Dear Reader,

Welcome to the first newsletter of 2026. By now, resolutions have met reality. Friends have supplied the “2016 vs 2026” evidence. Geopolitics hasn’t given us one boring moment. And all that glitters is “silver.” January has done what it always does: stretched itself into a year.

January also brought a certain Goldilocks framing back to the economy: not too hot, not too cold—just right. The IMF, for one, has raised India’s GDP growth forecast to 7.3% for FY26, and India is on track to enter the upper-middle-income bracket by 2030. With Republic Day around the corner, it’s worth saying plainly: we’re building from a position of underlying strength. (There’s plenty left to fix, but the base matters.)

As we enter the second half of this decade, resilience has become muscle memory. The last five years trained it into us. The question now is more deliberate: how do we engineer forward?

In private markets, engineering can mean many things. Better underwriting. Better governance. Better alignment. Better access. But one constraint sits upstream of all of it: investability.

India’s wealth is deepening. But our allocation stack still isn’t. AIF commitments are roughly ₹15T, still a small share of household financial assets even as India’s liquid wealth continues to accelerate. Which brings us to private markets: the next leg of India’s capital formation story.

The case for private markets themselves is already settled. Across cycles, private capital has consistently outperformed public equivalents, delivering excess returns in the range of 5.3% to 9.5%. Beyond performance, the impact is structural. Public markets recycle ownership of existing assets. Private capital is often growth capital; it funds capacity, technology adoption, and company-building. This is where strategic IP is built, where technology compounds, and where the real economy of the next decade takes shape.

Performance, then, is not the constraint.

The real barrier to allocation is more psychological than financial: the anxiety of the exit. The discomfort of being locked in for long periods in a world trained on immediacy.

This is often framed as a liquidity problem. That framing is misleading.

Private markets are not meant to behave like public markets. Their strength lies precisely in giving founders time, reducing noise, and allowing patient capital to compound alpha. Compressing build cycles or forcing premature exits would erode the very return engine investors seek to protect.

Today, private markets are still structured as a single arc journey: enter, hold, and then hope for a clean ending, whether that is an IPO window, a strategic buyer, or an opportunistic secondary. When those windows are scarce or mistimed, value remains trapped on paper even as businesses continue to compound underneath.

As the market scales and domestic capital becomes the anchor, this structure must evolve. The next phase is not about accelerating exits, but about decoupling capital return from company timelines. Markets must graduate from merely marking value to creating multiple pathways to realise it.

If this sounds abstract, public markets offer the clearest blueprint.

Over two decades, India has engineered a market system strong enough to earn household trust. Millions of investors commit capital to a volatile asset class, live through drawdowns, and still show up every month with discipline. The scale of that trust is visible in the numbers: SIP AUM has grown from ₹6.8 lakh crore in FY23 to ₹16.5 lakh crore by November 2025.

It is tempting to attribute this to transparency alone. But trust was not accidental. It was engineered, slowly and deliberately, layer by layer.

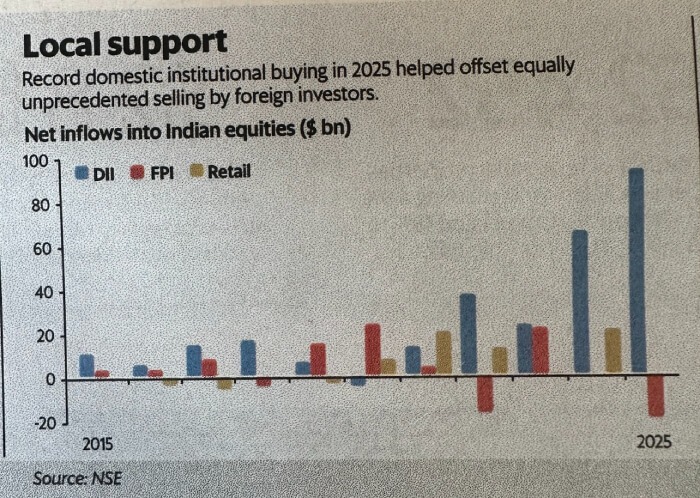

That engineering was tested in 2025 (and before). Foreign investors were on course for one of their largest net exits from Indian equities, even as domestic flows kept the market functioning. As foreign selling intensified, domestic institutional buying stepped in at record levels. The system did not freeze. The market held because domestic depth had grown strong enough to absorb the shock.

