A Slowing World, A Steady India

In recent weeks, India’s macro story has gained both volume and substance. Headlines have spotlighted geopolitical churn, central bank pivots, and capital market volatility but beneath it all, India continues to do what it now does best: compound progress. The past month served as a reminder that India’s rise is becoming harder to ignore in the noise.

India officially became the world’s fourth-largest economy, overtaking Japan with a nominal GDP of $4 trillion, according to IMF data.

“We are the 4th largest economy as I speak. We are a USD 4 trillion economy as I speak, and this is not my data. This is IMF data. India today is larger than Japan.” – BVR Subrahmanyam, CEO, Niti Aayog

The milestone marked a credible reaffirmation of India’s upward trajectory. At the same time:

The World Bank’s Global Economic Prospects report set a cautious tone for the year ahead.

“India’s steady nominal GDP growth is translating into greater weight in the MSCI EM index, driven by its consumption strength and maturing capital markets.” – Daniel Morris, Chief Market Strategist, BNP Paribas Asset Management

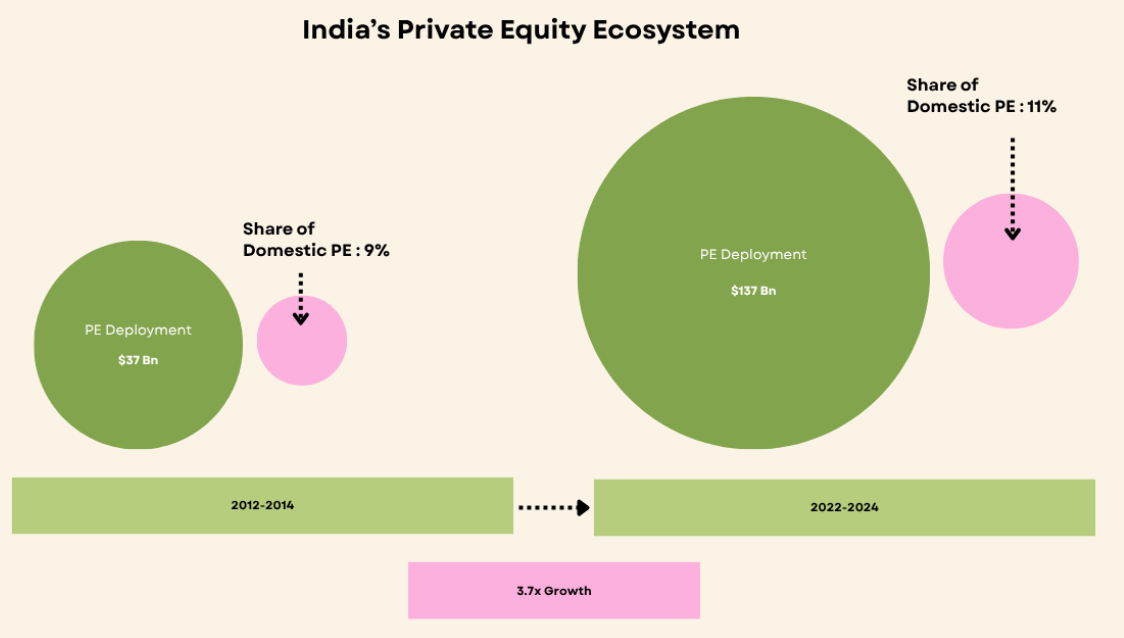

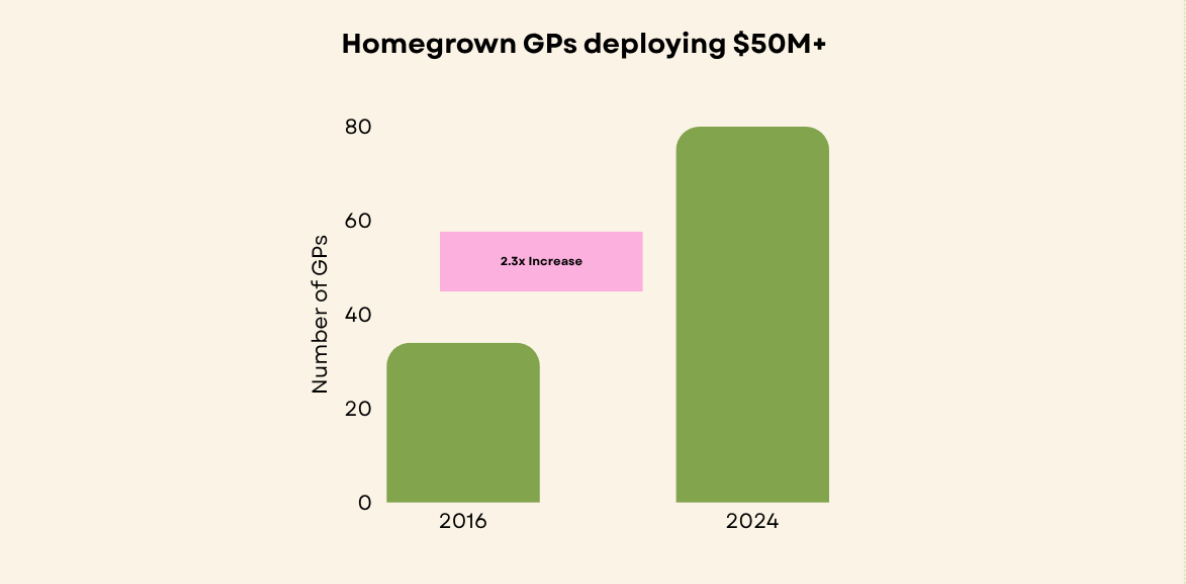

Domestic GPs are playing to India’s structural strengths, focusing on mid-market growth and sunrise sectors.

Alongside the rise of domestic fund managers, the alternative capital platform itself is gaining scale. AIF investments rose 32% YoY to ₹5.38 lakh crore in Q4 FY25, an indicator of how fast India’s alternative capital base is maturing.

Source: Mint, June 2024

The RBI’s June MPC meeting marked a clear pivot toward growth support. Key policy moves included:

Together, these decisions signal a pro-growth posture, yet one carefully calibrated. The RBI’s easing bias is backed by softening inflation and strong macro fundamentals, allowing it to act without sacrificing fiscal prudence.

(In case you missed it, last month’s memo is here.)

SOURCES:

TERMS OF USE

Thank you for your interest in our Website at https://unlistedintel.com/. Your use of this Website, including the content, materials and information available on or through this Website (together, the “Materials”), is governed by these Terms of Use (these “Terms”). By using this Website, you acknowledge that you have read and agree to these Terms.

NO OFFER, SOLICITATION OR ADVICE

Our site is provided for informational purposes only. It does not constitute to constitute (i) an offer, or solicitation of an offer, to

purchase or sell any security, other assets, or service, (ii) investment, legal, business, or tax advice, or an offer to provide such advice or (iii) a basis for making any investment decision.

