third parties and has not been validated or verified by us. In connection with our investment activities, we often become subject to a variety of confidentiality obligations to funds, investors, portfolio companies, and other third parties. Any statements we make may be affected by those confidentiality obligations, with the result that we may be prohibited from making full disclosures.

MISCELLANEOUS

This Website is operated and controlled by Oister Global in India. We may change the content on our site at any time. If the need arises, we may suspend access to our site, or close it indefinitely. We are under no obligation to update any material on our site.

CONTACT INFORMATION

Any questions, concerns or complaints regarding these Terms should be sent to info@oisterglobal.com