The deeper insight here is about agency. Investors participate with confidence because they know they can leave. Liquidity is not a property of being listed. It is the outcome of engineering.

This is where the next phase of private markets must focus.

The objective is not to import public market behaviour into private assets, nor to compromise the patience required to build great companies. Alpha still needs discretion, control, and time.

The work instead lies at the platform level. Engineering capital circulation around assets without disturbing how those assets are built. This is where secondary markets, portfolio level liquidity planning, and staggered realisation pathways become critical.

The task ahead is unglamorous. Borrowing the hard earned disciplines public markets developed over decades. Standardised information, counterparty discipline, repeatable processes, and transaction readiness built well in advance.

Private markets will never, and should never, offer public market liquidity. But a more stable exit environment across cycles can be created if capital return is treated as a system level responsibility rather than a single terminal event.

The comfort of an exit is what turns patience into confidence. And repeat participation is what makes a market durable. And it is the comfort of an exit that creates the courage for the entry.

As always, thank you for reading, and for shaping how we think. If you have a view on what makes exits feel credible in India, I’d genuinely love to hear it.

Happy Republic Day, and see you next month.

TERMS OF USE

Thank you for your interest in our Website at https://unlistedintel.com/. Your use of this Website, including the content, materials and information available on or through this Website (together, the “Materials”), is governed by these Terms of Use (these “Terms”). By using this Website, you acknowledge that you have read and agree to these Terms.

NO OFFER, SOLICITATION OR ADVICE

Our site is provided for informational purposes only. It does not constitute to constitute (i) an offer, or solicitation of an offer, to

purchase or sell any security, other assets, or service, (ii) investment, legal, business, or tax advice, or an offer to provide such advice or (iii) a basis for making any investment decision.

The Materials are provided for informational purposes and have been prepared by Oister Global for informational purposes to acquaint existing and prospective underlying funds, entrepreneurs, and other company founders with Oister Global's recent and historical investment activities.

Please note that any investments or portfolio companies referenced in the Materials are illustrative and do not reflect the performance of any Oister Global fund as a whole. There is no obligation for Oister Global to update or alter any forward-looking statements, whether as a result of new information, future events, or otherwise.

PURPOSE LIMITATION AND ACCESS TO YOUR PERSONAL DATA:

We will only collect your personal data in a fair, lawful, and transparent manner. We will keep your personal data accurate and up to date. We will process your personal data in line with your legal rights. We use your name and contact details, such as email, postal address, and contact number to continue communications with you. We may also use your contact information to invite you to events we are hosting or to keep you updated with our news.

USE OF COOKIES OR SIMILAR DEVICES

We use cookies on our website. This helps us to provide you with a better experience when you browse our website and also allows us to make improvements to our site. You may be able to change the preferences on your browser or device to prevent or limit your device’s acceptance of cookies, but this may prevent you from taking advantage of some of our features.

MATERIAL

The material displayed on our site is provided “as is”, without any guarantees, conditions, or warranties as to its accuracy, completeness, or reliability. You should be aware that a significant portion of the Materials includes or consists of information that has been provided by third parties and has not been validated or verified by us. In connection with our investment activities, we often become subject to a variety of confidentiality obligations to funds, investors, portfolio companies, and other third parties. Any statements we make may be affected by those confidentiality obligations, with the result that we may be prohibited from making full disclosures.

MISCELLANEOUS

This Website is operated and controlled by Oister Global in India. We may change the content on our site at any time. If the need arises, we may suspend access to our site, or close it indefinitely. We are under no obligation to update any material on our site.

CONTACT INFORMATION

Any questions, concerns or complaints regarding these Terms should be sent to info@oisterglobal.com