The Materials are provided for informational purposes and have been prepared by Oister Global for informational purposes to acquaint existing and prospective underlying funds, entrepreneurs, and other company founders with Oister Global's recent and historical investment activities.

Please note that any investments or portfolio companies referenced in the Materials are illustrative and do not reflect the performance of any Oister Global fund as a whole. There is no obligation for Oister Global to update or alter any forward-looking statements, whether as a result of new information, future events, or otherwise.

PURPOSE LIMITATION AND ACCESS TO YOUR PERSONAL DATA:

We will only collect your personal data in a fair, lawful, and transparent manner. We will keep your personal data accurate and up to date. We will process your personal data in line with your legal rights. We use your name and contact details, such as email, postal address, and contact number to continue communications with you. We may also use your contact information to invite you to events we are hosting or to keep you updated with our news.

USE OF COOKIES OR SIMILAR DEVICES

We use cookies on our website. This helps us to provide you with a better experience when you browse our website and also allows us to make improvements to our site. You may be able to change the preferences on your browser or device to prevent or limit your device’s acceptance of cookies, but this may prevent you from taking advantage of some of our features.

MATERIAL

The material displayed on our site is provided “as is”, without any guarantees, conditions, or warranties as to its accuracy, completeness, or reliability. You should be aware that a significant portion of the Materials includes or consists of information that has been provided by third parties and has not been validated or verified by us. In connection with our investment activities, we often become subject to a variety of confidentiality obligations to funds, investors, portfolio companies, and other third parties. Any statements we make may be affected by those confidentiality obligations, with the result that we may be prohibited from making full disclosures.

MISCELLANEOUS

This Website is operated and controlled by Oister Global in India. We may change the content on our site at any time. If the need arises, we may suspend access to our site, or close it indefinitely. We are under no obligation to update any material on our site.

CONTACT INFORMATION

Any questions, concerns or complaints regarding these Terms should be sent to info@oisterglobal.com